Mitch Brown Leads NIC Active Adult Committee to Sharpen Focus on Growing Property Type

NIC’s Strategic Plan includes objectives to ‘expand the tent’ across five key focus areas – Active Adult, AgeTech, Capital for Operations, Middle Market, and Partnering for Health. Focus Area Committees (FACs) were formed to support these efforts. The Active Adult Committee is led by Chair Mitch Brown, Principal of Senior Housing Consulting. I had a chance to talk with Brown and hear his thoughts about this important committee.

Clapp: How did you first get involved with NIC as a volunteer?

Brown: In late 2017, I joined Greystar to help build a dedicated team focused on Active Adult development and operations. NIC leadership reached out to me in mid-2021 to provide input to the strategic planning committee about the place for Active Adult in NIC’s array of events and services including conference content, research, and NIC MAP Vision data. This led to me joining NIC’s Fall Conference Planning Committee and several well attended sessions on Active Adult. When the FAC (Focus Area Committee) concept emerged from the new Strategic Plan, I was asked to help form and lead the initial committee. We had our kickoff meeting in Annapolis, MD, in May.

Clapp: You are the chair of the Active Adult Focus Area Committee. Can you tell us about the composition of the committee?

Brown: Our committee members are a diverse mix of investors, operators, developers and advisors. Several are “pioneers” of the segment including the founders of companies such as Clover Group, Avenida Partners, and Sparrow Partners, as well as our co-Chair, Jane Arthur Roslovic with Treplus Communities. We also have representatives from The Carlyle Group and Greystar who collectively own, manage, and/or operate the largest portfolios of Active Adult. We brought in expert researchers from conventional multifamily and “for sale” 55+ housing to get ideas and insights from these related segments.

Clapp: Why do you think it is important for NIC to focus on Active Adult?

Brown: For several years I served as Chair of the ULI Senior Housing Council and among our most active members were Beth Mace and Chuck Harry, both former NIC senior staff members. We all felt that Active Adult was a segment of senior housing that would emerge as an important new option for the millions of Baby Boomers who would soon be entering their early seventies and thinking about different lifestyle options. As the premier conference and data source for senior housing in the U.S., it is incumbent on NIC to provide the transparency and research for this new segment much as it did for Assisted Living as it emerged in the mid- to late-1990s.

Clapp: What does the Active Adult Focus Area Committee aim to accomplish in the next year?

Brown: Our mission is to provide input and guidance on Active Adult-related conference sessions, research, and learning opportunities whether through NIC Academy, webinars, or other formats. We are working on two sessions for the Fall Conference that will focus on challenges with scale as the growth of the segment continues to ramp up as well as a workshop on analytics for the 2025 NIC Data and Analytics Conference and a panel on Active Adult’s opportunity to enhance wellness and longevity for a younger cohort. We also have plans for research including an updated white paper, more great case studies, webinars – including one this September, and Boot Camps around future conferences. And an Active Adult specialty course will be available soon through NIC Academy.

Register now for the NIC Active Adult Market Update webinar being held September 4, 2024, at 2:00pm ET. Join Mitch, Greystar’s Adam Cohan, Kimberly Byrum of Zonda, plus NIC’s Lisa McCracken and Caroline Clapp for the latest data and insights on Active Adult.

Industry Legacies: Parents Pass the Baton to the Next Generation

A Conversation with Melody, Chip, Tye, and Max Gabriel

This article is the fourth in a series showcasing parent/child dynamics across the senior housing and care industry. My conversation with the Gabriel family—fifth generation owners of Generations LLC—offers insights into why this is becoming a common trend.

Melody Gabriel is the CEO and Owner of Generations LLC—an Oregon-based owner and operator of independent living, assisted living, memory care, and skilled nursing homes. Growing up in the industry, Melody brings over 30 years of experience and unique perspective to the business. Driven by a passion to create change that makes lives better every day, she has built a strong leadership team and doubled the size of the company since 2019. Melody proudly continues the legacy of her father, Wendell White, including deeply seated values around how those at Generations do their work and the quality and attention given to staff and residents.

Chip Gabriel is former executive chairman of Generations LLC. In the 35 years he worked at the company, it grew to operate 11 communities totaling 2,288 units in five Western states. Chip is currently Managing Partner of Senior Living Transformation Company, LLC/Centered Care Inc.

