Veteran Operator Ken Segarnick: “Lifestyle Is the Differentiator”

As the pandemic eases, seniors housing and care operators are looking ahead. What lessons have been learned over the last 15 months to bolster consumer confidence? What strategies will boost occupancy?

As the pandemic eases, seniors housing and care operators are looking ahead. What lessons have been learned over the last 15 months to bolster consumer confidence? What strategies will boost occupancy?

“The question now is whether we can really deliver on lifestyle,” said Ken Segarnick, chief corporate officer at Brandywine Living, a New Jersey-based operator of 32 luxury senior living communities in the Mid-Atlantic. “The game-changer is creating an environment that people want to age into.”

An industry veteran, Segarnick is among the thought leaders attending the 2021 NIC Fall Conference in Houston. The Conference is NIC’s first in-person convening of leaders in seniors housing and care since the pandemic began and offers a chance to share ideas with others weathering the same challenges.

Segarnick said the pandemic demonstrated that seniors housing can provide a safe environment. Acts of heroism and courage by the staff helped to protect residents from infection. Communities helped to provide early access to vaccinations. Data show that resident outcomes have generally been favorable.

The pandemic also highlighted the fact that a senior living experience must include human interaction. Isolation became a huge issue over the course of the disease outbreak. “Human beings need social engagement in order to thrive,” said Segarnick. “As operators, we need to maximize joy and happiness to help residents have a life well lived.”

Community programming did reach new dimensions over the last year, mostly out of necessity. Residents and families connected in creative ways through technology and social media. The customer experience became more tailored to individual preferences.

What’s Next?

The challenge now is to deliver a next-level lifestyle experience incorporating lessons learned. “Senior living is a consumer-driven business,” said Segarnick. “Though healthcare needs will continue to be a key element to senior living decisions, there’s more to what customers are looking for. They want to enjoy living their lives, they want a better experience.” The goal is to wrap the lifestyle experience around the care needs of residents. “Lifestyle is the differentiator,”Segarnick added.

Segarnick defines lifestyle as part choice, part engagement. Giving residents choices, based on their personal preferences, enhances their lifestyle. It could be offering different dining options or touch as small as knowing which newspaper the resident likes. “Small details build broader experiences,” said Segarnick.

Engagement is also key to a rewarding lifestyle. But true engagement goes well beyond the basic activities on the daily calendar and includes all dimensions of wellbeing to provide joy and social enrichment.

Segarnick challenged operators to translate the personal preferences of residents into exciting experiences tailored for them. “Our residents want engagement that meets them where they are,” he said.

Real estate is part of the lifestyle equation post-pandemic. Residents want more space and connectivity with the outdoors. Common areas should be big and open. Residents want larger apartments to enjoy their own space too. “Where people live is an essential element of lifestyle,” said Segarnick.

He admitted that more work needs to be done to rebuild consumer confidence in seniors housing and care. But he noted, “Consumer confidence is not something marketed or sold, but earned.”

Post pandemic, consumers want a more robust senior living option, and providing that will have a direct impact on the operator’s bottom line.

The 2021 NIC Fall Conference Will be In-Person

NIC is convening thousands of seniors housing and skilled nursing capital providers, operators, and sector stakeholders for the first in-person NIC event since the onset of COVID-19.

NIC is convening thousands of seniors housing and skilled nursing capital providers, operators, and sector stakeholders for the first in-person NIC event since the onset of COVID-19. The 2021 NIC Fall Conference will deliver an exceptional attendee experience which attendees of NIC conferences have come to expect – but is incorporating a few changes to adapt to the demands of a world still battling a pandemic.

Networking at ‘the NIC’

Veterans of previous NIC Fall Conferences know that ‘the NIC’ is the most efficient, effective single opportunity of the year for building and deepening relationships within the industry. This year will provide all of the opportunities to meet in hallways, at the bar, at the restaurants, in educational sessions, and in meeting rooms set up for the purpose throughout. And as always, NIC is providing numerous structured opportunities for high-quality networking throughout the event, so attendees can focus on pursuing new contacts, deepening existing relationships, and strengthening their networks.

As in previous years, the event will feature abundant networking environments throughout the conference space, including two areas specifically designated as official Networking Lounges. The lounges will also be home to numerous attendee resources, including the Headshot Lounge, Specialty Coffee Bar, Shoeshine Area, and LinkedIn Corner.

The conference will also feature two NIC Social Hour events, for a more relaxed happy hour-like atmosphere.

All attendees who register by October 1 will receive a NIC lapel pin in their pre-conference mailing. This pre-and post-conference icebreaker further extends networking possibilities, increasing the chances of attendees making new friendships and potential business relationships, even as they travel to and from the event.

As always, first-time attendees will be afforded special activities and resources specifically geared to help them successfully navigate the conference, including an orientation webinar, a First-time Attendee Gathering, and morning meetups.

Programming

Educational programming will span all three days of the conference—offering stand-alone, not-to-be-missed sessions on the issues that will shape seniors housing and care organizations for years to come. The program will include interactive discussions and will feature insights and perspectives from nationally prominent thought-leaders, industry veterans, and policymakers on a carefully curated set of topics of the most importance and relevance in today’s world.

New this year, both in service to safety considerations and the need to focus thought-leadership and discussions on the most important issues, there will be no concurrent sessions. Instead, larger spaces will hold a series of general sessions, scheduled not to overlap. For many, the schedule will be a welcome relief from having to choose between two important sessions occurring concurrently.

Subject matter will include many traditional topics, such as policy outlook, valuations, macroeconomic and capital market trends, and debt market trends. Attendees may also wish to hear from experts and insiders on capital for operations, the case for investing in seniors housing, the forgotten middle market, thinking differently about housing for boomers, and, of course, the recovery timeline for the industry.

Safety

NIC is requiring proof of COVID-19 vaccinations for all registered attendees, in the interest of everyone’s safety.

The decision to require every attendee to provide proof of vaccination, to be confirmed through a third-party vendor, may result in a few attendees opting to stay home. But it reflects both a commitment to fight the pandemic and an awareness of the heroic struggles of many attendees – and over a million of their frontline caregivers – who have fought so hard to protect their communities.

Attendees will be required to provide a photo of themselves, which will be placed on their conference credentials. They must also provide proof of vaccination, with the final dose completed no later than Sunday, October 17, 2021. Once confirmed, submitted documents will be deleted.

