Diverse Senior Housing Investment Opportunities Across the Risk Spectrum

Keen senior housing investors have a growing pool of opportunities that span the risk spectrum, at dislocated pricing, set against the backdrop of one of the most compelling fundamental stories in the real estate sector. This dynamic may accelerate in the coming months as several compounding forces coalesce to motivate sellers to strategically evaluate options, including to transact.

What is Currently on Market

The majority of deals on market can be widely categorized into two major groups: operating performance-driven and capital stack-driven.

Operating performance-driven sales encompass: 1) newer vintage assets, delivered just before or during the pandemic, experiencing a protracted or stalled lease-up, 2) older vintage assets that have lost market positioning, or 3) assets in currently saturated markets where supply has outstripped demand. Addressing the underperformance can involve resetting loan-to-values, requiring additional capital infusion, sales by tired equity capital, or sales by lenders who have lost confidence, in some cases accepting discounted payoffs.

Capital stack-driven sales, on the other hand, stem from challenges in capital composition. On the equity side, end-of-fund life issues, showcasing wins for the next fund raise, or addressing redemption backlogs is leading to sales. On the debt side, near-term maturities, expiring interest rate hedges, and a sudden increase in the cost of debt, are driving sales despite otherwise performing operations.

What to Expect for 2024

The capital markets have remained tight to start off the year. Sellers anticipating a downward trend in the UST 10Yr have witnessed a reversal in fortunes so far. As a recent Wall Street Journal article aptly titled “Investors Are Almost Always Wrong About the Fed,” sellers waiting on favorable capital markets may have to contend with a different reality. Coupled with mounting capital challenges on both the debt and equity fronts, this may accelerate the opportunities outlined earlier.

In addition to the prevailing factors, several other forces are set to intensify and converge in the coming months that may drive deal volume. First, according to NIC, there are $18 billion of senior housing loans maturing in 2024 and 2025. Second, expiring interest rate hedges in a still-elevated rate environment are straining levered free cash flows. Third, senior housing continues to garner interest from institutional equity, attracting both new entrants that have already signaled allocations and a reinforced commitment from existing groups. According to JLL Research, there is $402 billion of dry powder waiting to be deployed in commercial real estate. Given the attractive risk-adjusted-return profile for senior housing, there may be an escalating number of newcomers to the space which could fuel an even larger appetite for deals.

Investors who do transact stand to benefit not only from dislocated pricing, but also from participating in the positive fundamental growth story unfolding in the senior housing sector. Operational metrics continue an upward trajectory, with occupancy in the NIC MAP Primary Markets reaching 85.1%, marking the tenth consecutive quarter of gains. Occupied units in primary markets sit at ~599K – ~30K units higher than pre-pandemic.

In terms of supply, the backlog of delivering product continues to shrink while new starts continue to dwindle due to debt availability and still elevated construction costs. Construction starts were 2,221 units for the Primary and Secondary Markets in the fourth quarter 2023 – the lowest number since the second quarter 2009. Contractor bids remain elevated in a still tight labor market for skilled workers. The costs for raw and finished goods have seen some relief recently, but it may be short lived as geopolitical pressures have caused notable disruptions in the global supply-chains. Trans-Pacific shipping rates surged 24% sequentially in the week ended January 31st, according to the Drewry Hong Kong-Los Angeles benchmark. This index is up 338% from last year. Combined with lowered loan-to-costs, the substantial decrease in starts is likely to persist for the near future. On the demand side of the equation, in recent research by NIC MAP Vision, it was reported that to maintain the current market penetration rates, the sector will need 806,000 additional units by 2030.

The dynamics in play are set to create an active transaction environment in 2024 for investors spanning the cost of capital spectrum amidst increasingly favorable fundamentals with tailwinds for the foreseeable future.

2024 Presents a Golden Opportunity to Increase Occupancy Amid Favorable Market Dynamics

Amid favorable supply and demand market dynamics, 2024 presents a golden opportunity for senior housing communities to bolster occupancy rates and drive operational growth, thereby mitigating some of the challenges posed by capital market conditions.

