Moving to Action: Senior Housing Solutions for Serving the Middle Market: NIC Webinar Recap

Middle income seniors don’t have a wealth of senior living options. Either they don’t have enough money to afford a market rate community, or too much to qualify for an affordable place.

To address this widening gap, a panel of experts explored innovative solutions at a recent NIC webinar. About 1,000 people attended the February 1 session, which highlighted the business opportunity for industry stakeholders.

“The middle market has been underserved,” said Bob Kramer, co-founder and strategic advisor of NIC. “We need practical solutions for this huge and growing cohort.”

The session was led by NIC Head of Research & Analytics, Lisa McCracken. She was joined by Ryan Brooks and Caroline Clapp, both senior principals at NIC. They reviewed recent research to provide context for the discussion.

The shortage of senior housing for average Americans was first identified in NIC’s 2019 study, “The Forgotten Middle.” It was updated in 2022.

The number of middle-income seniors by 2033 will grow to 15.9 million, accounting for 44% of all seniors. About half will have chronic health conditions or mobility limitations. But only 2.2 million will be able to afford assisted living.

Due to a number of factors, middle market seniors face the dual burden of housing and care. “The private and public sectors have a lot of work to do,” said Clapp. The opportunity for the industry is to create a less expensive senior living model. “As the price point goes down, the potential market goes up,” said Brooks.

Defining the Middle Market

Middle income seniors are not all the same, cautioned Kramer. “There is no one-size-fits-all solution.”

The middle market can be divided into three income segments ranging from 60-150% of area median income (AMI). Kramer challenged providers to ask themselves:

* What part of the market are you seeking to serve?

* What level of services will you provide?

* What are the payment sources?

* What are the barriers to scale?

Financing a sustainable model is a big hurdle. A recent Milken report suggests four strategies: 1) Repurpose distressed properties; 2) Create a revolving loan fund; 3) Establish a value-based care delivery and payment model; and 4) Launch a senior housing-payer pilot partnership.

Two panelists presented their successful approaches.

Presbyterian Homes & Services targets the higher end of the middle market. “We maintain tight efficiencies and staffing ratios to bring down rents,” said Jon Fletcher, senior vice president at the organization. The goal is to tie increases in rents and expenses to the Consumer Price Index (CPI), so apartments remain affordable.

Innovation Senior Living repurposes distressed properties, growing in number post COVID. Buildings purchased at reduced prices can keep rents affordable, according to Pilar Carvajal, founder & CEO at Innovation. She also partners with healthcare and community service providers.

Panelist Lundat Kassa, vice president at Bellwether Enterprise Real Estate Capital, said that financing in today’s capital constrained market takes creativity. Lending sources are available, but public-private partnerships are needed to scale successful models.

McCracken wrapped up the session with a lighting round question. What key lever would produce more middle market senior housing?

Suggestions were to repurpose more underperforming properties and expand the definition of affordable housing used by policy makers to include the middle market.

More public subsidies and social impact investors are also needed. “We have the opportunity to solve this crisis,” said Carvajal.

CCRC Performance: Entrance Fee Occupancy Surpasses 90% in 4Q 2023

The following analysis examines occupancy and year-over-year changes in inventory, and same-store asking rent growth—by care segment—within entrance fee CCRCs and rental CCRCs in the 99 combined NIC MAP Primary and Secondary Markets. The analysis also explores the recovery of regional occupancy rates by majority contract type (entrance fee CCRCs vs. rental CCRCs) and compares the distribution of occupancy among different community types and by contract type during the fourth quarter of 2023.

Key takeaways

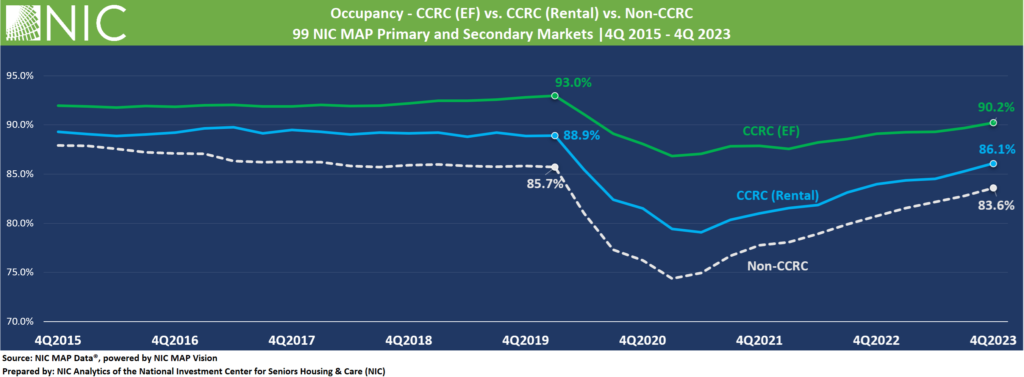

The occupancy rate for entrance fee CCRCs surpassed 90% in the fourth quarter 2023.