Also new this year is the fact that there will be no last-minute or onsite registrations, to allow for the additional safety protocols. NIC is offering no-fee cancellations, up to 30 days prior to the event, to further insulate attendees from the risks of COVID-19. Those who register by October 1 will receive their badges and a PPE kit via mail to reduce queuing and encourage adherence to safety protocols.

Detailed, up-to-date safety information can be found here.

Register Now

This year, given the new safety protocols, attendees must register by Thursday, October 28. As an increased safety measure, onsite registrations will not be accepted for the 2021 NIC Fall Conference. Currently, NIC is offering Early Bird incentives, with significantly discounted rates that will increase on August 16. Don’t miss the most important in-person industry event of 2021. Register yourself and your associates today!

{{cta(‘ee4df396-eafd-4330-9697-24b8cc03c800’)}}

“Business as Usual” at People’s United: A Conversation with Matthew Huber

NIC Chief Economist Beth Mace recently talked with Matt Huber of People's United about the merger, the benefits for borrowers, and the outlook for the sector.

This past February, M&T Bank Corporation announced its intention to merge with People’s United Financial, Inc. with M&T Bank as the surviving entity. The merger—expected to close in October—brings together two powerhouse seniors housing and care lenders.

The combined company will include about $200 billion in assets, and a network of nearly 1,100 branches spanning 12 states from Maine to Virginia.

People’s United is meanwhile open for business, says Matthew Huber, Market Manager of Healthcare Financial Services at The Bank. His team continues to close loans on a timely basis and provide commercial banking services.

NIC Chief Economist Beth Mace recently talked with Huber about the merger, the benefits for borrowers, and the outlook for the sector. Here is a recap of their conversation.

Mace: What does the merger mean for existing seniors housing and skilled nursing clients of both organizations?

Huber: M&T has a big presence in the seniors housing space and has a long-term commitment to the industry. So, I think the merger will be really good for the seniors housing and care borrowers at People’s United. M&T has a robust platform with permanent agency financing from Freddie Mac and FHA/HUD. Borrowers will have more solutions. People’s United is about half the size of M&T. Given their size, we’ll have more room to grow and participate in larger seniors housing and care transactions.

Mace: Will the merger affect how you traditionally look at borrowers that seek debt funding for seniors housing and skilled nursing mergers? How about recaps and rehabs?

Huber: Between now and the actual closing of the merger, we are operating as two separate companies. At People’s United, we have continued to do exactly what we’ve been doing for the last number of years – focus on relationships, advice and tailored solutions. We’re winning new business on a consistent basis. In April, we closed on a refinance loan for Masonicare at Mystic, a life plan community in Connecticut. We recently won a term sheet to provide construction financing for a new project by RSF Partners in New York State. We’re also refinancing a Benchmark property in New England. We’re sticking close to our credit policy in terms of price and structure. Given the pandemic, we’re still winning business because of our relationships with our customers. We’re proud of that.

Mace: Are you open for business for new development?

Huber: Yes.

Mace: What about turnarounds?

Huber: Other than new construction, we only finance properties with in-place cash flows. If it’s a turnaround, we can only finance what current cash flows can support.

Mace: You’ve traditionally been a relationship bank, working with repeat clients that have proven track records with experience in either seniors housing or skilled nursing. What should potential new borrowers be prepared to provide you to become eligible for new debt?

Huber: Though it’s a big industry, it’s small in terms of the number of companies and banks that are fully engaged in seniors housing and care. It would be surprising if a known company with a portfolio did not have a banking relationship. If we don’t know the company, then we ask other industry stakeholders such as attorneys and accountants if they know the company. Mostly, new borrowers for us must be regional in scope and have multiple properties. If they’re one of our top 20 prospects, they have to provide the same type of information we would ask from anyone making a new request. That includes a real estate schedule of their existing properties to see how they’re doing. We conduct full due diligence. As much as we’re seeing green shoots of positivity in the industry, we’re not out of the woods yet. I need to know borrowers have the liquidity to get them through this time, however long that may be. We’re going with the tried-and-true companies that have been there and done that, whether they’ve banked with us or not.

Mace: You’ve significantly grown People’s United lending volume with the seniors housing and skilled nursing sector in the last few years. What is your secret to success?

Huber: When I joined People’s United about four years ago, ourhealthcare portfolio was about $400 million in balances, with about half in seniors housing and the other half to hospitals. Today we are at about $2.5 billion. We’ve grown by hiring the right people and consistently delivering solutions for our customers. I have an experienced staff of five relationship managers who’ve been in the industry for decades. They know commercial banking and they know the healthcare industry. We have consistent solutions and don’t waiver from them. Our process is very simple from term sheet to approval. Certainty of execution is so important to the client and they know what they’re getting from us because we don’t change our terms. We don’t come in the day before closing and ask for more equity or covenants. Our customers are important to us. We learn a lot from them, and we truly enjoy building relationships with them.

Mace: With the worst of the pandemic hopefully behind us, how will your lending practices change post-COVID?

Huber: I think we’ll go back to more of a limited recourse requirement once we see facilities have stabilized. Until then, we have increased our requirements to full recourse, though we give borrowers a path to release based on performance. Prior to the pandemic, we were asking for 25% -50% recourse, depending on the deal or borrower. We don’t do non-recourse construction loans.

Mace: Have you seen a slowdown in construction because of cost overruns?

Huber: We have seen minor slowdowns in construction, but nothing too concerning yet. The cost of materials and overruns are mind boggling. The projects are so big, $70 million to $80 million. So, having strong sponsors is key for construction projects currently underway should challenges arise that dictate the need for additional project funding.

Mace: Are you optimistic for the recovery of the sector in 2021? Beyond 2021?

Huber: I am optimistic. Seniors housing and care has done a good job of getting residents vaccinated. There is still some work to be done on the employee side. But I think it’s headed in the right direction. We’re starting to see some positivity on occupancy. I think it’s going to take a little longer than we hoped for properties to stabilize. The recovery will continue into the first half of 2022. But I’m optimistic. Baby boomers are 75 years old. The first ones turn 80 in five years and that’s when the usage of seniors housing really escalates. Skilled nursing will undergo some changes that have been accelerated by the pandemic. We’re not going back to the way skilled nursing was in 2019 with a lot of short stays. More rehab will be done at home and we’ll need fewer beds over time. Nursing homes will do more home care for their customers coming out of the hospital.