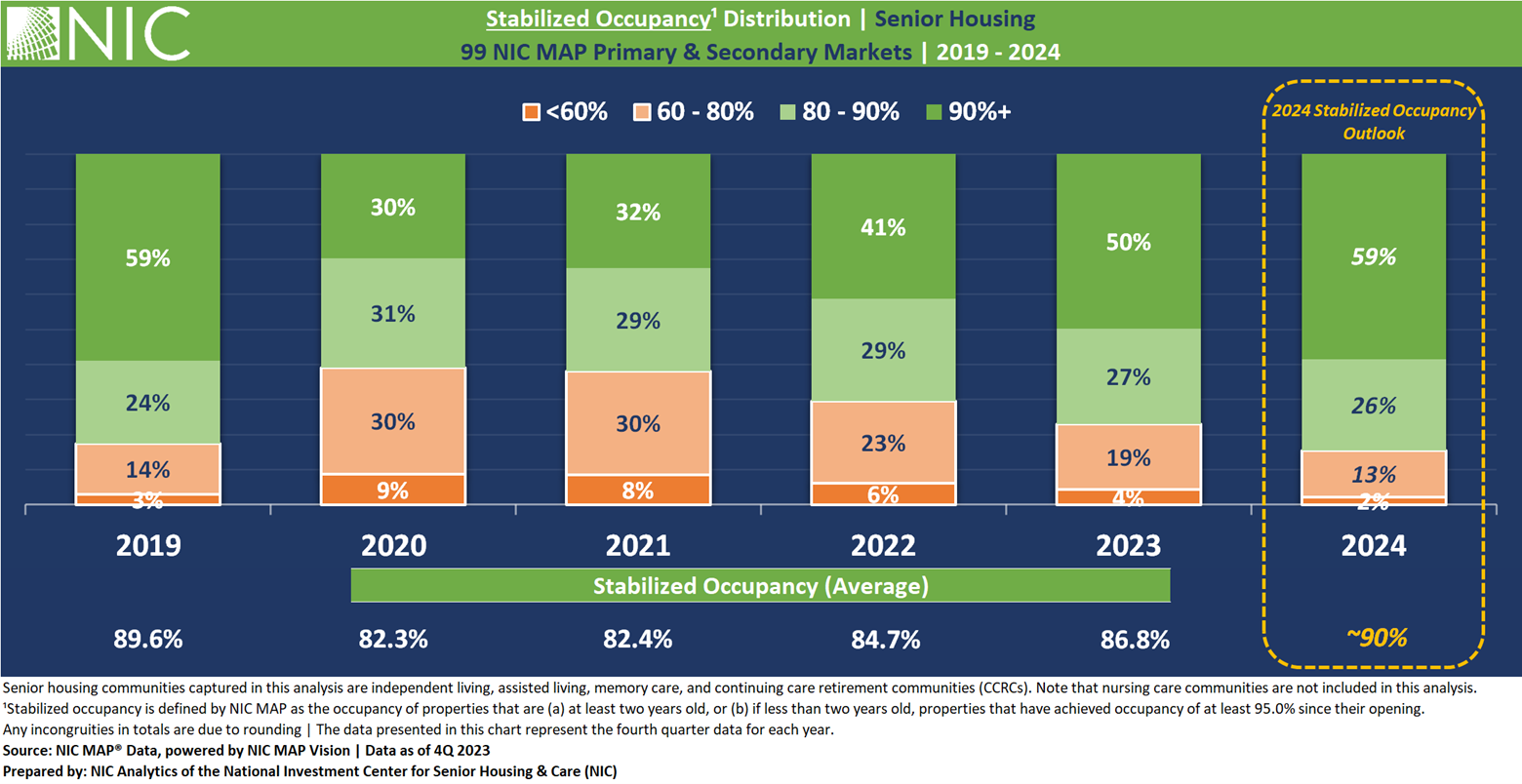

NIC Analytics recently published its first occupancy stratification report, focusing on the stabilized occupancy¹ distribution within the senior housing sector in 2023. The report reviews how senior housing communities are faring after 10 quarters of occupancy growth and recovery, fueled by a combination of robust demand and moderate new supply, reflected in the absorption to inventory velocity (AIV Ratio).

The report offers an outlook for stabilized occupancy in 2024 and examines stabilized occupancy distribution in 2023 across various dimensions, including NIC MAP market aggregates, regional variations, chain sizes, community types, payment types (CCRCs), community sizes, community ages, campus types, and profit statuses. Additionally, it provides occupancy distribution across select NIC MAP Primary and Secondary Markets.