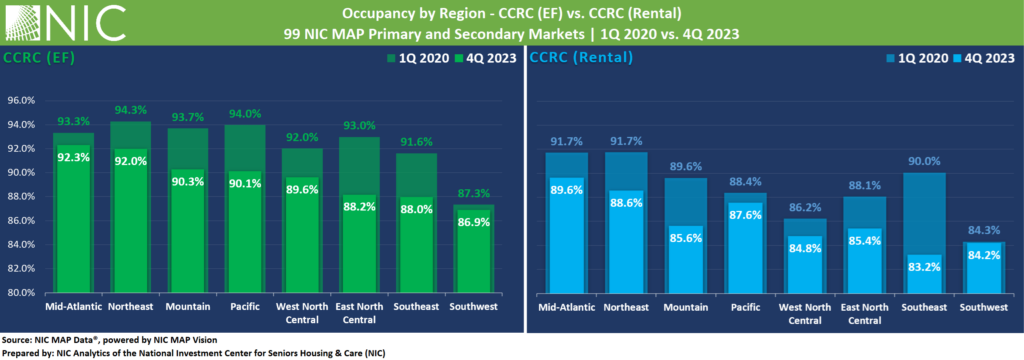

Entrance fee CCRCs maintained higher occupancy rates than rental CCRCs across all regions and care segments.

Occupancy rates and recovery timelines continue to be uneven across regions. In future publications, NIC Analytics will explore these regional differences to understand the underlying drivers.

The memory care segment within rental CCRCs experienced the smallest asking rate growth but the largest annual occupancy gain.

Nursing care Inventory within CCRCs is shrinking at a higher pace. There is a trend of CCRCs converting skilled nursing beds to assisted living or memory care units.

The Occupancy Rate for Entrance Fee CCRCs Surpassed 90% in the Fourth Quarter 2023. In the 99 NIC MAP Primary and Secondary markets, the occupancy rate for entrance fee CCRCs increased to 90.2%, 4.1 percentage points (pps) higher than rental CCRCs (86.1%) and 6.6pps higher than non-CCRCs (83.6%).

NIC Analytics recently published its first occupancy stratification report, which examines the distribution of stabilized occupancy within the senior housing sector in 2023. The report shows that CCRCs had the smallest share of communities with occupancy below 80% compared to other community types. Additionally, only about 10% of entrance fee CCRCs reported occupancy below 80%, less than half the share found in rental CCRCs and the smallest share across NIC MAP Vision dimensions comparisons.

Across all Regions, Entrance Fee CCRCs Maintained Higher Occupancy Rates than Rental CCRCs in the Fourth Quarter 2023. The largest differences in occupancy between entrance fee and rental were reported for the West North Central and Southeast Regions, where entrance fee CCRC occupancy was 4.8pps higher than rental, followed by the Mountain (4.7pps), and the Northeast (3.4pps).

Strong Occupancy Rates in Mid-Atlantic and Northeast. The Mid-Atlantic and Northeast Regions had the strongest occupancy rates for both entrance fee and rental CCRCs in the fourth quarter 2023. The occupancy rates within these regions with respect to contract type were well above the average occupancy rate for entrance fee CCRCs (90.2%) and rental CCRCs (86.1%) in the combined 99 NIC MAP Primary and Secondary Markets.

Mid-Atlantic and Southwest Regions Closest to Recovery. For entrance fee CCRCs, the Southwest and Mid-Atlantic Regions are the closest to fully recovering and returning to the occupancy levels of the first quarter 2020. The Southwest Region has reached 86.9% occupancy, while the Mid-Atlantic Regions is at 92.3%. Both regions are within 0.4pps and 1.0pps, respectively, of reaching pre-pandemic first quarter 2020 levels. As for rental CCRCs, the Southwest Region (84.3%) has fully recovered and returned to the occupancy level of the first quarter 2020.

In future publications, NIC Analytics will explore these regional differences to understand the drivers behind higher occupancy rates or faster recovery in some regions, and relatively lower occupancy rates or slower recovery in others.