Mace: What gives you pause about the sector if anything?

Huber: I don’t have a crystal ball, but uncertainty gives me pause. Telehealth and Home Care will impact our customer base, and anything like that causes uncertainty in cash flows. Assisted living is still somewhat of a choice. Memory care is coming back quickly. But we need to keep our eye on assisted and independent living and how skilled nursing will mature as an industry. I see a positive future. But the question is: will occupancies be back in the high 80s by the end of the year, or not?

Mace: Is there anything else you would like our readers to know about People’s United?

Huber: We are still open for business. We have one of the most experienced teams in the industry. Our team includes: Walt Unangst, David Canestri, Claudia Gourdon, Ginger Stolzenthaler and Ryan Zyskowski. The upcoming merger is a plus for customers. M&T Bank is a well-known lender in this industry and we are confident the combined company will deliver much value to our clients. Borrowers will be in good hands regardless of the name over the door.

Cautious Optimism: Occupancy Rates Appear to Have Hit Bottom

Senior housing occupancy rates may have reached the low point in February and March of 2021; however, when it will return to pre-pandemic levels remains a question.

While it is still early to say if the seniors housing and care market is showing strong and durable signs of a recovery, several indicators from the NIC MAP® Data, powered by NIC MAP Vision, and from NIC Analytics have sparked cautious optimism and suggest that we may be at least at the bottom of the cycle. Occupancy rates may have reached the low point in February and March of 2021; however, the outlook for when occupancy will return to pre-pandemic levels remains a question.

In this blog, we look at four indicators from NIC MAP data and NIC Analytics that measure occupancy, move-ins and move-outs, overall demand, and lead volumes, which all do seem to point to modest signs of inflection and portray the sector’s current level of performance.

Top Findings:

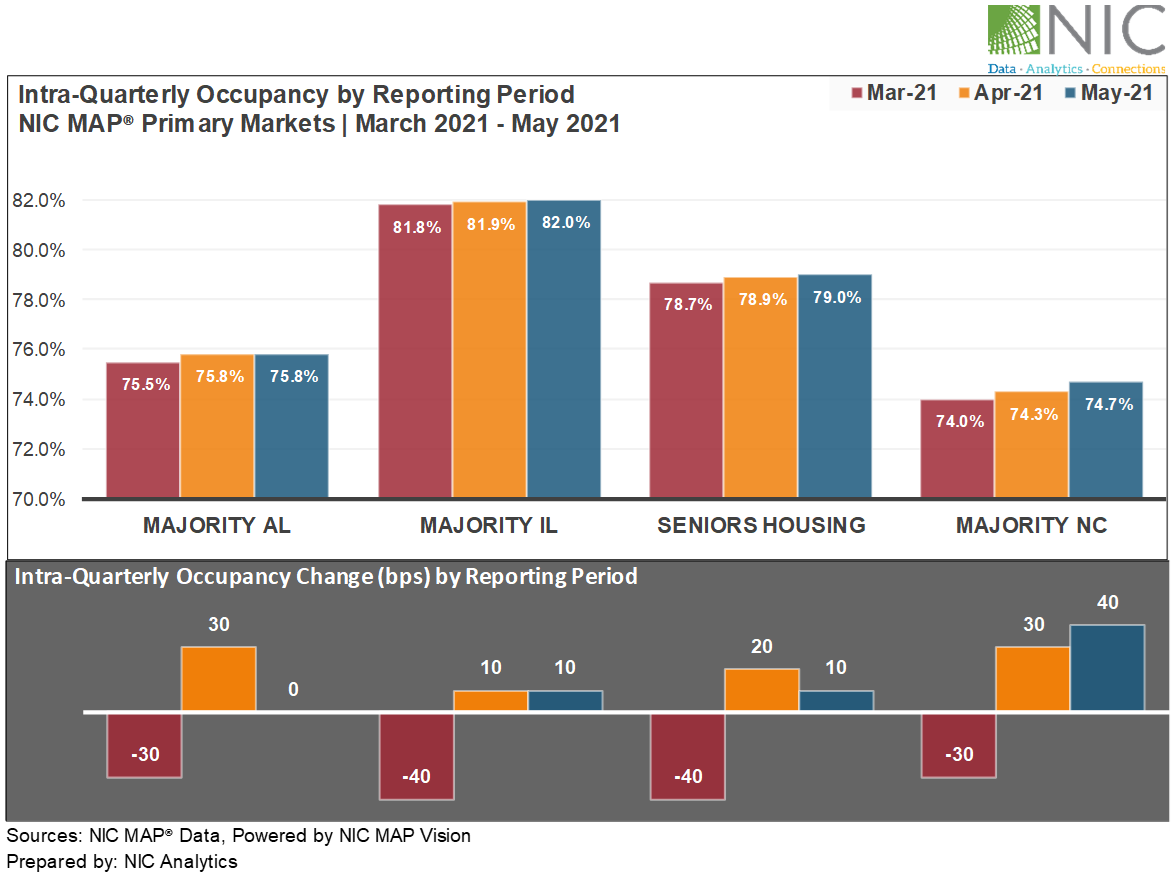

The just released NIC Intra-Quarterly Snapshot shared the latest reported NIC MAP data. This data showed that the occupancy rate for seniors housing edged up 0.3 percentage points in the May 2021 reporting period for the NIC MAP Primary Markets on a three-month rolling basis above its all-time low of 78.7% in the March 2021 reporting period, but it remained very low by historic standards.

NIC MAP intra-quarterly data showed that majority nursing care (NC) properties had the largest increase in occupancy since March 2021 reporting period, up 70 basis points (bps) but at 74.7%, it is still 11.9 percentage points (pps) below the pre-pandemic March 2020 level.