The past three years have seen a remarkable resurgence in demand for senior housing as the markets registered the strongest unit improvement in net positive absorption, as measured by the change in occupied stock, since NIC MAP began reporting the data back in 2005. Not surprisingly, however, the pace of occupancy recovery varies across communities, markets, and other dimensions tracked by NIC MAP Vision.

2024 Stabilized Occupancy Outlook: Average and Distribution.

In 2019, prior to the onset of the pandemic, 17% of senior housing communities in the 99 NIC MAP Primary and Secondary markets had stabilized occupancy below 80%. While the sector has made notable strides in occupancy recovery and is on record to return to and surpass pre-COVID occupancy levels by the end of 2024on average, there remains a group of communities that continue to face challenges.

Specifically, 23% of senior housing communities are still reporting occupancy rates below 80% as of the fourth quarter of 2023. Such stabilized occupancy levels below 80% are likely to pose challenges, particularly given the current capital market conditions and the resulting lending environment as well as higher operating costs.

The NIC Analytics outlook for 2024 suggests a notable improvement in the overall stabilized occupancy distribution by the fourth quarter. Notably, 85% of senior housing communities are expected to have occupancy levels of 80% or higher by the fourth quarter of 2024, slightly exceeding the share seen in fourth quarter 2019. In contrast, 13% are expected to remain within the 60–80% occupancy range, while another 2% are expected to have occupancy below 60%.

By the fourth quarter of 2024, the stabilized occupancy rate for senior housing communities in the 99 NIC MAP Primary and Secondary Markets is expected to reach approximately 90% on average.

Capitalizing on 2024 to Increase Occupancy and Align with the Broader Trend of Occupancy Recovery

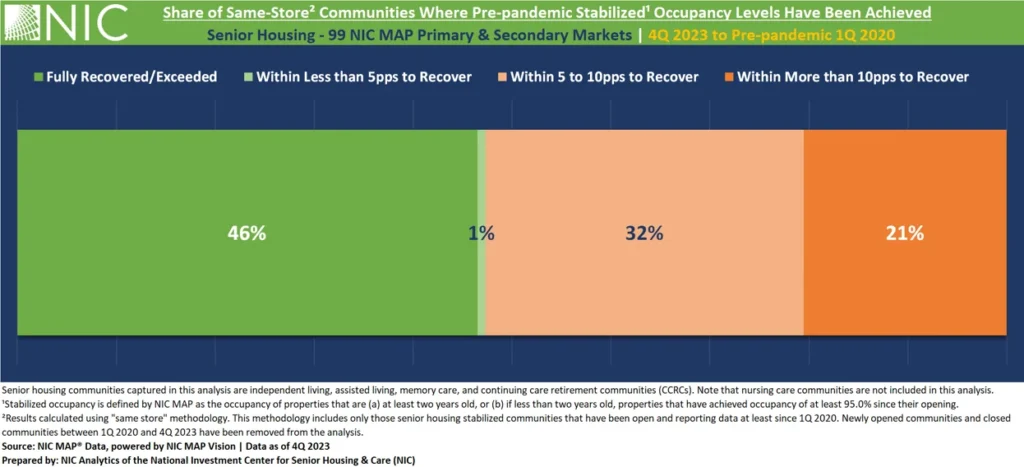

Since the first quarter of 2020, NIC Analytics has been tracking the recovery of stabilized occupancy across the 99 NIC MAP Primary and Secondary Markets by looking at the share of “same-store” senior housing communities that have achieved pre-pandemic stabilized occupancy levels and those that are still in the process of recovery. Same-store is defined as senior housing communities that have been open and reporting data at least since 1Q 2020. Within the 99 Primary and Secondary Markets, a total of 7,521 same-store senior housing communities were identified. Closed and newly opened properties since 1Q 2020 have been excluded from this second part of the analysis.

The exhibit below shows that 1Q 2020 stabilized occupancy levels have been achieved or surpassed as of 4Q 2023 in nearly half (46% – equivalent to 3,500 communities) of same-store communities within the 99 Primary and Secondary Markets. Additionally, a marginal 1% of communities are within less than 5 percentage points (pps) of returning to their pre-pandemic occupancy rates.

