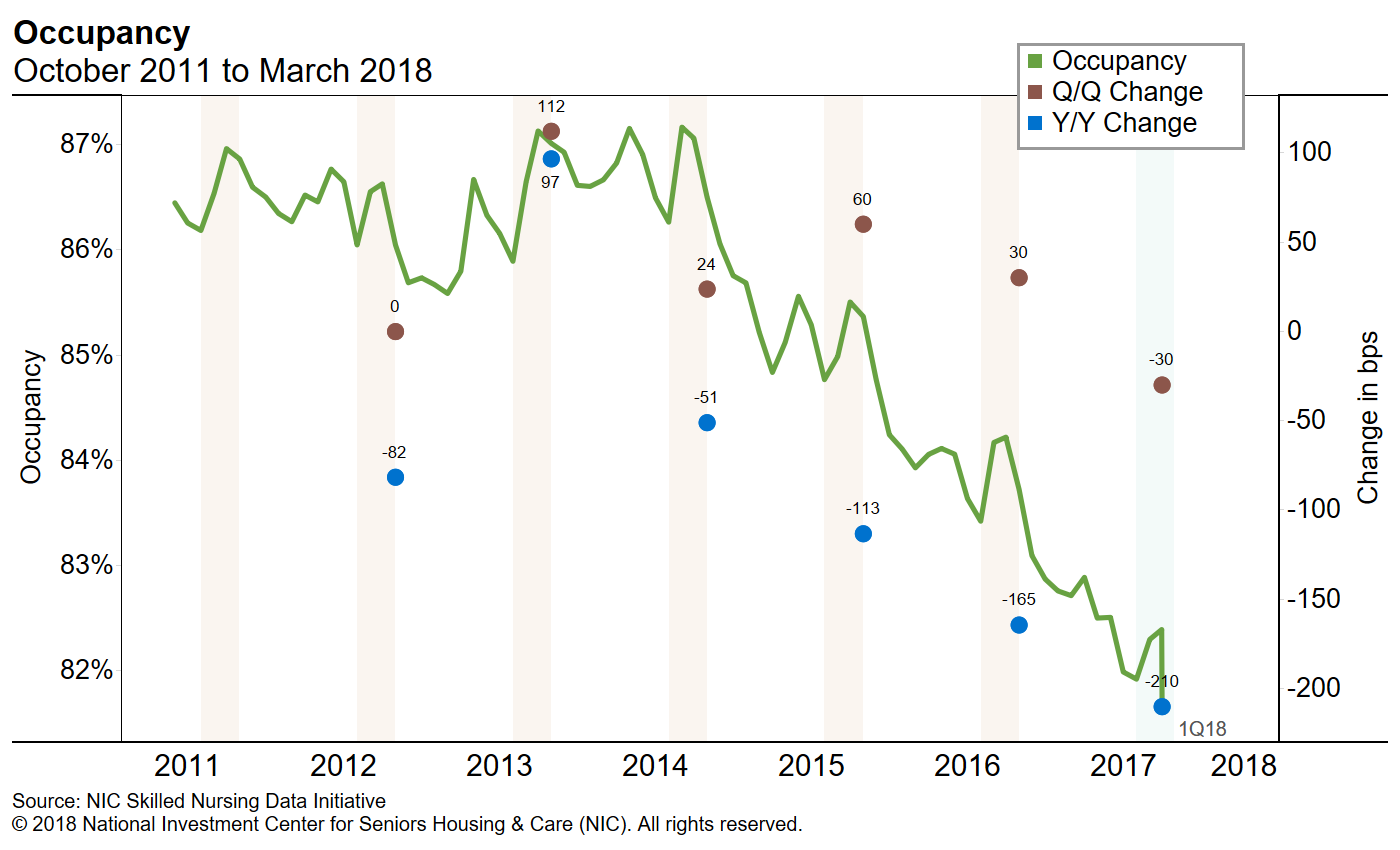

- Occupancy Continues to Fall, Despite Typical Seasonal Influence

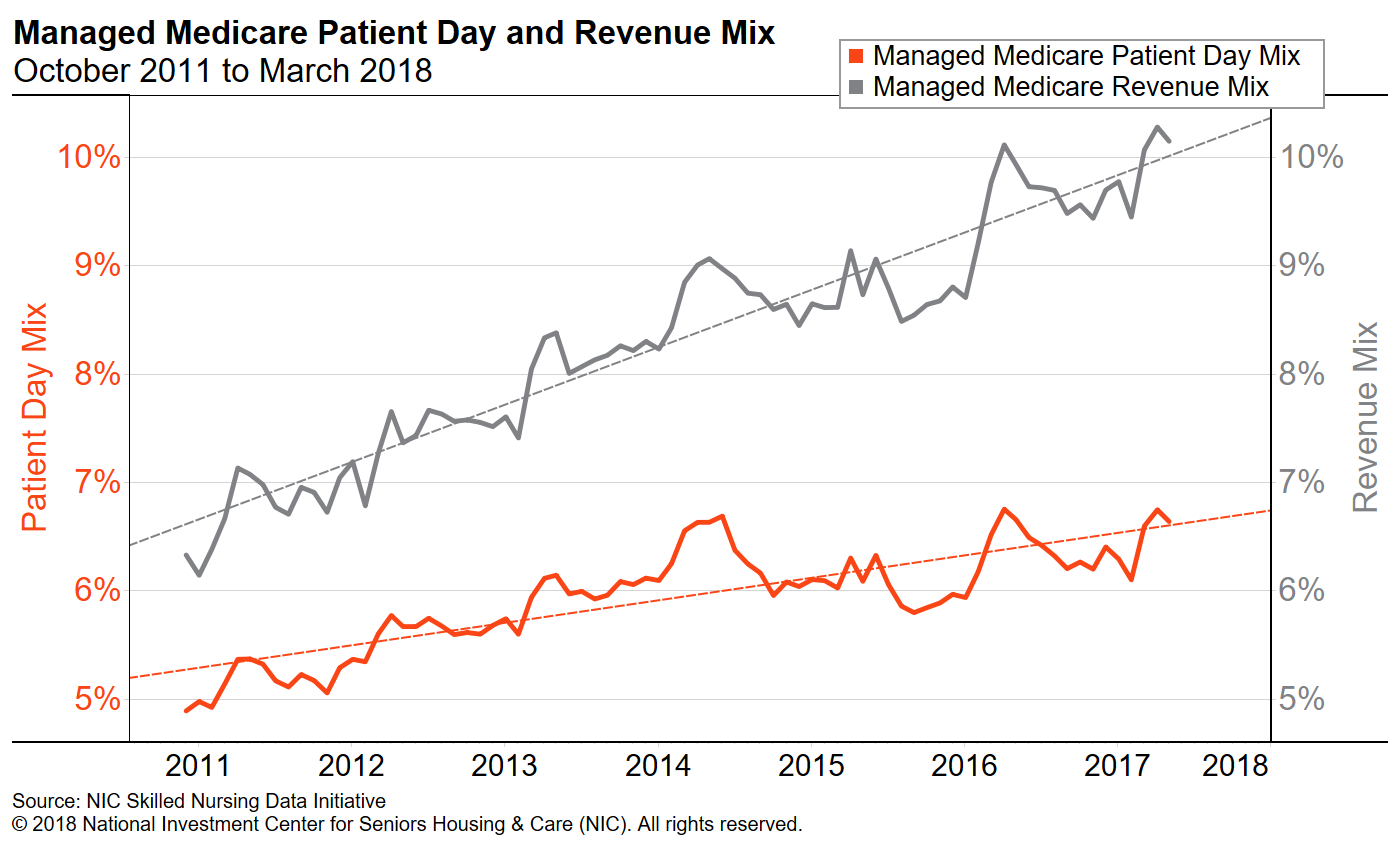

- Managed Medicare represents increasingly larger share of skilled nursing revenue

NIC released its first quarter 2018 Skilled Nursing Data Report last week, which includes key monthly data points from October 2011 through March 2018.

Here are some key takeaways from the report:

- First quarter national occupancy decreased 30 basis points from the fourth quarter to 81.6%, deviating from the expected historical trend which usually shows an uptick in occupancy from the fourth to the first quarter. Occupancy initially increased in both January and February before slipping back in March. March 2018 occupancy was down 210 basis points from the March 2017 rate of 83.7%. Occupancy declined on a year-over- year basis for both urban and rural areas, while it increased for urban cluster properties from the prior quarter.

- Skilled mix increased at the national level from the prior quarter as Medicare and managed Medicare patient day mix increased 56 and 54 basis points to 13.0% and 6.6%, respectively. This suggests that seasonality did influence the data as higher acuity patients are often admitted during the winter/flu season which in turn often drives an increase in overall occupancy. However, as overall occupancy decreased there may be other factors at play which are offsetting this influence such as pressures on admissions or length of stay. Skilled mix increased across all reported geographic areas in urban, rural, and urban cluster markets. Rural area properties are now at the highest level of skilled mix within the time-series, ending the quarter at 24.4%.