4Q 2023 Market Fundamentals by Care Segment – Entrance Fee CCRCs vs. Rental CCRCs

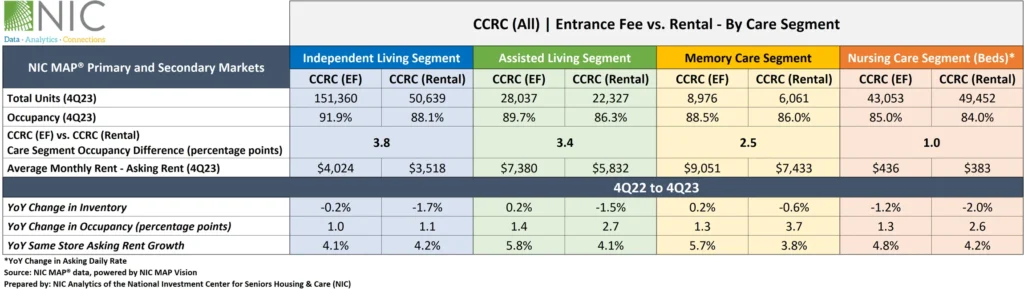

Occupancy. Overall, the occupancy rate for entrance fee CCRCs continued to outpace that of rental CCRCs across all care segments. The difference in the fourth quarter 2023 occupancy rates between entrance fee CCRCs and rental CCRCs was largest for the independent living segment (3.8pps) and the assisted living segment (3.4pps), and smallest for the nursing care segment (1.0pps).

The entrance fee CCRC independent living care segment had the highest occupancy (91.9%) in the fourth quarter of 2023, followed by entrance fee CCRC assisted living and memory care segments (89.7% and 88.5%, respectively).

In terms of occupancy improvements from one year ago, the largest occupancy gains for both entrance fee CCRCs and rental CCRCs were seen across assisted living and memory care segments, while the smallest gains were seen across independent living segments (1.0pps and 1.1pps, respectively).

Asking Rent. The monthly average asking rent for entrance fee CCRCs across all care segments remained higher than rental CCRCs. The highest year-over-year asking rent growth for entrance fee CCRCs was noted in the assisted living and memory care segments (5.8% to $7,380 and 5.7% to $9,051, respectively). For rental CCRCs, the largest year-over-year asking rent growth was noted in the independent living segment (4.2% to $3,518), while the smallest growth was seen in the memory care segment (3.8% to 7,433). Interestingly, the memory care segment experienced the largest annual occupancy gain (3.7pps) across all care segments and payment types.

Note, these figures are for asking rates and do not consider any discounting that may be occurring.

Inventory. Compared to year-earlier levels, nursing care inventory for both entrance fee and rental CCRCs continued to experience the largest declines (negative 1.2% and 2.0%, respectively). On the other hand, positive year-over-year inventory growth was reported for the entrance fee CCRC assisted living segments (0.2%) and memory care segments (0.2%).

Negative inventory growth can occur when units/beds are temporarily or permanently taken offline or converted to another care segment, outweighing added inventory. Anecdotally, there is a trend of CCRCs converting skilled nursing beds to assisted living or memory care units.

Look for future blog posts from NIC to delve deep into the performance of CCRCs.

Interested in learning more?

To learn more about NIC MAP Vision data, and about accessing the data featured in this article, schedule a meeting with a product expert today.

Initial Rate Growth and Discount Strategies in Senior Housing

The following analysis examines initial rate growth and discounts offered compared to asking rates across all senior housing care segments. Additionally, the analysis explores initial rate growth patterns within select NIC MAP® metropolitan markets reported by NIC MAP Vision.

Key Takeaways:

Initial rate growth remained robust and near record highs for assisted living and memory care but showed a slight deceleration for independent living.

Some markets saw negative year-over-year rate growth in initial rates in December 2023, contrasting with December 2022, when rates were positively growing, often in the double digits.

Average initial rate growth is expected to align with inflation in 2024, based on historical trends.

Discount strategies are being employed to offset higher initial rate growth and attract new residents.

The pace of move-ins appears to be a factor influencing these pricing strategies.

Independent living had the lowest average pace of move-ins in 2023, while memory care had the highest, followed by assisted living.

Discounts increased in independent living, held steady in assisted living, and declined in memory care.