By contrast, as of 4Q 2023, roughly one third of communities (more than 2,400) still lagged behind their 1Q 2020 stabilized occupancy levels, with a 5 to 10pps range of recovery. Additionally, 21% of communities (more than 1,500) still have a gap of over 10pps to bridge in order to reach 1Q 2020 occupancy levels.

While each of these communities faces its unique set of challenges contributing to a slow recovery process, overarching challenges and opportunities emerge at the market level.

Competition from New Entrants: The emergence of newly opened communities presents competition, capturing a portion of the market share and potentially prolonging the occupancy recovery process for some stabilized communities.

Leveraging Favorable Market Dynamics to Increase Census: Amidst record levels of demand and moderate new supply expected to continue through 2024, senior housing communities with lagging occupancy rates are presented with a prime opportunity to capitalize on market dynamics and enhance census and occupancy levels.

While currently construction starts are low and inventory growth remains moderate, consensus suggests a regained pace by the end of 2024. Consequently, competition from newly opened properties is expected to grow.

2024 presents a golden opportunity to increase occupancy amid favorable market dynamics.

¹Stabilized occupancy is defined by NIC MAP as the occupancy of properties that are (a) at least two years old, or (b) if less than two years old, properties that have achieved occupancy of at least 95.0% since their opening.

Industry Legacies: Parents Pass the Baton to the Next Generation

A Conversation with Lynne and Andrew Katzmann

This article is the first in a series showcasing parent/child duos across the senior housing and care industry. My conversation with Lynne Katzmann of Juniper Communities and her son, Andrew Katzmann with Columbia Pacific, offers insights into why this is becoming a common trend.

Growing up, I thought I understood what my dad, Alan Zuccari, did for a living. Now, as a second-generation member of Hamilton Insurance Agency, I have gained a newfound appreciation for his career. Working with my father has given me the opportunity to absorb the industry’s history, including its successes and evolving challenges. I’ve learned what kept him motivated then and continues to do so now—through even the most complicated markets—is the end user.

Our work, like that of the fellow professionals I highlight in this series, contributes to a larger ecosystem of caring for seniors. At the core of this industry is giving the generations before us the reverence and benefit of living a happy last chapter. Each of us feel a strong sense of responsibility to the mission of our individual companies and that of the greater community.

From owners to operators, vendors to lenders, and everyone in between, we all know firsthand this is not a field for the faint of heart, yet people from my age group and the one upcoming don’t shy away. This interview series seeks to shed light on what keeps us all coming back and following in our parents’ footsteps.

Lynne Katzmann is the founder and CEO of Juniper Communities, which invests in, develops, and manages senior living and long-term care communities. Juniper is the only woman-founded, owned and led business among the top 40 national assisted living companies. Its portfolio consists of 22 properties in three states and more than 1,600 employees.

Lynne was the first winner of the McKnight’s Women of Distinction Lifetime Achievement Award and was inducted into the American Senior Housing Association’s Hall of Fame. She holds a Ph.D. in economics from the London School of Economics.

Andrew Katzmann is Vice President at Columbia Pacific’s Real Estate Strategies division. He focuses on healthcare and senior housing sector investments. Previously, Andrew worked as an analyst for LTC Properties, a real estate investment trust centered on senior housing. Andrew holds a B.A. in economics from Tulane University.

Tell us about yourself and your work.

Lynne: I’ve been at Juniper for 35 years, but I started out in the senior care industry doing Medicare demonstrations and working in value-based care. I wrote a state health plan for Oregon, then went on to help run a public company that doubled its value in a couple of years, before it was sold and taken private.

I have experience in operations, finance, and I’m a health policy wonk by training. Juniper is an owner/ operator with a committed group of angel investors who’ve been with us since inception. Our structure is unique compared to companies with outside capital that limits them to certain requirements—it has enabled us to innovate, which I’m passionate about.

Andrew: Although I’ve been in proximity of Juniper my entire life, my professional career began in senior housing eight years ago. Out of college, I worked at LTC Properties in Southern California cutting my teeth on the capital, triple net side. A few years later, I transitioned to Columbia Pacific Advisors, which owns a number of senior housing establishments across the country. Being private equity focused, it’s a little bit different but still on the capital side. Instead of triple net, it’s the REIT Investment Diversification and Empowerment Act which gives us more operational influence. Growing up around Juniper and being in and out of buildings with my mom gave me a pretty good viewpoint and taste for the complexities of operations.