- Managed Medicare revenue mix reached a time-series high at the national level in February 2018, demonstrating the growing influence of this payor source. Even among rural properties, where revenue mix for managed Medicare is less than half the revenue mix reported in urban areas, the trend is consistent. Rural areas have been less affected by managed Medicare than others, but the trend warrants attention in the years to come, in all geographic areas. The revenue per patient day (RPPD) from managed Medicare continued to decrease from the prior quarter in all areas, except for urban cluster where it increased slightly.

- Medicare revenue mix increased in the first quarter and was close to the highs of one year ago in urban cluster and rural settings. While the Medicare revenue mix for urban area properties was up quarter-over-quarter, at 23.7%, it was far below previous first-quarter highs of approximately 28% last seen in 2015. Year-over- year, urban area Medicare revenue mix declined 157 basis points from March 2017. It is now down a total of 474 basis points over the past three years.

- Nationally and consistently across geographic areas, private revenue per patient day continues to increase, with the fastest growth in rate occurring in rural and urban cluster areas. Nationally, private RPPD reached a six-year high of $262 in February 2018 before ending the quarter at $260. Revenue mix for private revenue reached a six-year low at 7.7%, as the share of private revenue continues to drop.

The NIC Skilled Nursing Data Report is available at http://info.nic.org/skilled_data_report_pr. There is no charge for this report.

The report provides aggregate data at the national level from a sampling of skilled nursing operators with multiple properties in the United States. NIC continues to grow its database of participating operators in order to provide data at localized levels in the future. Operators who are interested in participating can complete a participation form at http://www.nic.org/skillednursing. NIC maintains strict confidentiality of all data it receives.