Jobs Increase by 311,000 in February; Jobless Rate Rises to 3.6%

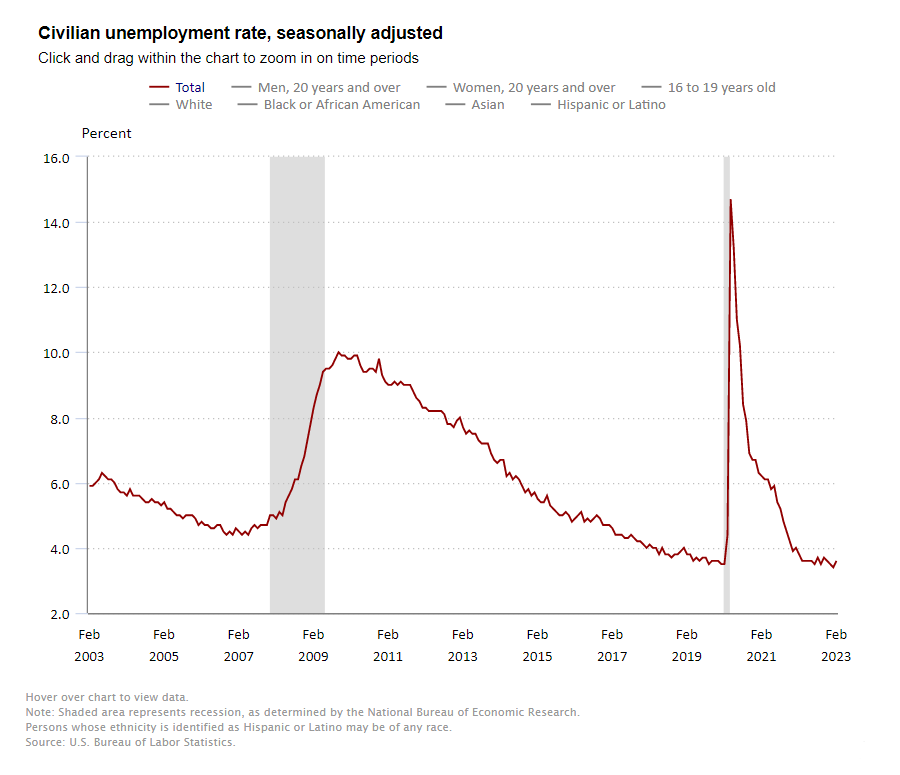

The unemployment rate reversed course and rose to 3.6% in February from 3.4% in January, which was its lowest level since 1969.