Max Gabriel serves as Director of Business Development and Analytics at Generations. He works on development finance initiatives and the organization’s operations and accounting team.

Tye Gabriel is a Senior Executive Director at Generations’ Cherrywood Village property.

Tell us about yourself and your work.

Melody Gabriel: Generations was started by my great grandmother. I grew up in a senior living environment and it’s always been where I feel most myself. In college I pursued a business in psychology degree and dabbled in other interests like modeling and fashion, but my heart brought me back to working with seniors. I started my career at Generations in sales and marketing. After 10 years, I got pulled into operations where I found my home.

As the company grew, I expanded my leadership and eventually took over as CEO when my brother stepped away. It’s been deeply satisfying to me to have the influence of how we operate and serve our residents and people.

My father is low ego, insightful, and extremely passionate about senior housing. He grew up without a father so he’s very family first, business second. He structured it in a manner that allows multiple personalities to work together in leadership roles.

Chip Gabriel: I married into the business. I was drawn to Melody’s father’s passion for the residents and dedication to the people who care for them. From the beginning, the focus was on innovation, creativity and not being the biggest, but being the best.

We listened to the customer and evolved to transform properties into intergenerational lifestyle communities. Our goal with newer campuses was to be exterior-focused and invite the general public to use the bistros, performing arts centers, and other amenities.

Max Gabriel: When I was born, my mom was Executive Director of a property in Portland. My nursery was right down the hall from her office, so I literally grew up in the community. Through high school I worked as waitstaff and maintenance, then right out of college I did a more formal management training exposing me to a range of different environments.

Through it all, I never felt pressure to join the business. My parents were adamant that I could choose my own path, but at the end of the day, working with residents and changing people’s lives was too special to pass up.

Tye Gabriel: I grew up around my parents being fully immersed in the family business. Initially, I didn’t have any desire to be in it myself. I did some odd jobs in the communities through high school but didn’t have the intention of pursuing it beyond that. When I was in college and for a few years after, golf was my number one focus. Eventually, it got to a point where I didn’t feel like I had the temperament to pursue the sport as a career. It is a very self-centered role and growing up in a family business that has a team-mission, I was really missing that.

While I tried to figure out my next move, I began helping on the sales side of Generations. In 2020, I went to business school to explore what I wanted to do. I came to the conclusion that this industry is set up for exponential growth. I felt like being a part of my family’s legacy was an opportunity of a lifetime holding so much purpose. That’s what led me to the operations side of the business where I am now.

What’s it like working with your sons?

Melody Gabriel: I was raised in the environment myself, so having my boys grow up in the Generations ecosystem seemed very natural. It helps that both Max and Tye are great communicators too.

My dad set up the company and managed it in a very specific manner that empowered a healthy work environment. Additionally, we spent years getting extra education from Oregon State University and focusing on how we could be a better family business. We also work closely with a family business attorney to talk us through structure and emotions. The key is compartmentalizing, so that we can be a healthy family operating a healthy business.