In 2023, a NIC analysis revealed differences in rate increases and their effects on demand growth and occupancy recovery between independent living, often a lifestyle choice, and assisted living/memory care segments, which are primarily need driven. This trend is consistent across discount strategies.

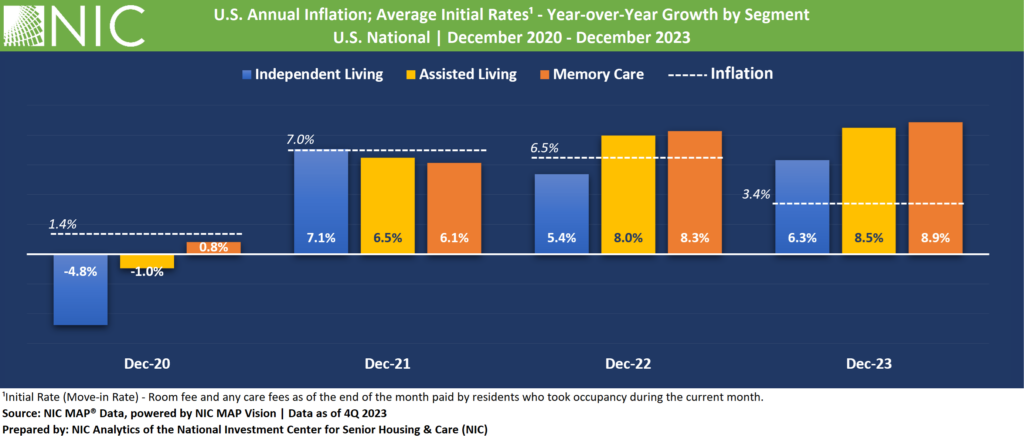

The Pace of Growth in Initial Rates Remained Robust and Near Record Highs for Assisted Living and Memory Care but Showed a Slight Deceleration for Independent Living

