Mullen and Colson Scholars Lead the Way

With an assist from NIC, universities and colleges are ramping up their senior living programs helping to build a robust pipeline of new, committed industry leaders.

Take, for example, Rebecca Bond. She’ll graduate this spring with a master’s degree in Management of Aging Services from the Erickson School of Aging Studies at the University of Maryland Baltimore County (UMBC).

Trained as a physical therapist, Bond previously worked at The Village at Rockville, a life plan community (CCRC) in Rockville, Maryland. During the pandemic, she took on more leadership responsibilities and started taking classes at the Erickson School to sharpen her management skills.

With the help of a $5,000 Mullen Scholarship, named in honor of NIC co-founder Anthony J. Mullen, she was able to devote full time to pursue a graduate degree at the Erickson School. “I could not have afforded to attend school full time without the scholarship,” said Bond, who also has a teaching assistantship at the school. Asked about her career goals, Bond said: “I’d like to start a business to help older adults age in place wherever they choose.”

Pictured: Rolanda Bragg, Dr. Dana Bradley, Michele Steele, Robert Kramer, and Rebecca Bond

NIC has a long history of working with colleges and universities to raise the profile of the industry and to educate new leaders. As a nonprofit organization with a mission to improve the lives of older adults, NIC has helped to support senior living university programs and scholarships.

In addition to the Mullen Scholarship, NIC also donated $100,000 to help fund the William E. Colson Scholarship at the Erickson School. It is named for the former president and CEO of Holiday Retirement Corp. Colson, now deceased, matched NIC’s gift at the time with a $100,000 donation of his own.

“The industry needs to attract the best and the brightest,” said NIC Co-Founder and Strategic Advisor Robert G. Kramer. He is also Founder & Fellow at Nexus Insights, a think tank advancing the well-being of older adults through innovative models of housing, community, and healthcare. “These scholarships will help meet senior living’s huge leadership and workforce demands.”

The Erickson School serves 800 students through its program that combines business management, public policy and the study of aging to meet the demand for educated and innovative leaders in the longevity market. The program offers undergraduate and graduate degrees in aging studies, along with merit and need-based scholarships.

The Mullen and Colson scholarships are both endowments. Donations are invested and a portion of the earnings from the investment are awarded as scholarships. Awards range from $2,500 to $10,000. “We continue to raise money from donations,” said Paul Stearns, assistant dean and chief of staff at the Erickson School.

Spreading the Word

The professional staff at NIC and its board members have donated hours of their own time to teach classes and speak at various other schools about the senior housing and care industry. They have also helped to develop curriculums to spotlight the field’s sizable opportunities amid a growing wave of older adults.

To further bolster its educational efforts, NIC’s Future Leaders Council includes a university outreach committee. They work with the colleges and graduate schools they attended and other schools to raise the profile of the field and attract more students to the sector. NIC also offers scholarships to select students currently enrolled in senior living programs to attend its conferences.

Recounting the history of NIC’s educational efforts, Kramer recalled that it was Mullen who first recognized the need to educate people about the senior living industry. In the 1990s, when the industry was just emerging, many people either weren’t aware of senior living or equated it with the stereotype of old-style institutional nursing homes. “We were an unknown,” said Kramer.

In 1995, NIC launched an executive development program at Johns Hopkins University. “Mullen drove that program,” said Kramer. “He had a passion for education.”

The program later moved to UMBC and in 2004 John C. Erickson founded the Erickson School of Aging Studies with the backing of then UMBC President Freeman Hrabowski.

Well-known in the industry, Erickson was the CEO and founder of Catonsville-based Erickson Living. He helped to establish the school with a $5 million donation which was matched by the state of Maryland. NIC donated $100,000 to help launch the school.

The NIC executive education program provided the school’s primary enrollment. Mullen and Kramer devoted much of their time to ensure that the curriculum would meet the needs of the next generation of senior housing leaders.

When Mullen died suddenly in 2018, Kramer led an effort to fund the Anthony J. Mullen Scholarship program in his honor at the Erickson School, raising more than $400,000. A broad cross section of industry leaders and stakeholders contributed to the fund. Brookdale Senior Living made the largest donation to honor long-time CEO Bill Sheriff, now deceased. “Our goal with the scholarship fund was to honor Mullen’s passion for senior living and education,” said Kramer.

Today, Mullen’s legacy is being realized by students like Demetrie Garner. He is a Mullen Scholar and in his last year as an undergraduate at the Erickson School. Like many students at the school, Garner, age 44, is finishing a degree later in life to make a change.

Garner’s grandmother had a stroke in her 70s and then suffered from dementia. “That always stuck with me,” said Garner, who spent years struggling with substance use disorder. He enrolled at the Erickson School and continues to work full time in research at a hospital. This year he received a $5,000 Mullen scholarship.

“The money is great, but there’s something special about the acknowledgement,” said Garner. With a degree in the management of aging services, he plans to work with older people who struggle with substance abuse and also need treatment for hepatitis C infection, conditions that often go hand-in-hand. “The scholarship gave me a real burst of confidence,” he said.