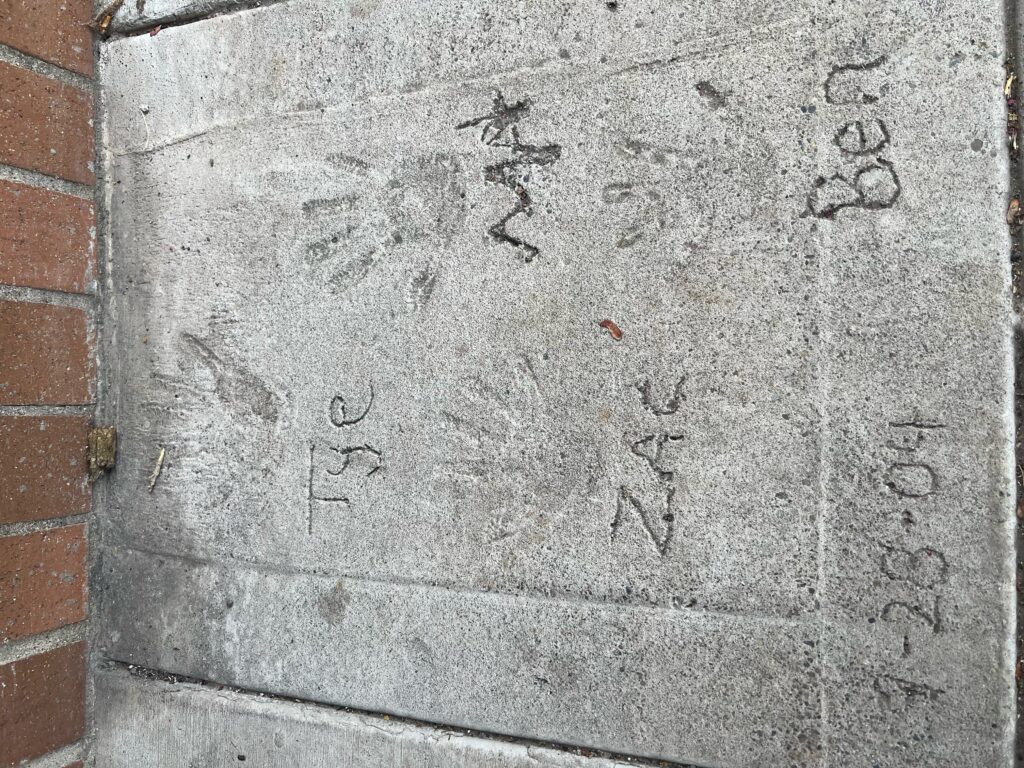

Chip Gabriel: In my previous position at Generations, working with my sons was so rewarding. I think back to opening the Cherrywood Village property in 1999, where all of Max and Tye’s grandparents lived. We poured concrete out front, and the four grandsons all made handprints. It’s cool to see the photo from when Tye was 8 –years old and consider that he’s now running the place.

We feel a great deal of success in the sustainable legacy we created.

Max and Tye, how’s working with your mother?

Max Gabriel: Seeing my mom every day at work has changed our relationship. Not in a bad way, it’s just interesting. One of the big pros is how close we all are. My grandfather takes so much pride in the family business and that has trickled down to us. In our family, it’s a privilege to work in the family business, not an expectation.

Being the owner’s kid and having everyone know who you are adds an extra layer of pressure. There are pros and cons to that. We hold ourselves to a higher standard and it’s helped me up my game.

Tye Gabriel: I had a different experience than Max. In my various roles, I haven’t worked at the home office, I’ve always been at a community in some capacity. I’ll go weeks or months without interacting with family members in a professional context. It’s allowed me to have a closer personal relationship with my parents and set clear boundaries. My team members know me as Tye, the Executive Director and not Tye, the son of the CEO, which gives me a sense of individualism within the business.

I’ve had the unique experience of having my grandfather live in the community I operate. Aside from the family business, we have a very close relationship stemming from our shared passion for golf. He is a very self-aware person, which is one of his best qualities. His combined identity as a resident and stakeholder gives him a really interesting perspective that I am constantly trying to balance with larger priorities of the community.

What advice do you have for the next generation?

Melody Gabriel: Find your passion. We spend so much of our lives in the work environment. My goal for Max and Tye was making sure they followed their passions, and not our expectations that they follow in our footsteps. I learned the importance of this through my brother who spent many years working at Generations even though his passion for it wasn’t strong.

For those interested in this career path, it’s deeply satisfying, but it’s hard work. We’re in the people business, whether you’re working with a resident or an employee. There’s a really cool heart and head alignment.

Chip Gabriel: Honest communication. For a family business to be successful, you need three intersecting circles of bylaws. Bylaws for a family, bylaws for ownership, and bylaws for management. You need to have accountability in all those things. Those who aren’t involved in the family business should be made to feel like they’re a part of the family too.

What advice do you have for the previous generation?

Max Gabriel: Lean into change. It’s natural for the older generation to hold onto the way things were, but the world is different and continuously evolving. Stay open-minded to it.

Melody Gabriel: I think that’s good advice. Ever since COVID, things are changing at a faster pace.

Max Gabriel: Senior housing is a unique business because of frontline caregivers. There has to be a balance of technology and staying up to date with the latest trends.

Tye Gabriel: In the last four years, the business and industry have probably changed more than any other time in our company’s history. One of my grandfather’s values has always been innovation and creating solutions to meet the needs of the market, which we need to continue. We also need to continue to be adaptable.