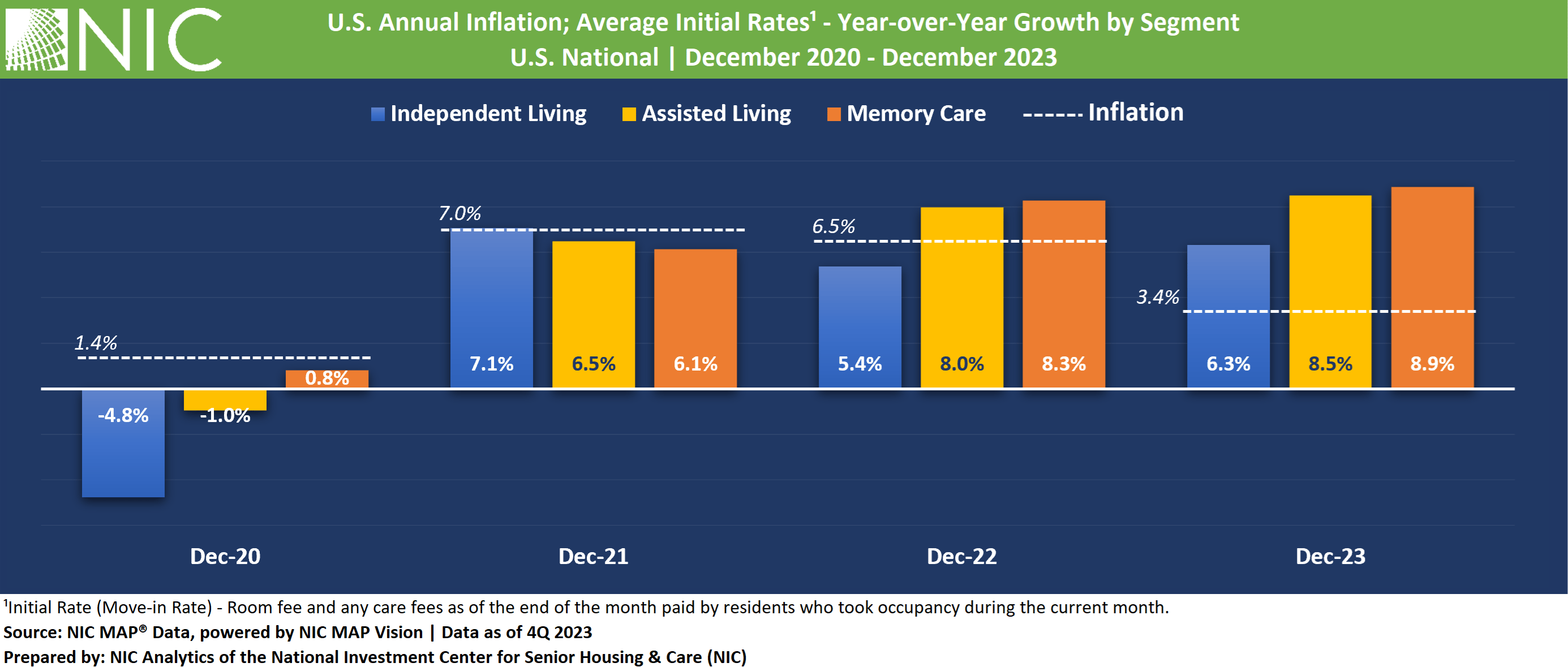

For the independent living segment, average initial rate growth peaked during the annual period ending December 2021, with the largest annual growth (7.1%) among all senior housing care segments. However, this pace of growth decelerated in the following annual periods ending December 2022 (5.4%) and December 2023 (6.3%), with initial rate growth being the lowest compared with assisted living and memory care segments.

This deceleration may be partly attributed to relatively slow move-ins for independent living and increased competition from active adult properties. Notably, the pace of move-ins for independent living averaged around 2.3% of inventory in 2023, less than that of assisted living (3.3%) and memory care (3.6%).

The assisted living segment experienced relatively higher year-over-year increases in average initial rates compared to independent living in December 2022 and December 2023, with 8.0% and 8.5%, respectively.

The memory care segment showed the largest year-over-year increase for initial rates among the three care segments, with an 8.3% increase in December 2022 and an 8.9% increase in December 2023.

In December 2023, the average initial rate for an independent living unit was $3,702, translating to $44,424 annually. For an assisted living unit, the average initial rate was $6,017, equivalent to $72,204 annually. For a memory care unit, the average initial rate was $7,899, equivalent to $94,788 annually.

Separately, inflation rates, as measured by the Consumer Price Index (CPI), were 7.0% in December 2021, 6.5% in December 2022, and 3.4% in December 2023. Despite a noted easing of inflation, initial rate growth for all segments continued to outpace inflation as of December 2023, indicating that senior housing operators maintain the upper hand in pricing.

While these rate adjustments are being made to account for increased care and operating costs due to inflation, the pace of growth in rates is expected to align with inflation at some point in 2024. This projection is based on historical trends and the observed 6-to-9-month lag between rate growth and inflation that was observed in 2022.

Discounts and Initial Rate Growth Vary by Care Segment and Market

Interestingly, some markets experienced negative year-over-year growth in initial rates in December 2023. For example, in the assisted living segment, Cincinnati, OH and Dallas, TX, saw declines of 7.1% and 1.8%, respectively. Similarly, Detroit and Houston experienced decreases of 15.6% and 7.3%, respectively, in the memory care segment. This contrasts with December 2022, when year-over-year growth in initial rates across these markets and care segments was positive, often in the double digits.

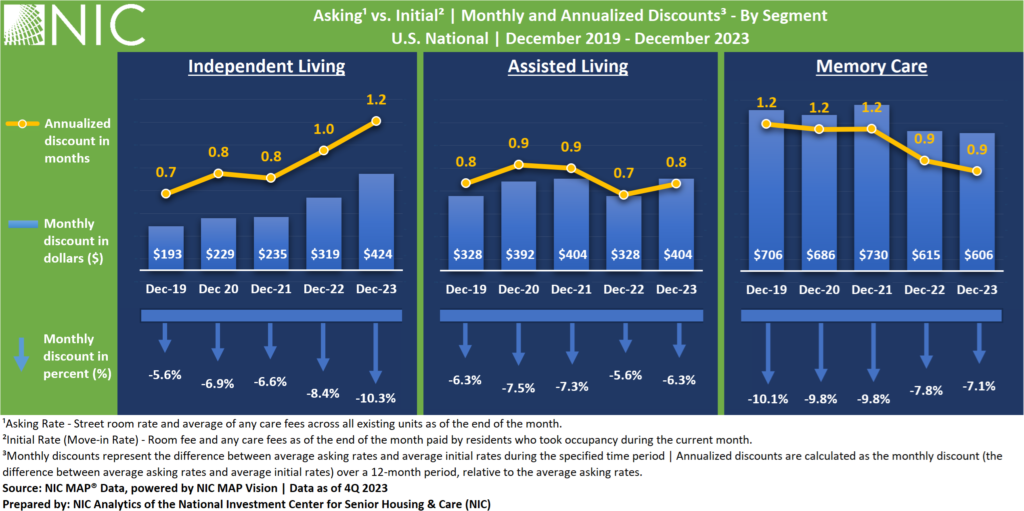

Discounts Increased in Independent Living, Held Steady in Assisted Living, and Declined in Memory Care

In 2023, a NIC analysis revealed differences in rate increases and their effects on demand growth and occupancy recovery between independent living, typically a lifestyle choice, and assisted living/memory care segments, which are primarily need-driven. This trend is consistent across discount strategies.