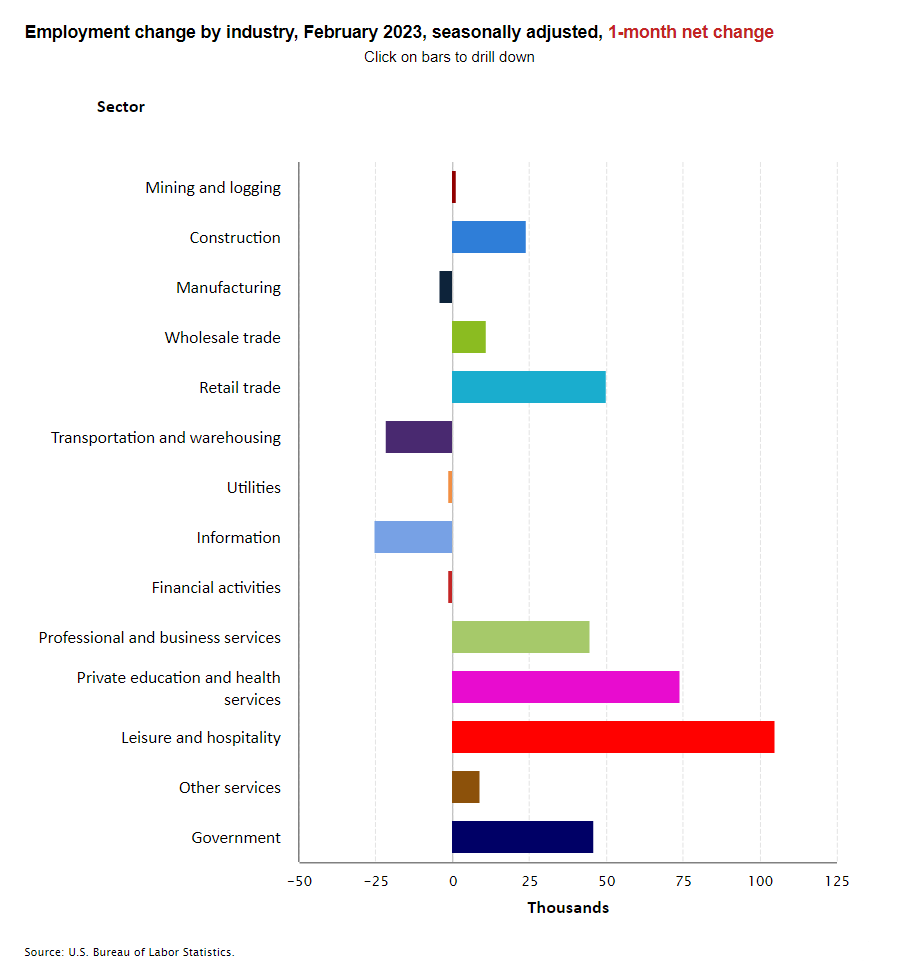

The unemployment rate reversed course and rose to 3.6% in February from 3.4% in January, which was its lowest level since 1969. Separately, the U.S. Bureau of Labor Statistics also reported that nonfarm payrolls rose by 311,000 in February 2023, below the monthly pace of 343,000 over the prior six months, but still strong. Market expectations had called for a gain of less than 225,000 jobs. Revisions subtracted 34,000 positions to total payrolls in the previous two months.

Today’s report shows the labor market remains strong with the economy still creating jobs at a rapid, albeit, slowing pace. That said, the slight rise in the jobless rate and a slowing in average hourly earnings suggest a potential adjustment in the labor markets is starting to occur. This report is not likely to change the path of the Federal Reserve which continues to increase interest rates to slow the economy in its fight against inflation. All eyes will now be focused on the CPI report to be released next week as the market tries to determine how much higher the Fed will push interest rates.

Employment in health care rose by 44,000 in February, compared with the average monthly increase of 54,000 over the past six months. Employment in nursing care facilities grew by 5,400 jobs from last month and 43,500 from year-earlier levels and stood at 1,386,800 positions. Jobs increased by 9,600 positions in CCRC and assisted living facilities and were up by 60,300 from year-earlier levels to 940,300 jobs.

In the household survey conducted by the BLS, the jobless rate increased 0.2 percentage point to 3.6%, up from 3.4% in January which was the lowest rate since 1969. Both months’ unemployment rates were well below the 14.7% peak seen in April 2020. The underemployment rate was 6.8% versus 6.6% in January.

Average hourly earnings for all employees on private nonfarm payrolls rose by $0.08 in January to $33.09. This was a gain of 4.6% from year-earlier levels.

The labor force participation rate inched up to 62.5% in February, up from 62.4% in January and the highest level since March 2020. It was below the February 2020 level of 63.3%, however.

Among the major worker groups, the January unemployment rates were 3.2% for adult women, adult men (3.3%), teenagers (11.1%), Whites (3.2%), Hispanics (5.3%), Blacks (5.7%), and Asians (3.4%), according to the U.S. Bureau of Labor Statistics.

Executive Survey Insights Wave 50: February 1 to 28, 2023

In a new question to the ESI, respondents were asked what areas have been impacted by the rising interest rate environment.

“In a new question to the ESI, respondents were asked what areas have been impacted by the rising interest rate environment. Purchasing properties was the area most reported to be affected by rising interest rates, followed by the ability to recapitalize properties. Across all care segments, one in twelve operators (8%) indicate that their abilities to purchase, sell, and recapitalize properties have all been impacted by the rising interest rate environment.

Respondents were also asked if their organization has set up formal partnerships with health care risk-sharing entities, such as accountable care organizations (ACOs) or Medicare Advantage (MA) plans. Four out of five respondents (81%) indicate that their organization does not have formal health care partnerships established, however a portion of this group (26%) also indicate that their organization is in active discussions to establish these types of partnerships. Only one in five (19%) responding organizations have formal partnerships with health care risk-sharing entities.”

–Ryan Brooks, Senior Principal, NIC

This ESI survey includes responses from February 1, 2023, to February 28, 2023, from owners and executives of 58 small, medium, and large senior housing and skilled nursing operators across the nation, representing hundreds of buildings and thousands of units across respondents’ portfolios of properties. More detailed reports for each “wave” of the survey and a PDF of the report charts can be found on the NIC COVID-19 Resource Center webpage under Executive Survey Insights.

In the February 2023 survey, respondents were asked in what areas their organization is using technology to maximize the efficiencies of the existing workforce. The most common area where technology is being deployed to maximize workforce efficiencies is in Human Resources. Categories of technological deployment within Human Resources include recruiting, staff onboarding, staff training, and employee retention. Almost nine of ten respondents (86%) reported using technology to improve efficiencies in Human Resources, followed by two-thirds (67%) deploying technology in Operations, and more than half deploying technology in Marketing (59%) and Finance (55%). Only one out of every six respondents reported using technology to improve workforce efficiency in the area of Supply Chain, however.

With the area of Human Resources experiencing a high degree of technological implementation to improve workforce efficiencies, it may not come as a surprise that operators are expressing some optimism with regards to their agency staff utilization in 2023. Two-thirds (67%) of responding operators expect to use less agency labor in 2023 when compared to 2022. Almost one-third (28%) anticipate using the same amount of agency labor, and only 5% expect to require more agency utilization than last year.

Technology applications in the Operations area include voice-enabled rooms, electronic medical records, and medication distribution. Applications within the Marketing area include virtual tours and customer relationship management while applications within the Finance area include accounting and procurement practices.