From a family business perspective, we need to stay aligned on shared goals and priorities.

Where do you see the future of senior housing?

Melody Gabriel: We all know how deeply our industry needs to change to take care of Baby Boomers. Max alluded to the importance of staying curious. Staying curious and pushing ourselves is how we’ll ultimately be able to attract more workers; pay them a fair wage and provide environments for seniors that are enriching.

Max Gabriel: I think there needs to be greater emphasis on vulnerability and transparency. Our job is tough emotionally, which requires vulnerability. That’s what separates us. That personal touch gets lost with big capital ambitions.

Tye Gabriel: When I think about the future, I think about the past as well. I think externally there’s been this perceived pressure that it’s Max and my responsibility to continue this legacy. I never felt that growing up. That lack of pressure and encouragement to pursue my own path in turn allowed me to come back and take on a leadership role within the company. I think we need to foster that sense of encouragement to the next generation of leaders in the senior space.

Insurance Trends in the Senior Housing and Care Sector

Senior living operators encounter several challenges when placing commercial insurance, driven by the unique risks associated with senior living communities and the evolving insurance market. Key challenges include aging infrastructure, regulatory compliance, litigation risks, natural catastrophes, business interruption risks, property valuations, rising costs, and fluctuating market conditions. Staying informed on commercial insurance market trends is crucial for accurately projecting budget expenses, as insurance can be one of the top five largest expenditures for operators in the senior living space.

Starting in the third quarter of 2023, the general and professional insurance market for senior living has experienced a significant shift. The impact of COVID-19 on the industry turned out to be less severe than anticipated, as many operators avoided major losses due to court closures, which lead to a backlog of cases and significant delays. Consequently, claims were settled for much less than they would have been under normal circumstances, resulting in deflated losses compared to typical industry losses.

This perceived profitability attracted new entrants to the senior living sector, drawn by inflated prices and favorable loss history. Additionally, previously dormant markets began to ramp up operations, increasing competition and driving down pricing. As a result, operators are seeing savings on their renewal premiums and favorable quotes on new acquisitions.

Despite the current market conditions, some GL/PL (General Liability/Professional Liability) carriers, such as those that previously offered historically low rates, are withdrawing from the market due to unprofitability. While the market is softening now, this trend may not last indefinitely as certain carriers continue to exit due to insufficient margins.

Management Liability is currently experiencing a softening market, similar to GL/PL. Before COVID-19, carriers faced substantial losses due to the rise in business litigation and the associated defense costs. While D&O (Directors & Officers) underwriters remain concerned about uncertainties stemming from global tensions, inflation, supply chain disruptions, and the scaling back of government subsidies, the market has seen an influx of capacity with new carriers entering, though many are initially focused on providing excess coverage. The reduction in excess pricing has led some carriers to lower premiums across the tower, including for primary coverage, thus beginning to push down primary rates.

Regarding commercial property insurance, placing coverage with admitted insurers remains challenging due to persistent issues such as natural catastrophe losses and inflation. However, 2024 is emerging as a transitional period for the E&S (Excess & Surplus) market, thanks to favorable reinsurance treaties that are creating healthy market capacity, poised for growth, increasing competition, and rate deceleration.

In recent years, supply chain disruptions, particularly in steel and lumber, contributed to rising loss costs. Carriers responded by correcting building valuations, increasing their rates and pushing for per-location limits instead of blanket limits. With much of the work on building valuations now completed, the focus has shifted to Business Interruption (BI) values, which carriers view as critical data for mitigating risks amid a bleak hurricane forecast.

Admitted carriers still anticipate continual rate increases this year, along with higher wind, hail, and water damage deductibles. Additionally, many admitted carriers are reducing their appetite for areas prone to catastrophe exposures, pushing more risks into the E&S market. Given that many senior living buildings are now 20 to 40+ years old, admitted carriers require detailed information on roof, plumbing, sprinkler systems, electrical, and structural improvements. Investing in regular updates and maintenance, along with robust risk mitigation, will help operators manage and reduce insurance premiums.