In the independent living segment (frequently more of a lifestyle choice than need-driven), discounts between asking rates and initial rates have been increasing since December 2019. averaging 10.3% or $424 off the asking rate in December 2023, equivalent to 1.2 months on an annualized basis.

Initial rate discounts compared with asking rates in the assisted living segment were relatively lower and remained generally consistent with discounts offered since 2019, averaging 6.3% or $404 in December 2023, equivalent to 0.8 month on an annualized basis.

In the memory care segment, discounts between asking rates and initial rates averaged 7.1% in December 2023, equivalent to $606. Despite the relatively higher rate increases for the memory care segment, annualized discounts have been decreasing in the last two years, from 1.2 month in December 2021 to 0.9 month in December 2023.

These trends and patterns also suggest that the pace move-ins – lowest independent living and highest in memory care – had some impact on the discounts being offered.

In conclusion, the analysis raises some important questions: Are these pricing strategies sustainable? What is the long-term effect of these discount strategies on resident retention and the pace of move-ins and move-outs? Will senior housing properties maintain the upper hand in pricing as inflation continues to moderate?

Additional key takeaways are available to NIC MAP Vision subscribers in the full report.

NIC MAP Vision continues to work to onboard new data contributors and is dedicated to reporting more metropolitan markets. It is only with the support of Actual Rates data contributors and officially certified Actual Rates software partners that expanded metro-level reporting is now available. For more information on which metropolitan markets are now available to NIC MAP Vision subscribers, please contact a product expert at NIC MAP Vision today.

About the Report

The NIC MAP Vision Seniors Housing Actual Rates Report provides aggregate national data from approximately 300,000 units within more than 2,700 properties across the U.S. operated by 35 to 40 senior housing providers. The operators included in the current sample tend to be larger, professionally managed, and investment-grade operators as we currently require participating operators to manage 5 or more properties. Note that this monthly time series is comprised of end-of-month data for each respective month, and that the set of properties included in each month’s data set is subject to change. The sample is not “same store,” and occupancy is inclusive of newly opened properties in lease-up. NIC MAP Vision is working on including same-store rate metrics in a future release.

Interested in Participating?

The Actual Rates Data Initiative is an effort to expand senior housing data and we are looking for operators who have five or more properties to participate. NIC MAP Vision has expertise in extracting data from industry leading software systems, such as Aline, Alis, Eldermark, MatrixCare, Move-N, PointClickCare, Vitals, and Yardi and can facilitate the process for you.

Operators contributing data to the actual rates report receive a complimentary report which allows them to compare their own data against national and metropolitan market benchmarks. In addition to receiving a complimentary report, your organization benefits through:

More informed benchmarking, strategic planning, and day-to-day business operations,

Increased transparency, aligning with other commercial real estate assets in terms of data availability,

Saved time, Actual Rates data is collected electronically directly from operators’ corporate offices, removing the need for telephone calls to individual properties, and

Enhanced investment and efficiency across the sector.

Expect Continued Pressure on Skilled Nursing Margins in 2024

Many skilled nursing experts project that 2024 may be a critical juncture for the industry. The growth of the aging population is expected to lead to increases in occupancy rates for skilled nursing operators.

As we venture through 2024, the skilled nursing sector is preparing to navigate the challenges and seize the opportunities that lie ahead. The sector is focused on securing increased funding, enhancing public education about the sector, and addressing the ongoing workforce challenges.

Many skilled nursing experts project that 2024 may be a critical juncture for the industry. The growth of the aging population is expected to lead to increases in occupancy rates for skilled nursing operators. According to the fourth quarter 2023 data from NIC MAP Vision, at82.7%, skilled nursing occupancy has recovered 9.3 percentage points from the pandemic low (1Q2021, 73.4%), but is still 3.5 percentage points below 1Q2020 levels.

Given the challenges such as continued occupancy below pre-pandemic levels, operators have had to pivot and adjust to a more difficult operating environment in recent years.