In a new question to the ESI, respondents were asked what areas have been impacted by the rising interest rate environment. Purchasing properties was the area most reported to be affected by rising interest rates, followed by the ability to recapitalize properties. Across all care segments, just under one in ten operators (8%) indicate that their abilities to purchase, sell, and recapitalize properties have all been impacted by the rising interest rate environment.

Respondents were also asked to specify in what ways those areas have been affected. Responses include an increased cost of capital, increased difficulty reaching good financing terms, and the increased cost of debt leading to wider bid-ask spreads that put both sellers and potential recapitalization partners on the sidelines.

When asked about other challenges currently facing their organization, rising operator expenses was cited as the most common (26%), followed by staff turnover (24%), and attracting community and caregiving staff (23%). Less commonly cited challenges include low occupancy rates (10%), new competition (6%), and the 2023 recession (6%).

In the February survey, respondents were asked if their organization has set up formal partnerships with health care risk-sharing entities, such as accountable care organizations (ACOs) or Medicare Advantage (MA) plans. Four out of five respondents (81%) indicate that their organization does not have formal health care partnerships established, however a portion of this group (26%) also indicate that their organization is in active discussions to establish these types of partnerships. Only one in five (19%) responding organizations have formal partnerships with health care risk-sharing entities. Among organizations who do currently have these formal partnerships established, responses show that the programs are not always implemented in every community. One-third (30%) of operators report these partnerships are established in up to 25% of their communities. One-tenth of operators indicate these programs are implemented in between 26-50% and another one-tenth indicate they are implemented in between 51-75% of their communities. The remaining half of responses have implemented these programs in between 76-100% of their communities.

February 2023 Survey Demographics

Responses were collected between February 1, 2023, and February 28, 2023, from owners and executives of 58 senior housing and skilled nursing operators across the nation.

Owners/operators with 1 to 10 properties comprise more than one-half of the sample (60%). Operators with 11 to 25 properties account for one-fifth (19%) and operators with 26 properties or account for another one-fifth (21%).

Two-thirds of respondents are exclusively for-profit providers (64%), one-third operate not-for-profit seniors housing and care properties (31%), and 5% operate both.

Many respondents in the sample report operating combinations of property types. Across their entire portfolios of properties, three-quarters (74%) of the organizations operate seniors housing properties (IL, AL, MC), 21% operate nursing care properties, and 28% operate CCRCs – also known as life plan communities.

The March 2023 ESI survey is currently open and will be collecting responses through March 31, 2023. If you are an owner or C-suite executive of seniors housing and care and would like an invitation to participate in the survey, please contact Ryan Brooks at rbrooks@nic.org to be added to the list of recipients.

NIC wishes to extend a heartfelt thank you to the owners and operators who have contributed to this survey over the past three years. It is remarkable that we have now completed more than 50 waves. We have surveyed through numerous challenges — COVID-19, threats of a looming recession, labor shortages, inflation, and rising expenses — many of which persist. As we continue to navigate these challenges, your input and real-time insights help ensure the narrative on the senior housing and care sector is accurate. By demonstrating transparency, you build trust.

The senior housing stabilized occupancy rate for the NIC MAP Primary Markets edged up to 84.3% in the February 2023 reporting period.

The senior housing stabilized occupancy rate for the NIC MAP Primary Markets edged up to 84.3% in the February 2023 reporting period, up 0.2 percentage point (pps) from the January 2023 reporting period on three-month rolling basis, according to intra-quarterly NIC MAP® data, released by NIC MAP Vision. From its pandemic record low of 80.3% in June 2021, senior housing stabilized occupancy increased by 4.0pps but remained 5.1pps below pre-pandemic March 2020 levels of 89.4%. Drilling down by metropolitan markets, Boston ranked first among the 31 NIC MAP Primary Markets with a stabilized occupancy rate of 89.8% (up 0.2pps from January 2023 and 7.1pps from its pandemic record low, but still 2.3pps below March 2020 levels). Boston’s stabilized occupancy rate was nearly 6pps above the average for NIC MAP Primary Markets.

By Majority Property Type. At 86.3%, the stabilized occupancy rate for majority independent living (IL) properties for the NIC MAP Primary Markets inched up 0.1pps from the January 2023 reporting period on a three-month rolling basis, but remained 5.0pps below March 2020 levels. For majority assisted living properties (AL), the stabilized occupancy rate for the NIC MAP Primary Markets was up 0.2pps to 82.2% from January 2023 but still 5.0pps below March 2020 levels.

Stabilized occupancy for AL continued to recover relatively fast compared with IL despite the relatively large inventory growth since the onset of the pandemic, but it’s notable that the AL stabilized occupancy rate also fell further from peak to trough. From it’s pandemic-related low, stabilized occupancy for AL increased by 5.5pps, twice the increase for IL (up 2.7pps since June 2021).