The commercial insurance market for senior housing and living is in a state of flux, influenced by both lingering effects of the pandemic and broader economic factors. While the current environment presents opportunities for cost savings and increased competition, the long-term outlook remains uncertain. Industry stakeholders must stay vigilant, adapting to changes in underwriting practices, market conditions, and emerging risks. By understanding these trends and proactively managing their insurance portfolios, senior living operators can better navigate this evolving landscape, ensuring they are well-positioned for future challenges and opportunities.

What’s the Economic Outlook for Senior Housing and Care? Is an Interest Rate Cut on the Horizon?

Economist Swonk to Brief Attendees at 2024 NIC Fall Conference.

Evidence continues to mount that the Federal Reserve could cut interest rates as soon as this September, a move that would lower borrowing costs and interest expenses, and potentially boost capital expenditures in the senior housing and care sector.

The latest inflation report released July 10 showed that the June consumer price index (CPI) dipped 0.1% from May, the first time since May 2020 that the monthly rate declined. The 12-month inflation rate clocked in at 3%, less than the 3.1% forecast by economists.

With potential monetary shifts on the horizon, distinguished economist Diane Swonk will take the main stage to present a timely keynote address on the economy at the 2024 NIC Fall Conference (September 23-25 in Washington, D.C.). A globally recognized advisor to policymakers and business leaders, Swonk is currently the chief economist at KPMG.

“By the time the NIC Fall Conference convenes, CPI figures for July and August will have been released,” said NIC President and CEO Ray Braun. “We’ll see if inflation continues to ease and what that means for future decisions by the Federal Reserve.” He added that Swonk’s presentation on Sept. 24 will help Conference attendees gauge economic conditions as they plan for 2025.

Faced with continued worker shortages, industry stakeholders are also closely watching the labor market. In his semi-annual monetary policy report to Congress last week, Federal Reserve Chair Jerome Powell not only discussed declining inflation, but also a cooling labor market.

The unemployment rate rose to 4.1% in June, the highest rate since November 2021. The Federal Reserve’s mandate from Congress is to maximize employment and keep prices stable, targeting an inflation rate of about 2%. Rising unemployment would foreshadow an interest rate cut to spur hiring.

But Powell indicated in his testimony that more evidence was needed that inflation has been tamed before cutting interest rates. He did not specify that a rate cut is likely this year or give any hints about the timing of a possible cut.

Economists think a cut could come on Sept. 17 at the meeting of the Federal Open Market Committee, which determines interest rates. However, that prediction was clouded when the government announced that wholesale prices rose in June just a day after the encouraging news of the drop in consumer prices.

How will these factors impact senior housing and care?

Swonk’s keynote session will provide a comprehensive analysis of the current economic environment and its influence on the industry. She will explore rate policy, rate expectations and the impact of the upcoming elections on fiscal and monetary policies.

Attendees can also expect to hear Swonk address:

Ongoing regulatory pressure on regional banks’ liquidity and its consequential restriction on the flow of debt capital.

The role of the private credit market.

Predictive indicators that signal changes in economic conditions.

Strategies to navigate economic uncertainties and leverage knowledge to advance the senior care landscape.

To register for the 2024 NIC Fall Conference, click here.

Senior Housing Occupancy Increases for Twelfth Consecutive Quarter in Second Quarter 2024

The NIC Analytics team presented findings during a webinar with NIC MAP Vision clients on July 18 to review key senior housing data trends during the second quarter of 2024.

NIC Analytics utilized a relatively new webinar format in which the second half featured a deep dive on a special topic. In July’s webinar, Arick Morton, CEO of NIC MAP Vision, discussed trends in Artificial Intelligence and the senior housing outlook with Lisa McCracken, NIC’s Head of Research and Analytics. NIC hopes participants enjoy this new webinar format and welcomes any comments or suggestions.