Many operators have increased focus on key operational improvements during this time. Operators are implementing strategies to enhance efficiencies and concentrating on staffing headwinds. For example, strategies that utilize data to drive outcomes with the assistance of Artificial Intelligence (AI) have proven beneficial. Many believe AI has the potential to reduce routine administrative burdens, guide clinicians to better outcomes, and improve the quality of care. Additionally, there is an aim to increase clinical competency among staff through enhanced apprenticeship programs and internal educational courses. Efforts are also being made to address staffing issues by focusing on diversity, equity, and inclusion initiatives.

A positive for the sector has been the increase in Medicaid reimbursement rates in many states. The increases have been essential in mitigating expense pressure for operators. However, some believe there is a possibility the sector will face financing threats due to the recalibration for Medicaid rates. In an attempt at budget neutrality, states typically withdraw funds that they initially allocated, in an effort known as “recalibration.” If this comes to fruition, it could pose more of a challenge for rural and smaller skilled nursing properties, rather than to larger ones. Many would also agree that while these increases have been beneficial, they have lagged for many years and, in many cases, still do not fully cover the cost of care provided.

As mentioned above, expense pressure is palpable, and this is leading to the squeeze in profit margins. This is due to a combination of factors, including continued wage-related and workforce expenses, rising interest rates and general inflationary cost increases. These economic pressures are driving up operating costs, thereby reducing the profitability of skilled nursing properties.

Another factor contributing to the margin squeeze is the growth of Medicare Advantage. The growth of Medicare Advantage (MA) plans has been challenging for operators, impacting margins, and sometimes leading to issues of high claims denials for service providers. High claim denials can result in an additional administrative burden during a time when nursing home staff is already stretched thin, in addition to increasing expenses due to higher bad debt items. Furthermore, operating revenue is pressured due to lower Medicare Advantage reimbursement compared to Medicare Fee-for-service. The Medicare versus Managed Medicare differential from the October NIC MAP Vision Skilled Nursing Data Report revealed that MA plans were reimbursing $123 less per patient day compared to traditional Medicare. The disadvantages of MA plans to providers have led a number of skilled nursing entities to explore ownership of their own MA plan and other value-based care arrangements where there is the potential for upside risk.

Last, there are concerns regarding the proposed federal staffing mandate as the sector continues to strive for better quality of care. Many believe this mandate could potentially compromise the quality of care and limit accessibility for many Americans, in addition to causing significant financial viability problems and potentially resulting in the closure of additional properties.

While there are demographic tailwinds, skilled nursing operators are facing a multitude of challenges in 2024. However, with strategic planning and effective advocacy, operators can navigate these challenges and continue to provide quality care for their residents. The industry remains hopeful that with predictable funding, long-term solutions to some of the most critical problems facing the industry can be addressed, ensuring the quality care our seniors deserve and paving the way for a sustainable future for skilled nursing services.

3Q 2023 Lending Trends in Senior Housing and Nursing Care Reflect Adjustments to New Economic Realities

NIC Analytics released the3Q 2023 NIC Lending Trends Reporttoday. The complimentary quarterly report includes data trends over seven years for senior housing and nursing care construction loans, mini-perm/bridge loans, and permanent loans from 3Q 2016 through 3Q 2023.

Third Quarter 2023 and Beyond: Market Forces Recap

The Federal Reserve nudged rates higher by another 0.25 percentage points (pps) in July 2023, bringing the federal funds rate to a target range of 5.25% – 5.50%. This was the eleventh rate hike since March 2022. Concurrently, the consumer price index (CPI), has decelerated since June 2022, reaching 3.0% in June 2023 before rebounding to 3.7% in August and September of 2023.

Despite a noted easing of inflation in the past year, the Federal Reserve acknowledged its persistent elevation. Since July 2023, the Federal Reserve held rates steady for four consecutive meetings, including the most recent one in January 2024. The omission of any mention of further rate hikes in the Federal Reserve’s statement suggests a more balanced outlook regarding the risks associated with reaching its employment and inflation targets. However, the central bank remains vigilant about adjusting monetary policy as needed to address emerging risks.

Looking ahead, the expectation is for any potential rate cuts to occur gradually, involving SMALL incremental adjustments. The goal is to recalibrate and align interest rates with inflation to support overall economic health and mitigate inflationary pressures or deflationary risks.