Inventory Growth. From March 2020 to February 2023, the inventory of IL and AL for the NIC MAP Primary Markets increased by 5.6% and 7.4%, respectively. However, from year-earlier levels, the inventory of IL increased by 1.9% or 6,490 units in the February 2023 reporting period, 0.3pps larger than that of AL (1.6pps). Notably, for both IL and AL inventory growth continued to be relatively slow compared with pre-pandemic levels, but growth in inventory did occur.

While new inventory compounded the downward pressure on occupancy during the height of the pandemic, this slowdown in the growth in senior housing inventory and development activity is helping to bring supply and demand into better balance and will ultimately serve as a tailwind for the occupancy recovery.

Select Metropolitan Markets. Stabilized occupancy rates increased or remained stable in 20 of the 31 Primary Markets for IL in the February 2023 reporting period compared with January 2023. Boston’s stabilized occupancy inched down by 0.1pps from the January 2023 reporting period, but at 94.0%, Boston continued to rank the highest among the 31 NIC MAP Primary Markets. Boston recovered 5.2pps from its pandemic-low and is currently 1.5pps short of reaching a full recovery and returning to March 2020 levels (in terms of stabilized occupancy). Orlando IL stabilized occupancy improved by 0.2pps from January 2023, but at 79.2%, it is still ranked at the bottom of the pack. In fact, Orlando is the only IL primary market with an average occupancy rate below 80%.

Stabilized occupancy rates rose or remained stable in 24 of the 31 Primary Markets for AL in February 2023 compared with January 2023. Boston had the second highest occupancy rate for AL among the 31 Primary Markets at 86.0% (up 0.4pps from January 2023 and 8.8pps from its pandemic record low, but still 3.1pps below March 2020 levels). Cleveland stabilized occupancy rate stood at 78.2% in February 2023, up 0.3pps from January 2023. Cleveland had the second lowest occupancy rate for AL among the 31 Primary Markets.

Keep track of the most timely comprehensive review of the sector’s market fundamentals and trends. The NIC Intra-Quarterly Snapshot monthly publication, available for complimentary download on our website, continues to provide a powerful and closely watched means to stay ahead of industry trends, even as senior housing markets sustain a fast pace of evolution and adaptation, amidst an apparent recovery.

The March 2023 IQ Snapshot report will be released on our website on Thursday, March 9, 2023, at 4:30pm.

Interested in learning more about NIC MAP Intra-Quarterly data? To learn more about NIC MAP Vision data, schedule a meeting with a product expert today.

Exploring the Interplay Between Inflation, Rate Growth, Demand and Occupancy in Senior Housing

In-depth analysis on the relationship between inflation, the pace of growth seen in-place actual rates, demand and occupancy in senior housing.

An In-Depth Analysis of NIC MAP Vision Actual Rates Data

Executive Summary

Through this in-depth analysis, we hope to shine a spotlight on the relationship between inflation, the pace of growth seen in-place actual rates, demand and occupancy. Actual in-place rates refer to effective rates or the rates that are “actually being paid” to live in senior housing. This is often not the same as the asking or listing rate that may be advertised or listed in a brochure.

NIC MAP Vision Actual Rates data has been collected for the last eight years with the ongoing aim of NIC to bring greater transparency into the industry. More specifically, this effort has included the collection of rent roll metrics on move-in, in-place and asking rates.

This blog is separated into three sections:

Section 1 provides background on the data collection process and its importance as well as the evolution of the actual rates database.

Section 2 looks at the relationship of inflation to in-place rate growth since the onset of the pandemic by specific senior housing care segments, i.e., independent living, assisted living and memory care, and finds distinct patterns of rate growth based on the level of inflation.

Section 3 takes a deep dive into actual rates data to uncover property level insights on the pattern of rate growth, occupancy and demand. Notably, this is one of the first in-depth analyses conducted on this data since the launch of the Actual Rates Data Initiative by NIC MAP Vision in 2015. This analysis was conducted using quintiles to examine the distribution of in-place rate growth in December 2022 from year-earlier levels on a same store basis.

We start with a summary of key findings.

Unveiling the Key Takeaways

Having good data processes in place can be considered as a proxy for better management and performance when evaluating a senior housing property, as well as an indicator of how the sector is evolving on a broader scale.

The year-over-year pace of growth in in-place rates for all care segments generally stayed moderate and largely aligned with the inflation rate in 2020. However, in the first half of 2022, as inflation reached 40-year highs, senior housing in-place actual rates also rose to record highs from year-earlier levels across all senior housing care segments despite the market’s still relatively low occupancy levels in general.

A notable relationship exists between in-place rate increases, demand growth and the pace of occupancy recovery. These relationships differ between independent living care segments (frequently more of a lifestyle choice than need-driven) and assisted living care segments/memory care segments (more of a need-driven than lifestyle choice.

For the independent living care segments (frequently more of a lifestyle choice than need-driven) the data shows that the stronger the demand, the greater the pace of increases in in-place rates. Notably, annual increases in in-place rates are highly associated with stronger demand and improvements in occupancy rates.