What do you see for the future of the senior care industry?

Lynne: I think it’s an extremely exciting time for the industry. While things have changed a lot in my 35 years, I envision more change happening at an accelerated pace. Why? Because I’m the next consumer, and I don’t want what we have today. If for no other reason, I want someone to develop something new and different so that I fall in love with the experience, yet again.

The demographics show huge growth and a massive untapped market. Right now, senior living is only 10-12% of the entire senior market so tremendous opportunity exists. But it requires us to look at things differently. I’m excited for the next generation to come in, learn, bring new ideas to the table, and most importantly, provide new energy.

Andrew, what have you learned from Lynne?

Andrew: Working in the same industry as a parent, especially one who’s built their own company from the ground up, has been a real privilege. Having her perspective through my professional career has been invaluable. I’ve learned so much from my mom, but it was really highlighted during COVID-19 and through the current debt environment. She was able to offer perspective from the people doing the work, day in and day out. I spend most of my time analyzing numbers and having broad conversations, so that boots-on-the-ground insight of what’s going on in the buildings sheds light on what pushing the census in a new environment really looks like.

As she mentioned, this is a very interesting time in senior housing. There is a lot of opportunity and so much to be gained, both financially and educationally. To change our reputation as an industry right now depends on how we move forward. I’m grateful to have my mom’s wealth of expertise on speed dial as we tackle new challenges.

What’s your advice to the next generation, Lynne?

Lynne: I think the key for the next generation will be rebranding senior living. We need fresh insight and updated messaging to reinforce how important the work we do is. How people think about senior living needs to change. It won’t necessarily change what we do on a daily basis, but it will alter how employees and consumers talk about it.

Most people associate our work with the final stage of life, which is not where they want to focus time and energy. They also think of us as caregivers. Through COVID, we were raked through the coals as part of that post-acute continuum. The industry has a lot to overcome in addition to societal issues with ageism, death, and dying. I think the biggest challenge and the greatest opportunity is to start thinking about how we evolve from the real estate model and that requires a major shift in how we brand ourselves as an industry.

The next generation will need to manage change. They’ll have to think differently, creatively, and be solution oriented. Most importantly, they’re going to need grit, passion, perseverance.

What’s your advice for the previous generation, Andrew?

Andrew: It’s an interesting question. I’m very proud of where I come from. Those who know my mother know she’s very forward thinking. One of my biggest takeaways from COVID is the old adage: ‘those who don’t study history, are doomed to repeat it.’ If you keep doing what you’re doing because you’ve made a lot of money or you’ve built a company that way, there’s not much room for future growth.

Changing the perception of the industry like Lynne mentioned is not going to happen if you just keep doing the same old thing. From where I sit, my advice is—you’ve done a good job in the past, but that’s not where we are now, so keep evolving. The same goes for our generation and those younger than us.

How do you recommend we make the right calculated decisions as we move forward?

Lynne: We have more data than we had before. Better information equals better decisions. Additionally, it’s about evolution, not radical change. The only thing that needs to radically change is how we talk about who we are.

Andrew: Everything we’re talking about—how both groups draw on the experience of one another and tap a desire to do something different and try something new. That’s where having a parent in the industry is very valuable.

You’re not always going to agree, and that’s the beauty of it. things We’ll always see things based on our knowledge. There’s no shortcut for experience.

When it comes to talking about work, do you have boundaries so that it doesn’t always bleed into dinner table talk?

Andrew: We work a lot. Our jobs are very much a part of our lives, so the personal and the professional definitely bleed into one another. We never run out of things to talk about. Our conversations span the spectrum, from celebrating wins to troubleshooting challenges. I love it!

Lynne: I love it, too. It’s such a joy to have a multidimensional relationship with your child. Andrew understands what I do with my time. I understand what he does with his. How cool and rare is that? My father was an electrical engineer. I understood his work in a general sense, but I couldn’t connect with him about it in any meaningful way. This is just another way for us to relate. It’s fun, it’s great, and it’s enriching.