Key takeaways from the second quarter data included the following:

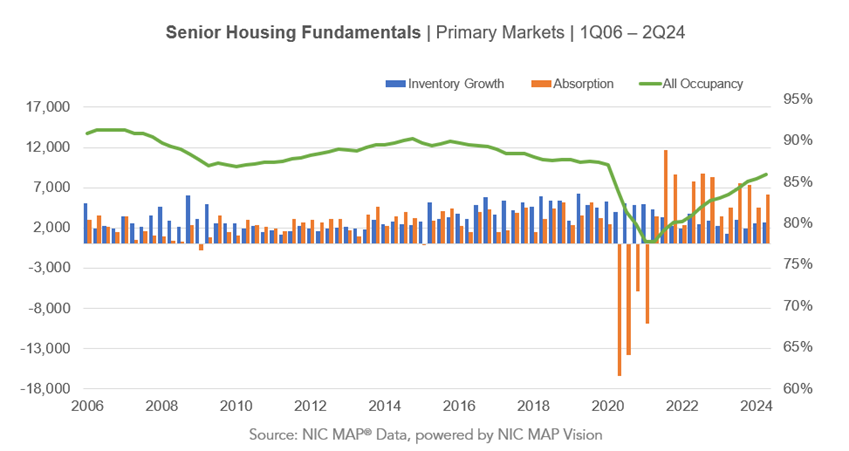

Takeaway #1: Occupancy Increased for the 12th Consecutive Quarter

The occupancy rate for the 31 NIC MAP Primary Markets rose 0.5 percentage points to 85.9% in the second quarter.

This marked the twelfth consecutive quarter of occupancy gains, driven by consumer

Takeaway #2: Occupied Units Continue Climbing to Record Highs

The total number of occupied senior housing units set another record high in the second quarter, rising to nearly 607,000 units for the 31 Primary Markets.

This trend is similar for the Secondary Markets at nearly 330,000 occupied units and shows that today more older adults than ever before are residents in senior housing properties.

Takeaway #3: Annual Inventory Growth Rate Remained Low

The inventory growth rate for both assisted living and independent living remained relatively low at 1.6% and 1.3% year-over-year in the second quarter, respectively.

Takeaway #4: Senior Housing Units Under Construction Least Since 2014

The number of senior housing units under construction in the Primary Markets continued to decline and stood at less than 27,000 units in the second quarter of 2024, which was the lowest level in 10 years.

By property type, majority independent living properties and majority assisted living properties each comprised roughly half of the construction under way.

As a share of existing assisted living inventory, units under construction totaled 3.9%, well below its peak of 10.2% in 2017.

For independent living, units under construction totaled 3.6% of existing inventory, down from its peak of 6.7% in 2020.

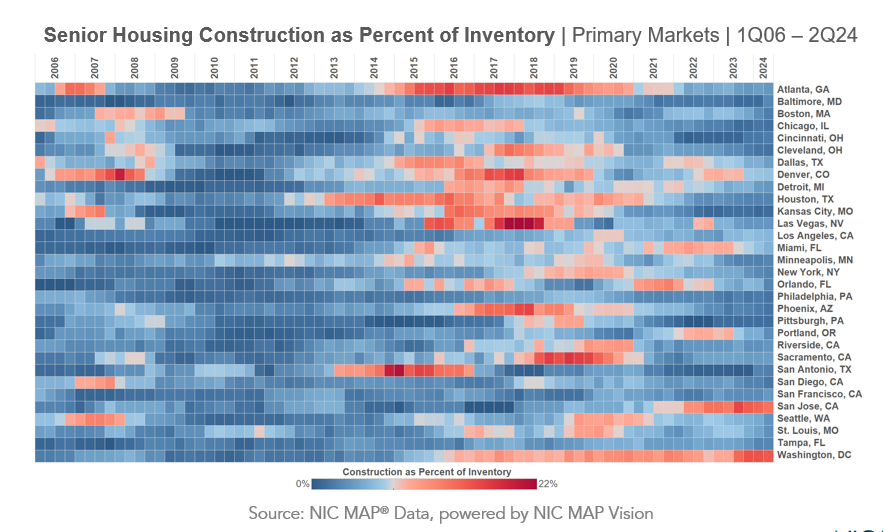

Takeaway #5: Construction Activity Still Slow in Most Markets

By metro area, this heat map shows which markets are experiencing the most construction activity.

The blue tones on the right side of the chart for the most recent quarter indicate that construction activity is relatively “cool” in most markets.

And the markets that are shaded brighter red had the most construction as a percent of inventory in the first quarter. This group continues to be led by Washington, D.C., and San Jose, followed by Los Angeles and Denver.

At the other end of the spectrum are markets where there is very little construction underway, although we no longer observe any markets with zero construction.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. NIC's privacy policy can be viewed here. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.