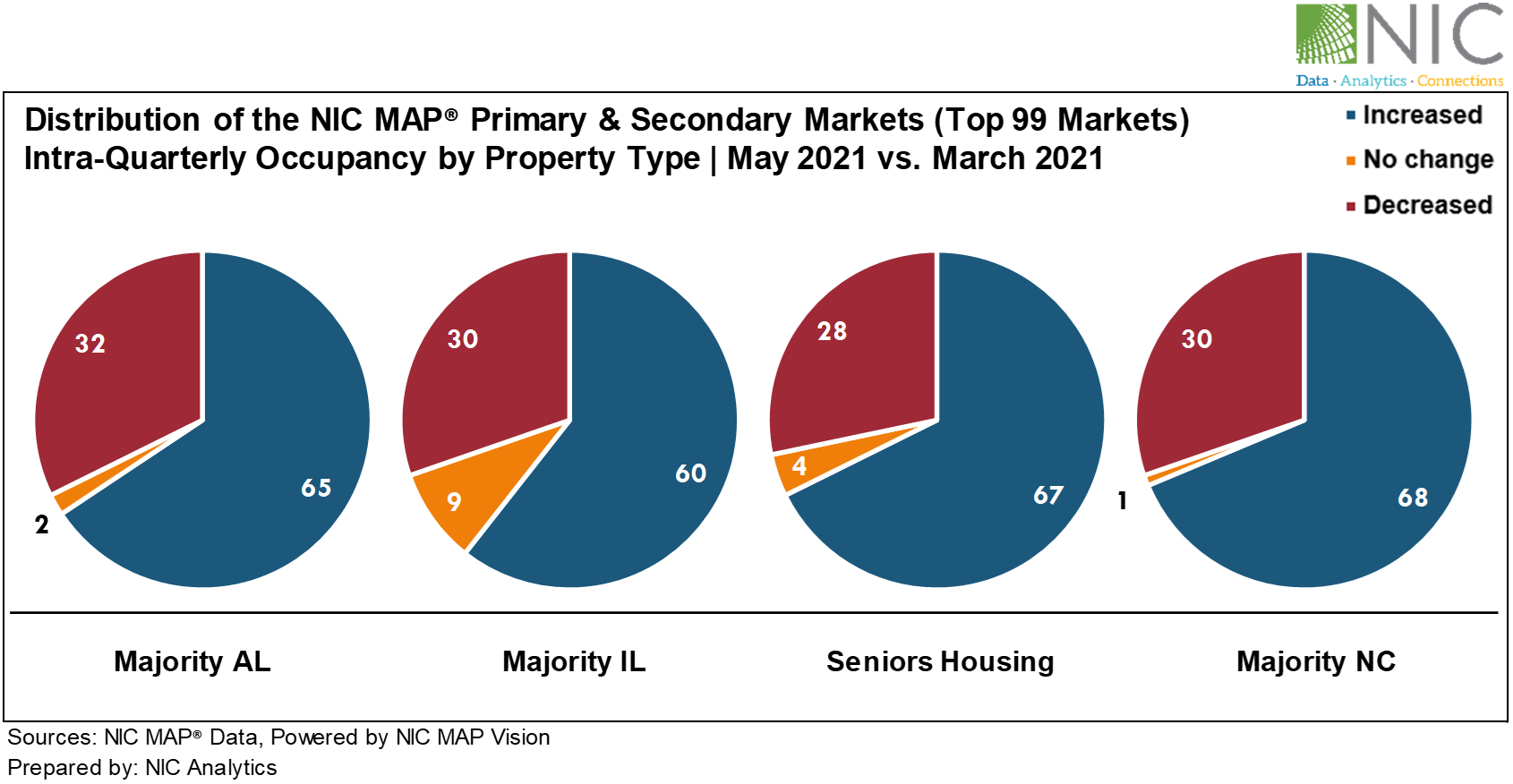

Sixty-seven of the 99 NIC MAP Primary & Secondary Markets for seniors housing saw an increase in occupancy since March 2021. Over the same period, sixty-eight markets for majority nursing care experienced an increase in occupancy rates, according to May 2021 NIC MAP intra-quarterly data.