The relationship is NOT the same for the assisted living care segments and memory care segments – (more need-driven than lifestyle driven). For these segments, the data suggest that there is negative correlation between in-place rate increases and demand growth/occupancy recovery. This means that, as year-over-year in-place rate increases get smaller, there is a stronger demand growth and occupancy recovery, on average.

Additionally, there is evidence that operators bought occupancy by limiting rent growth. That is, the lowest occupied assisted living and memory care segments were able to generate new demand and grow occupancy faster, but this occurred largely because of minimal or even negative rent growth. And on the other hand, the highest priced assisted living and memory care segments were able to command the most rate growth, maintained relatively stable occupancy, but saw little net new demand.

Further, the analysis also highlighted the importance of understanding what current and potential senior housing residents are willing to pay and the potential impact of higher rate increases on the pace of move-ins and move-outs, demand growth, and occupancy recovery—as it pertains to in-place rates.

Section I – Good Data, Good Management: The Link Between Effective Data Processes and Performance.

“With data collection, ‘the sooner the better’ is always the best answer.” — Marissa Mayer

Data powers everything that we do. We live in a data-driven world, which means, without accurate, relevant, and timely data, it is nearly impossible to make informed decisions, evaluate risks and opportunities, understand the context in which we operate, and develop effective business solutions in today’s constantly evolving markets.

For the senior housing and care sectors, collecting and applying accurate data is as important as ever. That said, it is fair to acknowledge that it is not always an easy task for many senior housing and care providers. Data collection involves both human and technological resources, including well-designed organization structure, data collection and storage infrastructures, and efficient internal processes. Having good data processes in place can be considered a proxy for better management and performance when evaluating a senior housing property, as well as an indicator of how the sector is evolving on a broader scale.

The Evolution of NIC MAP Vision Actual Rates Data: Is the Senior Housing Sector Meeting the Needs of Today’s Market?

One of the many strategic initiatives undertaken by NIC and NIC MAP Vision over the years has been the NIC MAP Vision Actual Rates Data Initiative. This has been driven by the need to increase transparency in the senior housing sector to achieve greater parity to data that is available in other real estate property types.

This strategic initiative provides accurate data on the monthly rates that senior housing residents are specifically paying compared to properties’ asking or listed rates. The dataset includes nearly eight years of data for in-place rates, move-in rates, asking rates, occupancy, and leasing activity, as measured by monthly move-in and move-out velocities from April 2015 through December 2022.

Each quarter, NIC MAP Vision releases monthly time series of actual rates comprised of end-of-month data for each respective month. The release includes aggregate national data across senior housing property types (i.e., majority independent living and majority assisted living) and senior housing care segments (i.e., independent living, assisted living, and memory care).

In recent years, the dataset has grown to report the aggregate data for select metropolitan markets at the care segment level (12 markets for the independent living care segment, 22 markets for the assisted living care segment, and 16 markets for the memory care segment) to gain a comprehensive understanding of markets and their actual rates dynamics. This data collection has provided the ability to compare move-in and move-out velocity measures and, importantly, an assessment of discounts and concessions being offered to residents as they move into properties. However, reporting on additional markets relies upon participation rates of the individual market’s senior housing operators.

Participation from all senior housing providers is key to increasing transparency in the sector and meeting the needs of today’s market. The more accurate data that is collected, the more reliable the conclusions and valuable the insights will be. This not only benefits the industry as a whole, but also individual operators who can use the insights gained from analyzing actual rates data for improved decision-making and better outcomes for all stakeholders involved.

Section 2 – The Pandemic’s Ripple Effect: Exploring the Connection Between In-Place Rates and Inflation.

Largely driven by supply shortages for goods, rising energy prices, as well as escalating rents and home prices, inflation, as measured by the year-over-year change in the consumer price index (CPI), increased by 9.1% in June 2022, the highest rate in four decades. Subsequently, and following a year of aggressive interest rate hikes by the Federal Reserve to control inflation, the annual inflation rate in the U.S. slowed for a sixth straight month to 6.5% in December 2022, down 2.6 percentage points from the highs seen in June 2022 (9.1%). In January 2023, the annual inflation rate inched lower and stood at 6.4%.

Despite this recent deceleration in price increases, it remains difficult to say if and when inflation will meet the Fed’s 2% inflation target. However, following a series of 0.75 percentage points increases in the federal funds rate by the Fed, the 0.25 percentage points increase in the federal funds rate at the last FOMC meeting in February 2023 suggests that the Fed may be a bit less fearful of accelerating inflation and moving toward a less tight monetary policy stance.

The next section of this article explores the relationship of in-place rates to inflation. In-place rates are for those residents already living within a property and often adjust annually to take into account rising costs of goods and the provision of care services. The in-place residents generally make up the majority of residents in a stabilized property.

Year-over-Year In-Place Rate Growth and Pre-inflationary Times

Exhibit 1 compares this pattern of inflation growth with the year-over-year pace of growth in in-place rates for all care segments (independent living, assisted living and memory care). The pace of growth in rates generally stayed moderate and largely aligned with the inflation rate in 2020, but there was a notable shift in trend during the early months of the pandemic.