The Medicare Advantage Landscape: Plan Consolidation and Proposed Rate Cuts Impact Care Providers

In 2023, Medicare Advantage (MA) enrollment surpassed traditional fee-for-service Medicare enrollment for the first time in the program’s history, with more than 30 million seniors—51% of the Medicare population—now enrolled in a private plan. While MA plans can boast lower 30-day hospital readmission rates and fewer avoidable hospitalizations for their members, the increasing penetration of MA plans is a trend that senior housing and care providers should monitor closely.

Medicare Advantage plans routinely contract with health care providers—including assisted living and nursing care operators—for services. These plans control which care providers are in their networks as well as the characteristics of their contracts.

MA Plan Consolidation and Rate Cut Implications for Care Providers

When a single MA plan has considerable penetration in a given market, their contractual offerings to a post-acute care provider may not cover the costs of basic custodial care, let alone the more intense care provided within a skilled nursing setting. For post-acute care providers, this can present a lose-lose situation. While their costs may not be covered due to contractual payment limitations, not accepting a contract offer could result in inadequate service volume, leading to lower occupancy and further financial strain.

Simultaneous to MA enrollment reaching its highest level, the number of MA plans available to eligible seniors fell for the first time ever, with fewer plans available to choose from in 2024 than in 2023. With smaller plans exiting the market, larger MA organizations further consolidate, resulting in more limited competition and diminished negotiating power for providers.

An additional challenge facing the marketplace is a proposed 2025 rate reduction in the Medicare Advantage base payment rate which, if finalized, would mark the second consecutive year with a lower benchmark rate. The response from MA insurers will likely be increased premiums and a reduction to enrollee benefits and provider reimbursement.

One-fifth of Medicare beneficiaries discharged from a hospital receive post-acute skilled nursing care. In the Medicare Advantage plans, skilled nursing providers are much more likely to encounter prior authorization requirements for necessary drugs and treatments. These authorizations often lead to delays in care and in some cases are denied for reimbursement. Post-acute providers have long decried the burdensome prior authorization process and high denial rates experienced with Medicare Advantage plans.

Navigating the MA Landscape by Care Providers

There are moves that providers can make to better navigate this MA landscape. First, ongoing advocacy related to prior authorization and the high rate of denials is needed. A number of groups continue to push federal officials to further scrutinize these denial patterns. Second, there are a number of providers who have entered value-based care arrangements themselves. Some have formed their own Medicare Advantage plans as owners while others have joined a network with others to share in risk. This puts the provider in a greater position of upside risk for delivering positive outcomes for their residents. Last, it is imperative that provider organizations are sophisticated in demonstrating their value through prevention and wellness efforts that result in cost savings and better outcomes for their residents.

With the CMS goal to have all Medicare-eligible individuals enrolled in a value-based care relationship by 2030, it is anticipated that these MA trends will only increase in the next several years. Providers need to stay on top of these trends, understand their local markets, and explore where they can participate in value-based care arrangements to better position for success and viability long-term.

If you’re attending the 2024 NIC Spring Conference in Dallas, mark your calendar for two informative main stage sessions you don’t want to miss: “Orchestrating the Future of Medicare and Medicaid for Senior Living Operators,” on March 5 at 4:00pm, and “Medicare Priorities and Programs” with Dr. Meena Seshamani, Director of the Center for Medicare and Deputy Administrator of CMS, on March 6 at 9:30am.

Exploring the Potential of Multigenerational Living and Learning: A Conversation with Anne Doyle

How to reimagine senior housing in partnership with higher education.

What does it mean to bring an explorer’s mindset to the redesign of senior housing?

Anne Doyle, CEO of Spark Living and Learning, shares exciting new ideas here on how to develop a learning culture to attract the next generation of residents. Partnerships with local colleges or universities can provide unexpected benefits such as employee sourcing, expense management, educational enrichment, and engagement with the wider community.

NIC Co-Founder and Strategic Advisor Bob Kramer interviewed Doyle at the 2023 NIC Fall Conference. What follows is an edited version of their conversation. The discussion offers relevant context and detail on how to leverage the benefits of higher education to create an aspirational community—one where people want to live.

View Anne Doyle’s NIC Talks presentation on multigenerational living here:

Kramer: You had a revelation on a recent vacation. Can you tell us about it?

Doyle: This past summer I had the opportunity to kayak in the Artic on the west coast of Greenland. Being in a remote place surrounded by massive glaciers and huge icebergs thousands of years old made me think about the senior living industry and the short time we have on this earth in comparison to our natural world. It put into sharp focus the importance for us to make the most of our time here and not think that those later years as ones to just slide through.