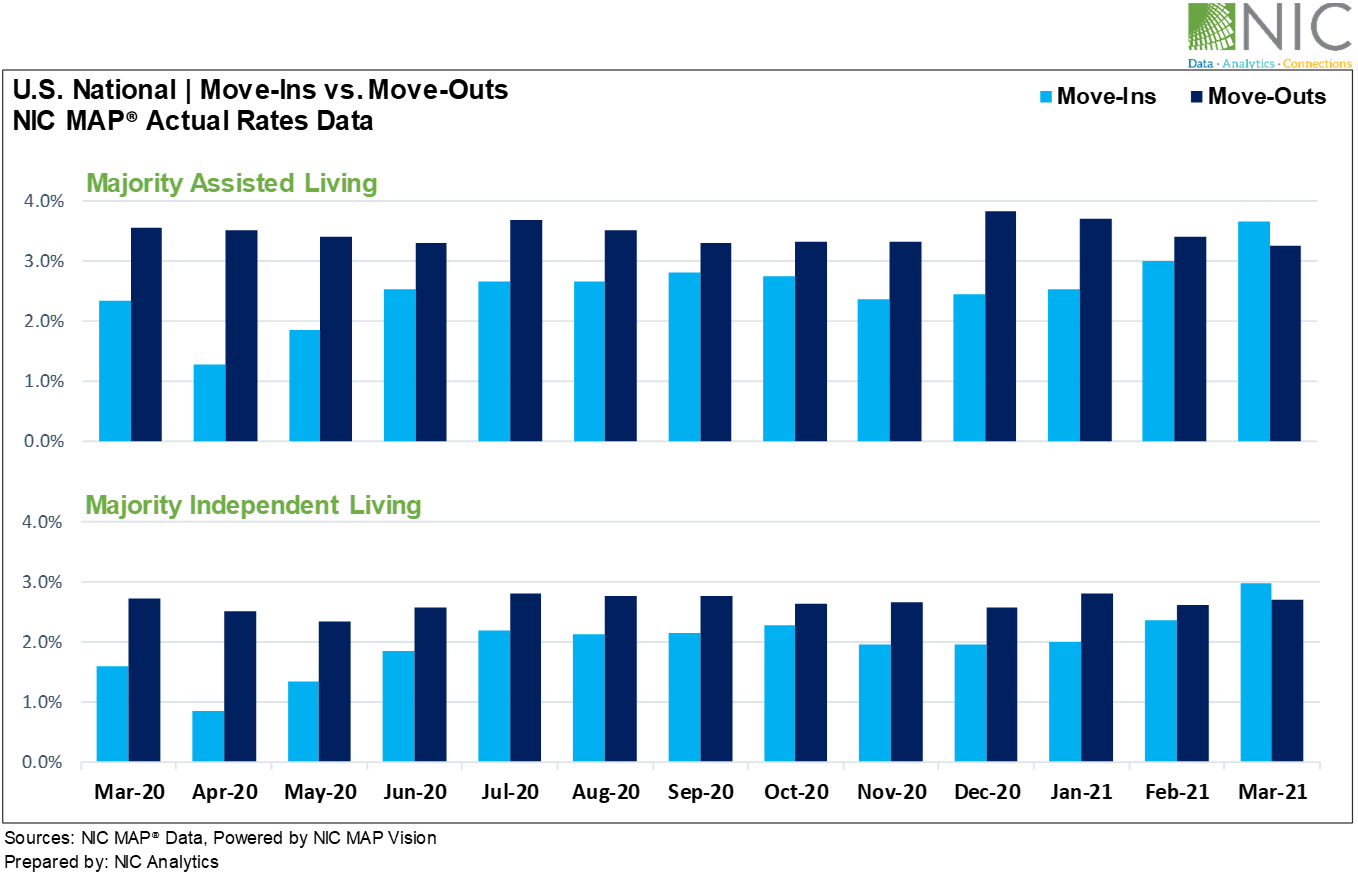

The NIC MAP Actual Rates Report showed that move-ins reached new highs in March 2021 for both majority independent living and majority assisted living since NIC began reporting actual rates data in 2015.

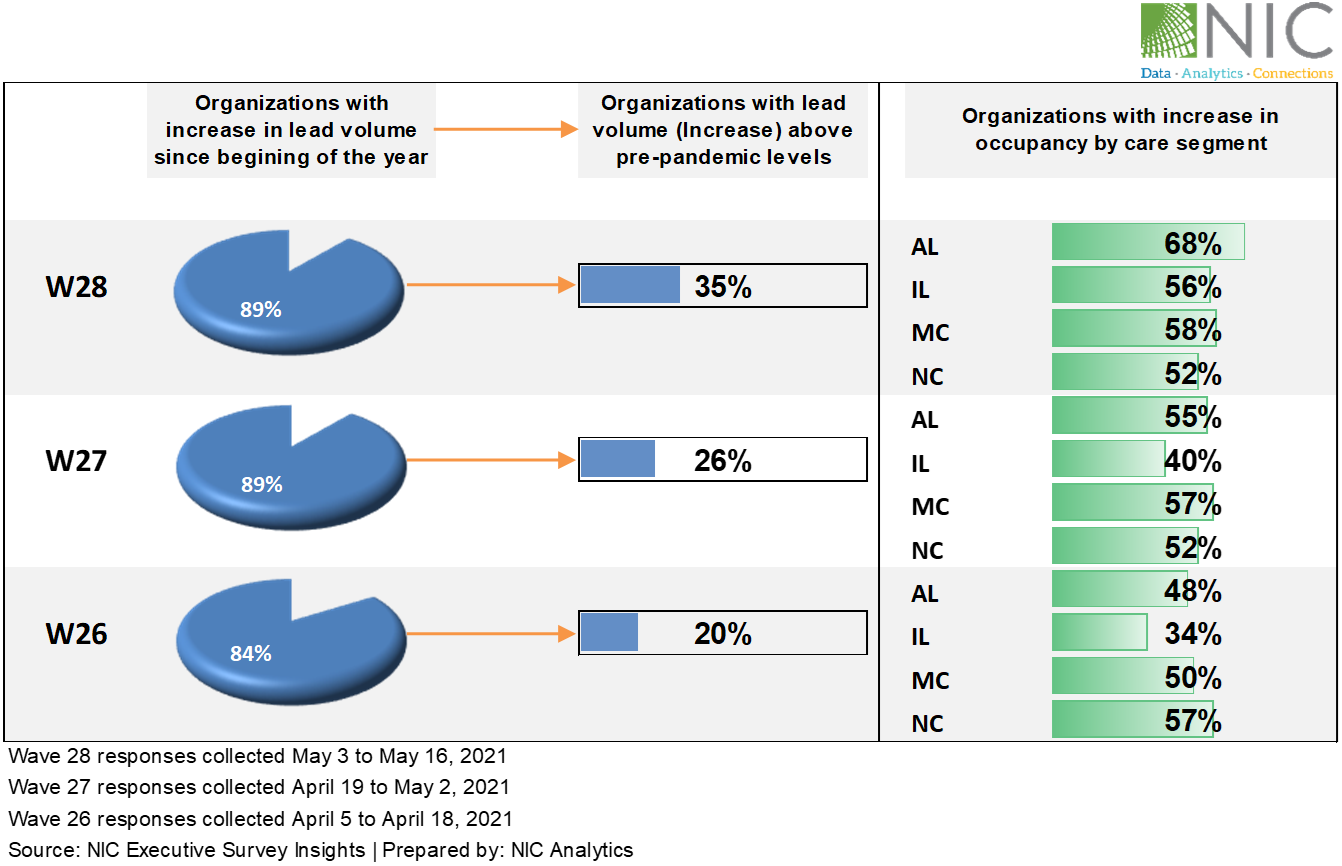

Wave 28 of NIC Executive Survey Insightsalso reported lead volumes increasing and move-ins accelerating for some survey respondents, resulting in gains in occupancy for more than 50% of respondents.