The exhibit shows that by mid-2020, year-over-year growth in in-place rates for the independent living care segment fell below the inflation rate, while growth in in-place rates for the memory care segment shifted to positive territory and experienced growth above the inflation rate. This could be explained by a rate adjustment to account for the increased care costs associated with the pandemic’s impact on high-acuity residents and needs-driven care settings.

By December 2020, in-place rates for the independent living care segment – frequently more of a lifestyle choice than need-driven – had the smallest increase and were up by 0.1% from year-earlier levels and continued to record the smallest increases since the trend shift occurred, followed by the memory care segment (up by 2.4% from year-earlier levels), and the assisted living care segment (up by 2.7% from year-earlier levels). Over the same period, the annual inflation rate stood at 1.4% in December 2020.

Year-over-Year In-Place Rate Growth During Inflationary Times

The vaccine rollout happened to coincide with the start of rising inflation in early 2021. Notably, inflation rates rose from 1.4% in January 2021 to 5.0% in May 2021 and stayed within the 5.0% range for five months. During this period, year-over-year in-place rates growth remained somewhat stable across all senior housing care segments. However, as inflation soared to unprecedented levels by the end of 2021 and began to impact the operating costs of senior housing operators amid relatively low occupancy rates, in-place rates across the three care segments started to increase and followed inflation rates, but this time remained lower than inflation rates.

In the first half of 2022, as inflation reached a boiling point, senior housing in-place rates rose to record highs from year-earlier levels across all senior housing care segments despite the market’s still relatively low occupancy levels in general.

By December 2022 and as the pace of inflation began to slow, in-place rates for the independent living care segment had an annual growth of 5.2%, the highest year-over-year growth in the time series, in-place rates for the assisted Living care segment grew by 5.8% year-over-year, but was down one percentage point from the highs seen in June 2022 (6.8%), and memory care in-place rates increased by 5.3% from year-earlier levels, down 2.6 percentage points from the time series high of 7.9% in October 2022. Comparatively, the inflation rate was 6.5% in December 2022, higher than in-place rate annual increases across all care segments.

Learn more about discounting of in-place rates relative to asking rates.

Section 3 – Uncovering Property-Level Insights for the First Time: A Deep Dive into Actual Rates Data.

Unpacking the Analytical Methodology

For the first since NIC MAP Vision launched the NIC MAP Vision Actual Rates Data Initiative, NIC Analytics conducted an in-depth analysis to examine the distribution of senior housing in-place rate growth across all senior housing care segments (independent living, assisted living, and memory care) at the property level, and the impact of these year-over-year increases on occupancy and absorption, as measured by the change in occupied units. Note that in-place rates are defined as the room fee and any care fees as of the end of the month paid by residents who took occupancy prior to the current month. Additionally, in-place rates include any discounting that may be occurring relative to asking rates.

The analysis was conducted using quintiles to examine the distribution of in-place rate growth in December 2022 from year-earlier levels on a same store basis. This methodology divides the data into five equal cohorts based on the distribution of percentiles and includes only those segments within properties that have reported data in both comparison months (December 2021 and December 2022). Properties reporting in one but not both months were removed from the analysis.

Additionally, this analysis centers on examining the relationship between in-place rate growth and demand as measured by the change in occupied units, or absorption and occupancy rates; it does not take into consideration supply trends, as it pertains to same-store metrics. Note that the change in inventory within the same store properties captured in this analysis was very small.

Independent Living Care Segments: In-Place Rate Increases and the Effect on Occupancy and Absorption

Exhibit 2 below shows how year-over-year in-place rate increases in December 2022 are distributed among the independent living care segments. The exhibit also illustrates the relationship between these increases and the growth in demand and average occupancy gains across the five quintiles in the same segment.

The data shows that for the independent living care segment – frequently more of a lifestyle choice than need-driven, the stronger the demand, the greater the pace of increases in in-place rates. Notably, annual increases in in-place rates are highly associated with stronger demand and improvements in occupancy rates. This makes sense from the simple laws of supply and demand dynamics. However, this is not the case for the assisted living or memory care segments.

In the two post-worst years of pandemic recovery, 2021 and 2022, properties with higher in-place annual growth rate generally maintained higher occupancy rates and experienced larger increases in both occupancy and demand or said another way, the most occupied properties were able to command the largest pace of growth for in-place rates. Conversely, independent living properties with lower in-place annual growth rate tended to have lower occupancy rates and experienced less demand growth, in general. This means that the lowest occupied properties had the most limited ability to grow in-place rates.

In-place rate growth across quintile five for the independent living segment, which includes the 20% of independent living segments within the 80th and 100th percentiles, experienced relatively stronger demand despite having the highest year-over-year in-place rate growth (equal or above 8.2% in December 2022). In fact, these segments reported a 3.2 pps increase in occupancy, from 83.8% in December 2021 to 87.0% in December 2022, mainly driven by an annual absorption rate of 4.3%, as measured by the change in occupied units. The same story applies to the independent living care segments within quintile 4 (the 20% of segments at the property level within the 60th and 80th percentiles in the distribution of year-over-year in-place rate growth).