Kramer: It sounds like you realized the importance of intentionality in thinking about our later years.

Doyle: Absolutely. Before I went kayaking in the Artic, I thought all icebergs were the same. But I saw that they’re all different, with a variety of shapes and hues. Most people think those who are older are similar. But we know people at 55, 65, 75, or 85 are incredibly different and each of us is different.

Kramer: How does that relate to senior living?

Doyle: This applies to the individuality of people in their later years and how to develop choices for older adults. I’m excited about opportunities to create intergenerational communities. How do we take this incredible opportunity considering the diversity of people, backgrounds, and interests to help them make the most of their lives?

Kramer: People might be familiar with your work at Lasell Village and think that being located on a college campus is the only way to partner with higher education. What would you say to them?

Doyle: Lasell Village is a great example of a way to bring people together. Lasell Village is a fully integrated continuing care senior living community on the campus of Lasell University in Newton, Massachusetts, outside of Boston. About 300 people live there across all levels of care. When residents move in, they agree contractually to have 450 hours a year of education. This model may not work in most places, but there are opportunities to tailor communities to different campuses.

Kramer: Why is this the right time?

Doyle: Higher education faces a declining birthrate and reduced customer base, while our industry faces an exploding customer base. There is an opportunity to match the puzzle pieces. Universities have a big interest in serving more people, and they have high fixed costs. Universities can benefit from a relationship with senior living.

Kramer: What are the benefits for residents? Does a community affiliated with a college or university appeal to a wide swath of people?

Doyle: There are clear benefits to individuals. Some are seeking purpose, or new educational opportunities. Maybe they’re interested in learning a new language, or in a different field of study. Maybe they want to retool their skills while they continue to work. If we have the benefit of a long life, those extra 20-30 years could give us the ability to have an extra career or pursue a new interest.

Kramer: What are some of the different models that combine senior living and higher education?

Doyle: There are fully integrated communities like Lasell Village where the community is embedded on the campus as well as communities that are associated with a college or university. The model could include all different types of housing. It could be a co-housing model with families. It could be an affiliation with a secondary school, cultural organization, or performing arts center. We have to think intentionally about how to partner with assets in the wider community.

Kramer: What are the multi-generational opportunities that might make this model attractive to the college or university?

Doyle: When thinking about young people, they need work and senior housing offers work opportunities in hospitality, clinical sciences, marketing, and other areas. There is also the opportunity to develop intergenerational friendships when people are naturally together, say volunteering at a day care center on campus, in class together, or at the art studio. Friends can be made anywhere. Those relationships help address not only a concern in senior housing but also among those caring for young people. The perspective of older adults when a young person is stressed out can help mitigate mental health challenges and colleges don’t have enough mental health practitioners. Friendships across the life space can really make a difference.

Kramer: What is the value proposition for older adults, investors, operators, the university and for the college age students themselves?

Doyle: There are a lot of stakeholders in this puzzle, and I would add another, the workforce itself. As I mentioned, students need to work. The smart senior housing organization will develop a strong relationship with the university or college so students can work at the community or continue their education through capstone projects. Student workers surrounded by a professional support group and mentors are likely to have longevity with that senior living organization. Retention benefits the business, the students, and the older adults who see and get to know the student worker over a longer period of time.

A second benefit is expense management. Senior housing and higher education have a similar infrastructure. We have workforce expenses, property, dining services and amenities. We can get creative about how to leverage each other’s resources. For example, we could buy IT services from each other and reduce our costs. Finding a way to pool our backend services really makes a lot of sense.

The third benefit is that a college or university campus just naturally provides engagement every day. Communities serving older adults are constantly trying to up their game in terms of engagement and education. A university campus offers ever changing lectures, classes, and events.

Kramer: What questions should senior living leadership be asking about their own goals that might inform new partnerships?

Doyle: Start by asking: How do you want to live when you are 75, 85, 95 or 105? If we really honestly answer that for ourselves, then we realize all the things we want to do. Our group who went to Greenland was in their 60s and 70s. It was cold. The wind ripped our tent in half. But we found it totally exciting. We need to design our communities for what we are interested in and not what we think other people are interested in. Maybe you’ve never had an opportunity to learn a musical instrument, and you’d like a place that has a relationship with a music conservatory. If we are intentional about what we want to do and who we want to do it with, there are so many possibilities. We’ll get a lot more creative and build better communities.