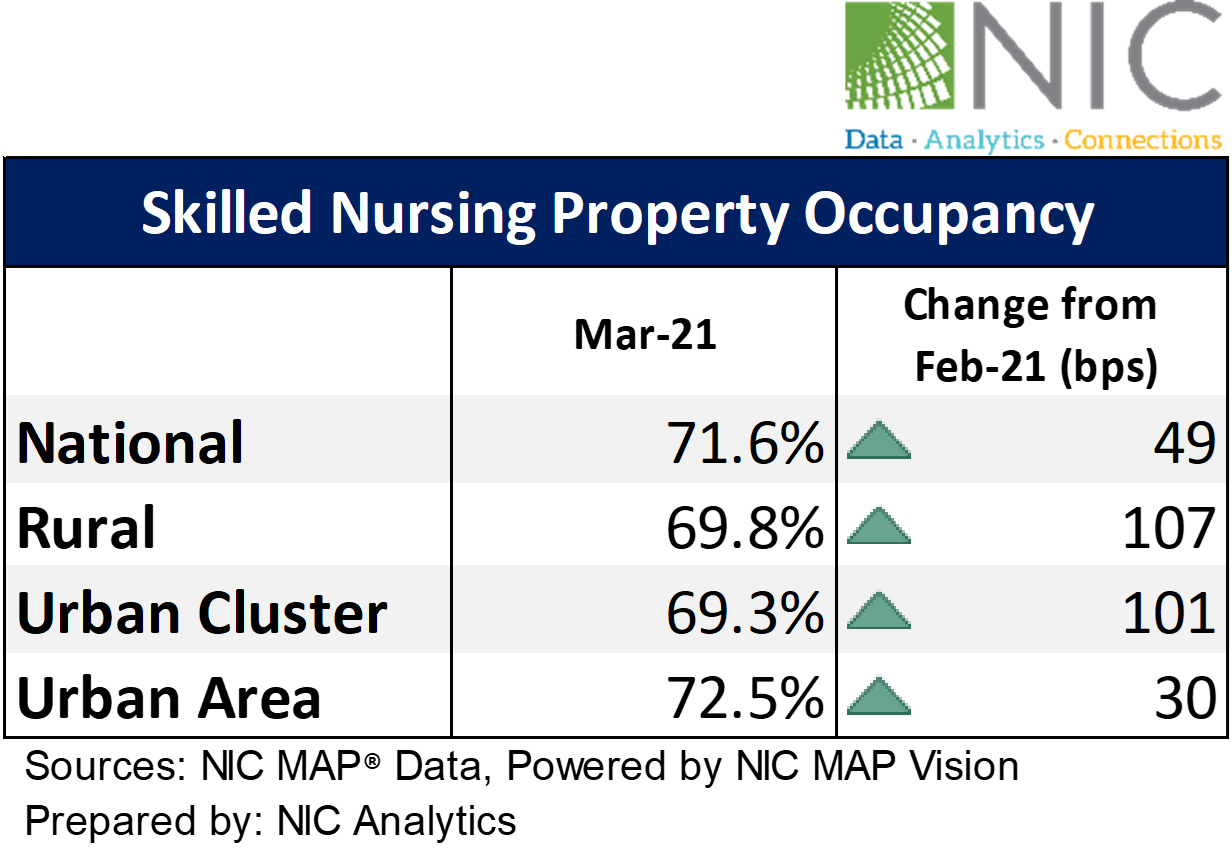

The NIC MAP Skilled Nursing Monthly Report, released by NIC MAP Vision, with data through March 2021 showed that skilled nursing property occupancy increased for a second month in a row. It increased 49 bps from February to end March at 71.6%. It is up 89 bps from the low set in January 2021.

NIC MAP Intra-Quarterly Data – As of May 2021

Exhibit 1 below depicts that the all-occupancy rate for seniors housing inched up 0.1 percentage point to 79.0% in the May 2021 reporting period for the NIC MAP Primary Markets on a three-month rolling basis from the April 2021 reporting period. This placed the occupancy rate 0.3 percentage points above its all-time low of 78.7% in the March 2021 reporting period, but it remained very low by historic standards. Prior to the pandemic in the March 2020 reporting period, occupancy was 87.5% — 8.5 percentage points higher than the most recent data point.

Since its low point in the March 2021 reporting period, the all-occupancy rate for majority assisted living (AL) was up 0.3 percentage points to 75.8% for the NIC MAP Primary Markets on a three-month rolling basis, although there was little change from the April 2021 reporting period. Majority independent living (IL) properties saw an increase of 0.2 percentage points since March 2021, with a gain of 0.1 percentage point in both April and May.

Majority nursing care (NC) properties had the largest increase in occupancy since March 2021 reporting period, up 70 bps but at 74.7%, it is still 11.9 pps below the pre-pandemic March 2020 level. The relatively large improvement shows the positive impact early inoculation has had on occupancy rates for majority nursing care properties. In addition, skilled nursing properties have benefitted from the resumption of elective surgeries at hospitals since recuperation and post-acute care from knee and hip surgeries often take place in skilled nursing settings.

The bottom line is that for the overall NIC MAP Primary Markets aggregate occupancy rate, no declines have been reported for two consecutive monthly reporting periods (April and May 2021) across all property types.

Exhibit 1 – Intra-Quarterly Occupancy by Reporting Period – Data as of May 2021

Exhibit 2 below shows that occupancy increased or remained stable in 65 of the 99 NIC MAP Primary & Secondary Markets for AL in the May 2021 reporting period compared to March 2021 levels. Thirty-two markets’ occupancy continued to slip further, and two remained stable.

For IL, 60 of the 99 Primary & Secondary Markets had higher occupancy rates in May 2021 compared to March 2021 levels.

Overall, 67 of the 99 NIC MAP Primary & Secondary Markets for seniors housing saw an increase in occupancy since March 2021. Over the same period, 68 markets for majority nursing care experienced an increase in occupancy rates.

Exhibit 2 – Distribution of the NIC MAP Primary & Secondary Markets (Top 99 Markets)

NIC MAP Seniors Housing Actual Rates Data – As of March 2021

The recently released 1Q2021 NIC MAP® Seniors Housing Actual Rates Report showed that for the first time since the pandemic unfolded in the U.S. and began to influence the seniors housing sector, move-ins outpaced move-outs for both majority independent living and majority assisted living, as shown in Exhibit 3.

Notably, move-ins reached new highs in March 2021 for both majority independent living (3.0%) and majority assisted living (3.7%) since NIC MAP began reporting actual rates data in 2015. This corroborates the increase in lead volume captured in NIC’s Executive Survey Insights, which has been reportedly above pre-pandemic levels for some data contributors.

Exhibit 3 – Majority Assisted Living and Majority Independent Living – Move-ins vs. Move-Outs

NIC Executive Survey Insights (Wave 28 Survey)

Wave 28 of NIC’s Executive Survey Insights also reported lead volumes increasing and move-ins accelerating for some survey respondents, resulting in gains in occupancy for more than 50% of respondents.

Exhibit 4 below depicts that since early April, respondents were asked if their organizations had seen an increase in resident lead volume since the beginning of the year and, if they had, if lead volume is above pre-pandemic levels. As shown in the chart below, about nine out of ten organizations reported an increase in lead volume (89%). Additionally, one-third of organizations report lead volume currently above pre-pandemic levels (35%) compared to 20% in Wave 26 conducted just one month prior. Regardless of reports of notable improvement in lead volume, nearly two-thirds of survey respondents expect their organizations’ occupancy rates to recover to pre-pandemic levels sometime in 2022. This sentiment has remained consistent since first reported in late February (Wave 23). In fact, roughly 50% to 70% reported upward changes in occupancy in the Wave 28 survey.