—-

Note: This is the first in a series of articles spotlighting senior living scholars and the university programs that support them. The stories of these future leaders highlight the personal and institutional commitment that NIC has made to the wellbeing of older Americans.

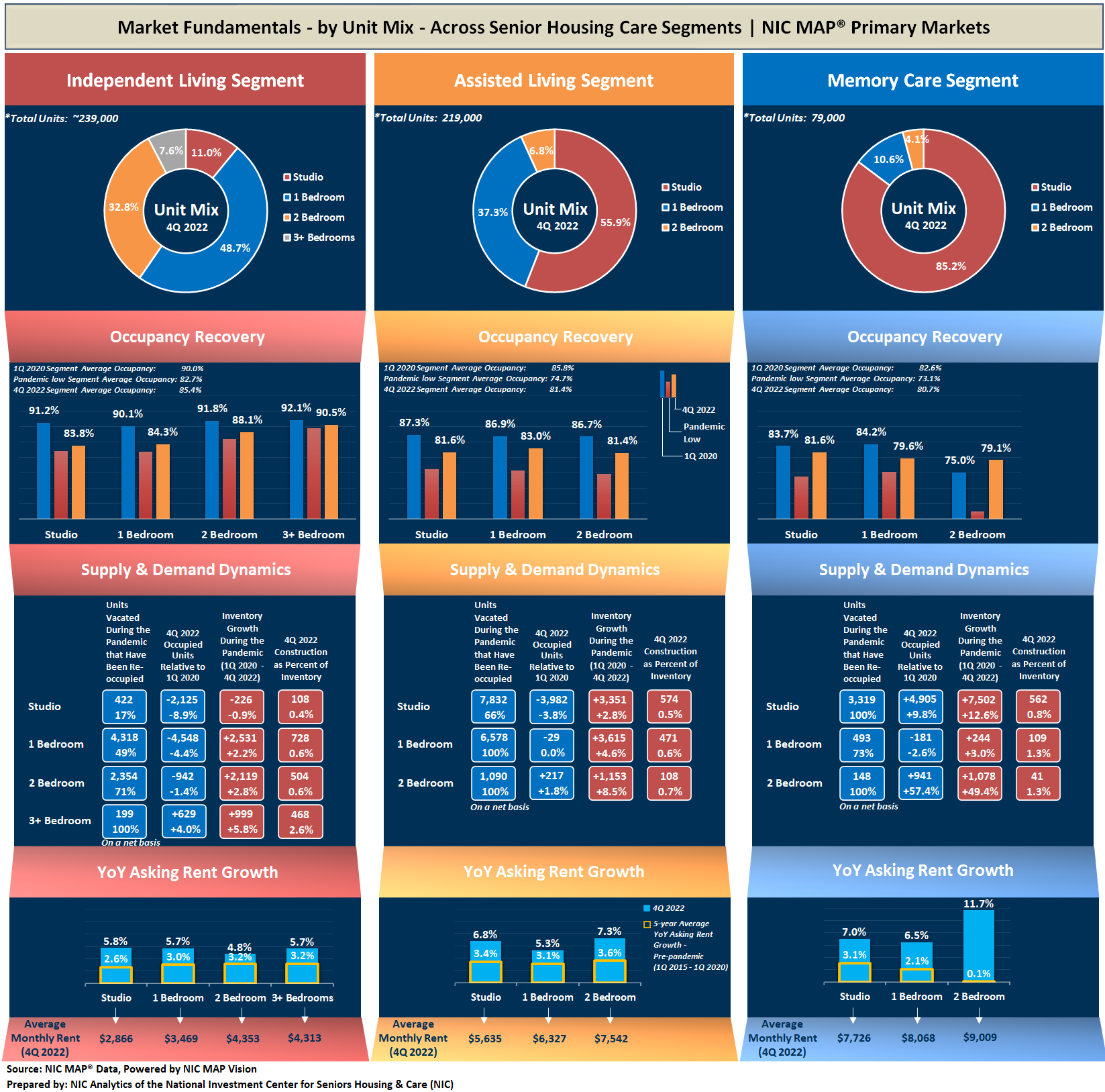

It’s a tale of two markets and many influencing factors as we move further into 2023. The capital markets remain hostage to the Federal Reserve which continues its course of tighter monetary policy and higher interest rates. Most pundits believe this will continue through mid-year 2023 until tangible evidence emerges of decelerating inflation, and in particular service inflation. Meanwhile, market fundamentals continue to improve for senior housing, with rising occupancy rates, strong demand patterns, and limited, albeit on-going, inventory growth.

It’s a tale of two markets and many influencing factors as we move further into 2023. The capital markets remain hostage to the Federal Reserve which continues its course of tighter monetary policy and higher interest rates. Most pundits believe this will continue through mid-year 2023 until tangible evidence emerges of decelerating inflation, and in particular service inflation. Meanwhile, market fundamentals continue to improve for senior housing, with rising occupancy rates, strong demand patterns, and limited, albeit on-going, inventory growth.