Kramer: What’s the value add of the university community compared to a traditional senior living community?

Doyle: The value add is having a pool of customers who want to move into your community. We know that we’re not that excited about moving to communities where our parents have lived. If we continue to replicate that model, we will have occupancies that continue to reflect that. Be honest about what interests us and our friends, and build for choice. The value comes from prospective residents who say this is a place I want to live and live for a longer time.

Kramer: One of the issues in our industry is whether we are an avoidance setting or an aspirational setting. An avoidance setting is one in which I want to do everything I can, so I don’t end up being forced to move there. An aspirational setting is a place to explore new things, and a university is a great setting for that. I like to say lifelong learning is learning for a long life. How do you view the connections between universities and senior housing?

Doyle: I absolutely see the connections between higher education and senior living as aspirational. People choose to move in because they want to be in a community of curious people, and in a diverse community—people with different professional, racial, cultural, and geographical backgrounds.

People often move to senior living close to where they’ve been living. But in my experience, a university or college connection creates a buzz around the opportunity for change. It’s like new college students who are open to all the possibilities on campus. I’d like to frame our communities as ones of possibility not of restrictions. We have that within our means.

Kramer: How do these partnerships challenge the prevailing paradigm about getting old and aging?

Doyle: I have a 91-year-old friend who says a healthy attitude leads to a healthy mind and body. This is from someone with many health issues. We can create communities that are about opportunities and not restrictions. We can support each other in a shared culture that believes we can do the things we want to do even with cognitive and physical decline.

Kramer: As senior living leadership thinks about their own goals and pursuing partnerships with universities and colleges, what advice would you give them? What questions should they be asking themselves?

Doyle: I led senior living on a campus, and we experienced tremendous success coming out of COVID with a large waitlist. Residents were engaged in education. Senior living leaders need to recognize that it often takes more intention to work with a university. The business objectives of the senior living community and the university must be 100% aligned. As I said before, the college may be suffering from reduced enrollment and the need to spread fixed costs over a smaller customer base. Schools want to diversify their revenue.

The college might be interested in selling or leasing land to a senior living provider. The provider could buy IT, fitness, dining, or educational services from the school rather than creating them in-house. The key questions are: What are your objectives? Are you aligned with the school’s objectives to develop an intentional partnership?

Kramer: What is the most surprising thing you’ve learned as director of Lasell Village and with your new firm?

Doyle: We too often segregate social services and healthcare. And education is never in the same conversation. Put those pieces together, and then we’re really talking about wellbeing.

Kramer: What is the key takeaway from your time leading Lasell Village?

Doyle: A key attribute of our success is that I had a role in the governance of the university. I had very good insights into the educational sector and the bottom line as well as the strength of the senior living community. I was constantly thinking of ways to benefit each party. It’s important to think about the alignment at the top. It can’t just happen naturally.

Kramer: You recently took a trip to Sweden. What new perspectives did you bring back?

Doyle: When I was 25, I studied in Sweden looking at alternative ways for older adults to live and receive services. I recently went back as a fellow at the University of Gothenburg. My ‘aha moment’ was that it’s universal to think about how to live a full life. We all want to be respected, live fully and not be restricted.

Kramer: Anything else you’d like to add?

Doyle: If we just focus on the capital markets and whether it makes sense to build a community near or on a campus, we are missing the opportunity to create intergenerational communities. But it takes an intentional connection between the leaders of both organizations. This period of slow development should not stop us from thinking boldly about what is possible to entice the next generation.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. NIC's privacy policy can be viewed here. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Anne Doyle, CEO of Spark Living and Learning, shares exciting new ideas here on how to develop a learning culture to attract the next generation of residents. Partnerships with local colleges or universities can provide unexpected benefits such as employee sourcing, expense management, educational enrichment, and engagement with the wider community.

Anne Doyle, CEO of Spark Living and Learning, shares exciting new ideas here on how to develop a learning culture to attract the next generation of residents. Partnerships with local colleges or universities can provide unexpected benefits such as employee sourcing, expense management, educational enrichment, and engagement with the wider community.