Exhibit 4 – Lead Volume and Occupancy by Care Segment According to Data Compiled by NIC Executive Survey Insights (Wave 28 survey)

NIC Skilled Nursing Data Initiative – Data as of March 2021

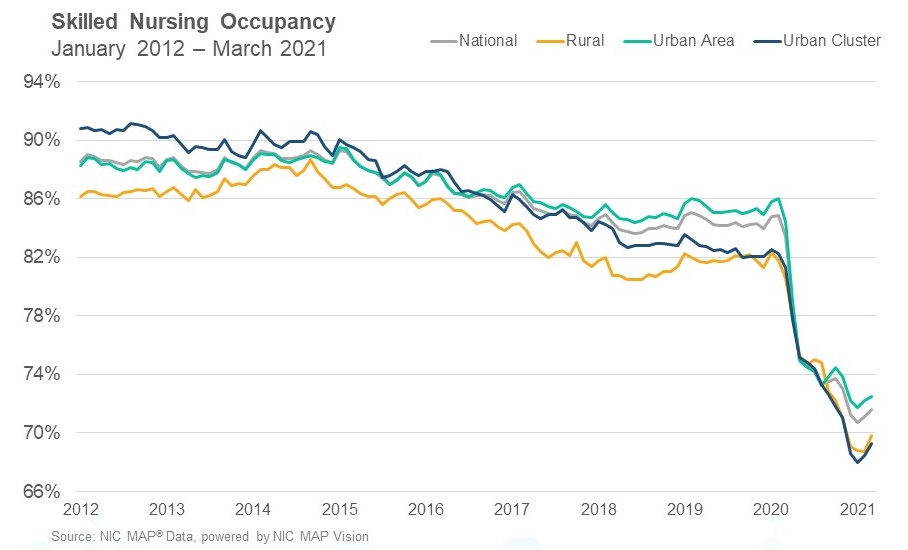

The NIC MAP Skilled Nursing Monthly Report released by NIC MAP Vision, with data through March 2021, showed that skilled nursing property occupancy increased for a second month in a row. As shown in Exhibit 5 below, it increased 49 bps from February to end March at 71.6%. It is up 89 bpsfrom the low set in January 2021. The expectation was occupancy would increase given the decline in COVID-19 cases across the country. Although occupancy seems to have stabilized, it remains very low compared to pre-pandemic levels. It is 13.2 percentage points below the February 2020 occupancy when it was 84.8%.

Nursing care properties in urban areas reported the highest occupancy rate in March 2021 at 72.5%, followed by rural (69.8%) and urban clusters at 69.3%. The largest increase in occupancy has been reported in rural, up 107 bps from February 2021 levels.

Exhibit 5 – Skilled Nursing Property Occupancy – Data as of March 2021

These signs are promising and suggest that positive demand is returning. The full recovery from the COVID-19 crisis, however, will likely not be immediate or fast. Operators have not only suffered significant losses due to the COVID-19 pandemic but also had to navigate through the COVID-19-related recession amid slowing rates of move-ins and rising operating expenses to protect their residents. While some entire industries shut down such as restaurants, seniors housing remained open despite a host of proliferating challenges related to PPE, testing, infection control, staffing challenges, a patchwork of disparate regulations, lockdowns, limits on visitation, and social distancing. This agility, in and of itself, shows the resilience and endurance of the seniors housing market through the pandemic.

Thanks to the way vaccines have been distributed and administered, prioritizing the population most vulnerable to the virus, namely older Americans and residents of skilled nursing and seniors housing properties, COVID-19 cases in the U.S. have fallen to levels not seen since March 2020 and virus cases in skilled nursing properties dropped to lowest point in pandemic, according to CMS data compiled by NIC’s Skilled Nursing COVID-19 Tracker. The positive impact early vaccinations have had on the sector started to translate into positive demand, higher lead volumes, and improvements in occupancy rates.

With 15 years’ hindsight, the seniors housing market plays a critical role in supporting and helping America’s seniors age comfortably. The pandemic has revealed hidden and long-standing weaknesses, but also presented enormous opportunities for innovation and growth. Consumer demand and housing needs may have changed but the value proposition of seniors housing care settings in the post-pandemic world have strengthened. High quality care is essential for continuum of care in seniors housing. However, a sense of belonging, socialization, and engagement are the value propositions of a continuum of wellness. This will lead to a healthier resident outcome, a stronger seniors housing market, and a faster recovery for the sector, especially, as demand and the population of seniors increase and the baby boomer generation ages.

Looking ahead with any certainty is always difficult, but there is an air of cautious optimism regarding the future trajectory of seniors housing. The industry will recover if for no other reason than the fact that the industry’s value proposition and product offerings are critical for care and housing options for today’s older adult population as well as for America’s rapidly aging population. Today’s oldest baby boomer is 75 and quickly approaching the age of needing seniors housing (age 82 or more). Additionally, the sector offers compelling and emerging opportunities in both healthcare collaboration and population health management, as evidenced by the pandemic, and as critically needed to stave off staggering societal healthcare costs. And lastly, there is a better understanding of the sector by institutional capital providers who hold significant amounts of investable and targeted capital.

Interested in learning more about NIC MAP data? To learn more about NIC MAP data, powered by NIC MAP Vision, and about accessing the data featured in this article, schedule a meeting with a product expert today.

Skilled Nursing Occupancy Increased in March for Second Straight Month, But Remains Low

Key takeaways from the March 2021 Skilled Nursing Monthly Report, from NIC MAP® Data Service, powered by NIC MAP Vision.

Medicare Patient Day Mix Continues Decline.

NIC MAP® Data Service,powered by NIC MAP Vision, released its latest Skilled Nursing Monthly Report on June 3, 2021, which includes key monthly data points from January 2012 through March 2021.

Here are some key takeaways from the report:

Occupancy

Skilled nursing property occupancy increased for a second month in a row, increasing 49 basis points from February to end March at 71.6%. It is up 89 basis points from the low set in January. The expectation was occupancy would increase given the decline in COVID-19 cases across the country, but the question remains of how fast it will recover. Although occupancy seems to have stabilized, it remains very low compared to pre-pandemic levels. It is 13.2 percentage points below the February 2020 occupancy when it was 84.8%. There is still cautious optimism, but the next few months of data will be critical in order to verify if the recovery in occupancy continues.