Perhaps, not surprisingly, the median in-place rates in December 2022 across independent living segments captured within both quintiles four and five are also the highest rates — $3,968 and $4,079, respectively. Such relatively high rates suggest that these segments are likely within high-end properties, designed and built to provide a range of premium features and amenities to selective residents interested in exclusive lifestyle experiences and prime location, among other high-end features.

While high-end properties may offer a higher standard of living and amenities, residents can still become more resistant and sensitive to rate increases after a certain point, even if they can technically afford the higher rate. In fact, in December 2022, quintile five, which captures the highest rate increases, had relatively lower occupancy rates compared with quintile four. This was the case for the independent living care segments as well as for the assisted living care segments and memory care segments.

Conversely, the 20% of segments captured within quintile one, equivalent to the 20th percentile in the distribution, reported a negative year-over-year in-place rate growth (less than negative 0.1%) and had the lowest occupancy rates in both December 2021 and December 2022, at 72.5% and 74.4%, respectively. Interestingly, these segments reported a relatively larger occupancy gain (1.9 pps) and demand growth (2.7%) in December 2022 from year-earlier levels, compared with the second and third quintiles (40% of segments within the 20th and 60th percentiles in the distribution of in-place rate growth), but less than in the top two quintile tiers. In fact, the second and third quintiles reported the smallest demand growth and occupancy recovery.

The relatively lower median in-place rate for quintile one ($3,063) and quintile two ($3,080) suggests that these segments exist within properties that are designed and built to provide basic and less pricey housing for residents with lower incomes or those who choose not to spend their money on expensive housing. Additionally, the fact that these segments have negative in-place growth rates also suggests that their demand may have contracted more severely during the height of the pandemic, and to accelerate the recovery of occupancy, one potential option was likely to lower rates, or they may have been trying to buy occupancy.

Assisted Living Care Segments: In-Place Rate Increases and the Effect on Occupancy and Absorption

Unlike independent living care segments, the data in Exhibit 3 below suggest that there is negative correlation between in-place rate increases and demand growth/occupancy recovery in the assisted living care segments (more of a need-driven than lifestyle choice). This means that as year-over-year in-place rate increases get smaller, there is a stronger demand growth and occupancy recovery, on average.

Said another way, there is evidence that operators of assisted living properties bought occupancy by limiting rent growth, so to speak. That is, the lowest occupied assisted living care segments were able to generate new demand and grow occupancy faster, but this occurred largely because of minimal or even negative rent growth. And on the other hand, the highest priced assisted living units were able to command the most rate growth (nearly 12%), maintained relatively stable occupancy, but saw little net new demand.

More specifically, the assisted living care segments within quintile one, which refers to the 20th percentile of year-over-year in-place rate growth in the distribution (less than 0.9% – note that most of these segments reported negative in-place rate growth, equivalent to 17% of the total care segments count), experienced the strongest demand recovery and largest occupancy gains. Notably, occupancy within these segments increased by 6.3 pps, from 69.0% in December 2021 to 75.3% in December 2022, and occupied units grew by 9.5% over the same period. Despite the notable improvements in demand and occupancy, the lower 20% in the distribution continued to have the lowest occupancy rates across the board in both December 2021 and December 2022. This could be due relatively larger occupancy declines during the peak of the pandemic.

On the other end of the distribution, segments within quintile five, equivalent to the upper 20% of year-over-year in-place rate growth in the distribution (11.7%+), reported the smallest gains in demand and occupancy. Additionally, quintile five had relatively lower occupancy rate in December 2022 across all quintiles, with the exception of quintile one. This is likely due to steep rate hikes and suggests that it is vital to understand what current and potential senior housing residents are willing to pay and the potential impact of higher rate increases on the pace of move-ins and move-outs. Monitoring this relationship can help demand and occupancy recover faster, and inform the potential for future rate increases, especially as inflation eventually subsides.

Another important takeaway from this data is that the difference between the median in-place rate for quintile one ($5,092) and those of all other quintiles was the smallest across all senior housing care segments (about $500). This suggests that in December 2021, prior to the annual increases depicted in Exhibit 2 below, median in-place rates for assisted living care segments were somewhat aligned, but due to very low occupancy rates for quintile one, small and often negative increases were adopted to boost occupancy recovery.

Memory Care Segments: In-Place Rate Increases and the Effect on Occupancy and Absorption

The memory care segments (also a more need-driven than lifestyle choice) exhibited similar patterns as the assisted living care segments. The smaller the year-over-year in-place rate growth, the larger the demand growth and occupancy recovery. The highest priced memory care units were able to command the most rate growth (over 12%), maintained relatively stable occupancy, but saw little net new demand. Conversely, the lowest occupied memory care segments/properties were able to generate new demand and grow occupancy faster, but this occurred largely because of minimal or even negative rent growth.

Just like the assisted living care segments, the third and fourth quintiles had and maintained the highest occupancy rates in December 2021 and December 2022, although experienced a relatively smaller demand growth and occupancy improvements compared with the first and second quintiles. Additionally, quintile five, the equivalent of the upper 20% of year-over-year in-place rate growth in the distribution (12%+, the highest increase across all quintiles and care segments), reported a negative absorption rate of 0.1% and the smallest gain in occupancy rates across all quintiles and care segments. Further, quintile five had a relatively lower occupancy rate in December 2022 compared with the third and fourth quintiles. Again, this is likely due to steep rate hikes.

On the other hand, quintile one (year-over-year in-place rates below 1.1% – note than most of these segments reported negative in-place rate growth, equivalent to 16% of the total care segments count) had the strongest demand growth and the fastest occupancy recovery in December 2022 from year-earlier levels. Demand grew by 8.3%, and as a result, occupancy increased by 6.3 pps, from 73.5% in December 2021 to 79.8% in December 2022. Compared with quintile five, quintile one closed the occupancy gap from 8.5 pps in December 2021 to 2.6 pps in December 2022.

Notably, the difference in the median in-place rates in memory care segments between quintile one ($6,738 – least occupied segments overall) and upper quintiles four ($7,593) and five ($7,870) – most occupied segments overall, was the widest of all three care segments, with a gap ranging from $800 to $1,100.

Overall, the effect of in-place rate increases on occupancy and demand in all care segments is influenced by multiple factors, including the local market conditions, availability of options for residents with varying income demographics, the specific property and its amenities, and the perceived value of the unit in comparison to the competition in the area.

Interested in learning more?

To learn more about NIC MAP® data, powered by NIC MAP Vision, and accessing the actual rates data, schedule a meeting with a product expert today.

NIC MAP Vision welcomes your participation by contributing your properties’ data to the actual rates data set. Find out more by visiting NIC MAP Vision’s website.

Skilled Nursing Occupancy Remains Below 80%

NIC MAP Vision released its latest Skilled Nursing Monthly Report. The report includes key monthly data points from January 2012 through December 2022.

NIC MAP Vision released its latest Skilled Nursing Monthly Report on March 2, 2023. The report includes key monthly data points from January 2012 through December 2022.

Here are some key takeaways from the report:

Occupancy

Skilled nursing occupancy declined slightly, dropping one basis point from November to end December at 79.6%. Occupancy is up 182 basis points from one year ago in December 2021 as it continues to recover since the pandemic low of 73.6% set in January 2021. Occupancy has oscillated between 79.0% and 79.7% since May. Challenges do persist as staffing shortages continue to create difficulties within skilled nursing properties limiting the ability to admit new residents in some markets. However, the current occupancy trend does suggest that demand for skilled nursing properties is recovering, given the increase in occupancy in 2022. Occupancy remains low compared to February 2020 pre-pandemic levels of 87.8% (8.2 percentage points).

Medicare

Medicare revenue per patient day (RPPD) increased slightly from November to end December 2022 at $593. It has increased 3.1% since September. Most of this increase in reimbursement is likely a result of the increase in Medicare rates to skilled nursing properties for fiscal year 2023 and potentially higher acuity patients, which also increases RPPD to care for more complex patients. Meanwhile, Medicare revenue mix increased for the third month in a row. It increased 56 basis points from November to end December at 22.6%. It is up from one year ago as well, increasing 196 basis points from December 2021.

Managed Care

Managed Medicare revenue mix declined slightly, dropping 25 basis points from November to end December at 10.2%. It has declined 163 basis points since its recent high of 11.8% in February 2022. However, it is up by 171 basis points from the pandemic low set in May 2020 of 8.5%. Expectations are that it will continue to increase over time with the growth of managed Medicare. Meanwhile, Managed Medicare revenue per patient day (RPPD) decreased from $473 to $472 in December and is down 1.2% from last year in December 2021. It has decreased $120 (20.2%) from January 2012 and continues to pressure some operators’ revenue as managed Medicare enrollment grows around the country. However, some operators see managed Medicare as an opportunity for growth in patient volume.

Medicaid

Medicaid patient day mix decreased to 63.8 % in December. However, it has increased 175 basis points from the pandemic low of 62.1% set in January 2021. In addition, Medicaid revenue mix decreased in December, representing just less than half of property revenue at 49.4%. However, it has increased 210 basis points from the pandemic low of 47.3% set in February 2022. Meanwhile, Medicaid revenue per patient day (RPPD) declined slightly to $265 in December. It increased 0.73% from $263 one year ago in December 2021.

The report provides aggregate data at the national level from a sampling of skilled nursing operators with multiple properties in the United States. NIC continues to grow its database of participating operators to provide data at localized levels in the future. Operators who are interested in participating can complete a participation form on our website. NIC maintains strict confidentiality of all data it receives.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. NIC's privacy policy can be viewed here. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.