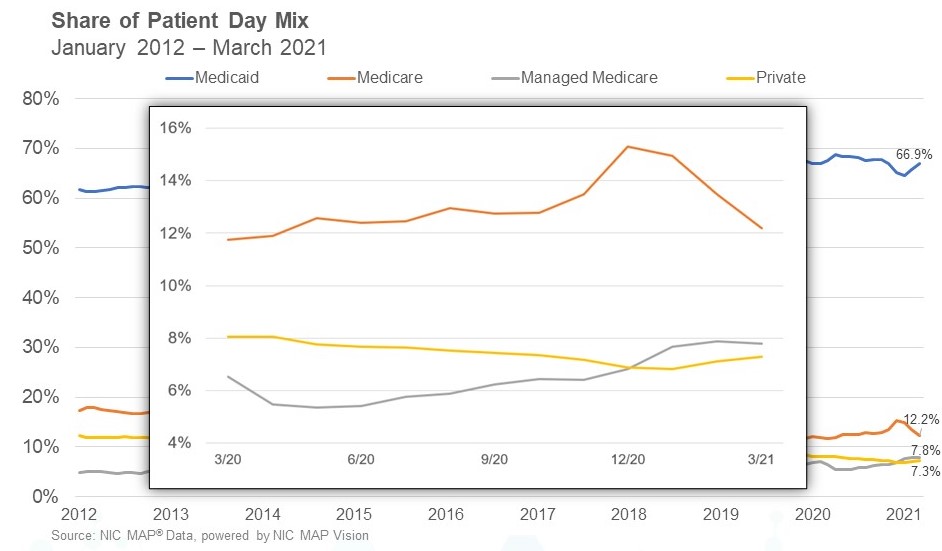

Medicare

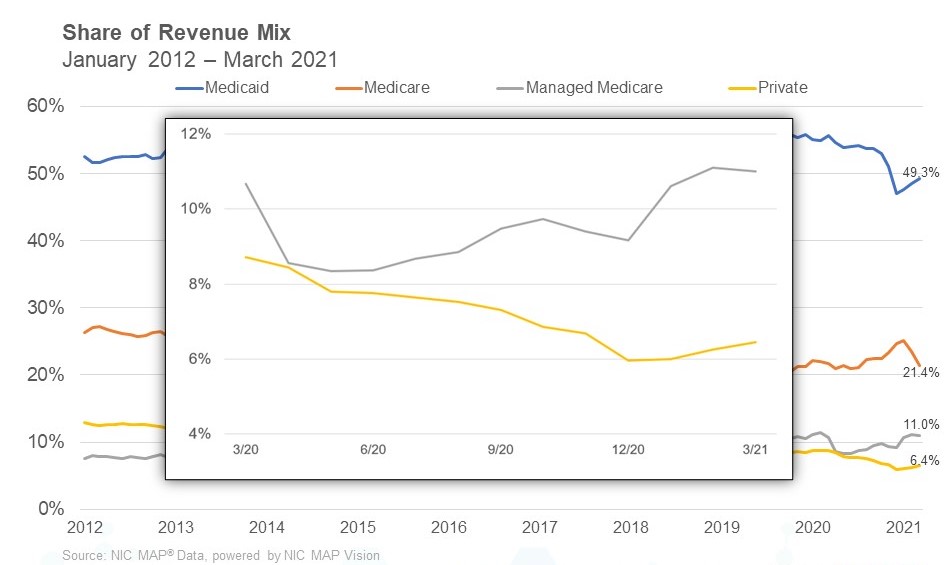

Medicare patient day mix dropped 127 basis points from February to end March at 12.2%. It has decreased three months in a row and is now down 309 basis points from the recent high set in December 2020. In addition, Medicare revenue mix declined as well, falling 201 basis points from February, and ending March at 21.4%. This suggests the utilization of the 3-Day Rule Waiver is declining which makes sense as COVID-19 cases declined significantly since January. The 3-Day Rule Waiver was implemented by Centers for Medicare and Medicaid Services (CMS) to eliminate the need to transfer positive COVID-19 patients back to the hospital to qualify for a Medicare paid skilled nursing stay.

Managed Medicare

Managed Medicare patient day mix was relatively flat from the prior month, ending March at 7.8%. However, it is up 245 basis points from the pandemic low set in May of 2020 when many states restricted elective surgeries and some skilled nursing operators were unable to admit patients. In addition, managed Medicare revenue mix ended March at 11.0% and is up 183 basis points from the end of 2020 and up 266 basis points from its low also set in May of 2020. The slight increase in occupancy and managed Medicare patient day mix of late is welcomed news but the question remains of if, and when, patient admissions will get back to pre-pandemic levels.

Medicaid

Medicaid revenue mix continued to increase as it ended the month of March at 49.3%. It continues to inch back to a more historical normal level. The pre-pandemic level in February 2020 was 55.0%. It is up 228 basis points from the pandemic low of 47.0% set in December 2020. In addition to lower overall admissions, the waiver of the 3-Day Rule also likely played a role during the pandemic in regard to lower Medicaid revenue mix as COVID-19 positive patients converted to Medicare from Medicaid.

The report provides aggregate data at the national level from a sampling of skilled nursing operators with multiple properties in the United States. NIC continues to grow its database of participating operators in order to provide data at localized levels in the future. Operators who are interested in participating can complete a participation form here. NIC maintains strict confidentiality of all data it receives.

Interested in learning more about NIC MAP data? To learn more about NIC MAP data, powered by NIC MAP Vision, and about accessing the data featured in this article, schedule a meeting with a product expert today.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. NIC's privacy policy can be viewed here. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

“The question now is whether we can really deliver on lifestyle,” said Ken Segarnick, chief corporate officer at Brandywine Living, a New Jersey-based operator of 32 luxury senior living communities in the Mid-Atlantic. “The game-changer is creating an environment that people want to age into.”

“The question now is whether we can really deliver on lifestyle,” said Ken Segarnick, chief corporate officer at Brandywine Living, a New Jersey-based operator of 32 luxury senior living communities in the Mid-Atlantic. “The game-changer is creating an environment that people want to age into.”