Escalating loan expenses due to higher interest rates are impacting senior housing property assets, creating challenges for many and distress in certain others. The sector anticipates billions of dollars maturing this year. While somemay endure the repercussions of high interest rates, more stability is anticipated in 2025 for those that can weather the current conditions, with an expected improvement in capital market conditions, occupancy, and NOI outlook.

The lending environment for senior housing and nursing care in the third quarter of 2023, although tighter compared to 2020, showed relatively similar conditions to the second quarter 2023 with some adjustments from both borrowers and lenders.

Takeaways from the 3Q 2023 NIC Lending Trends Report

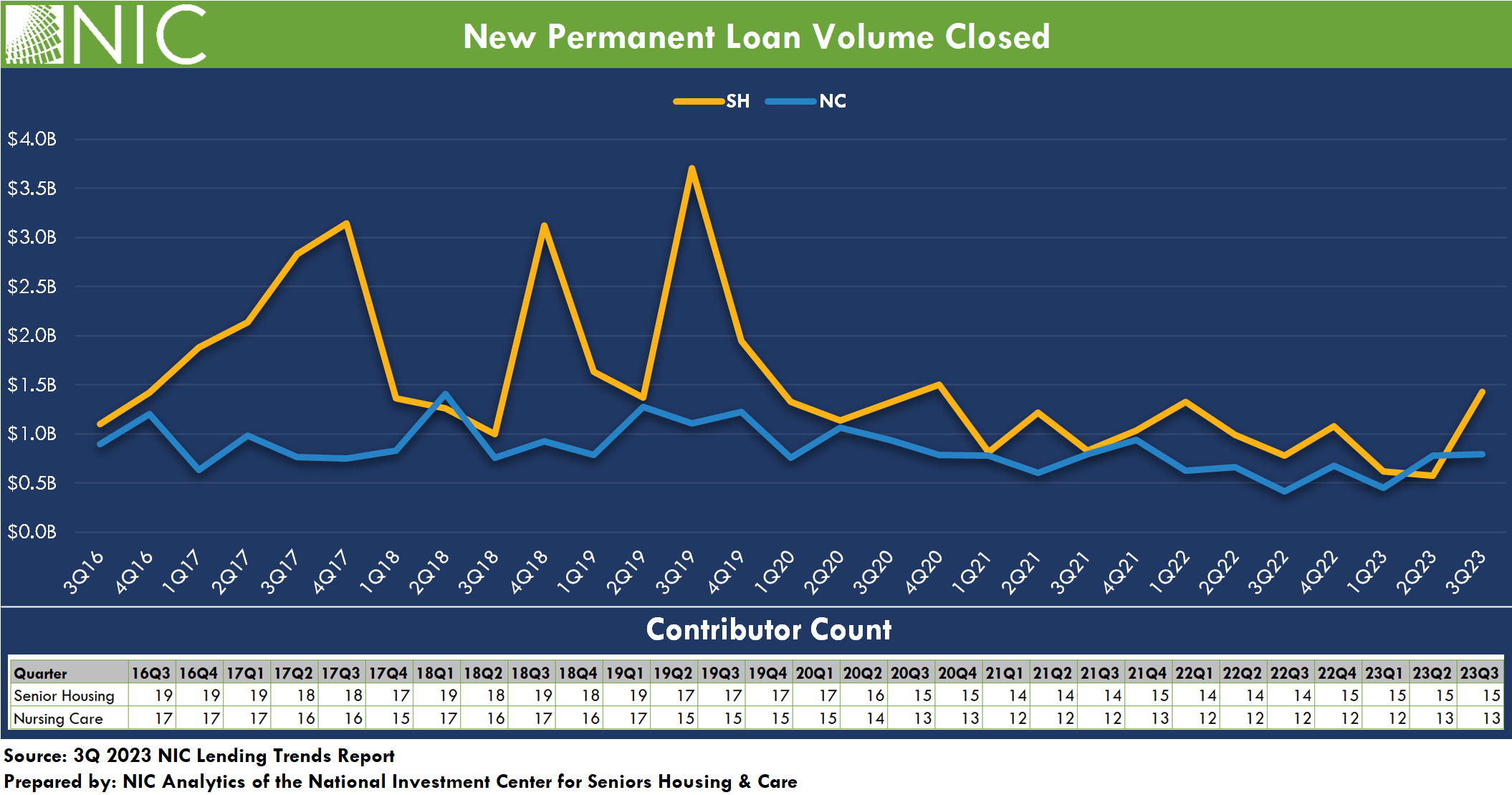

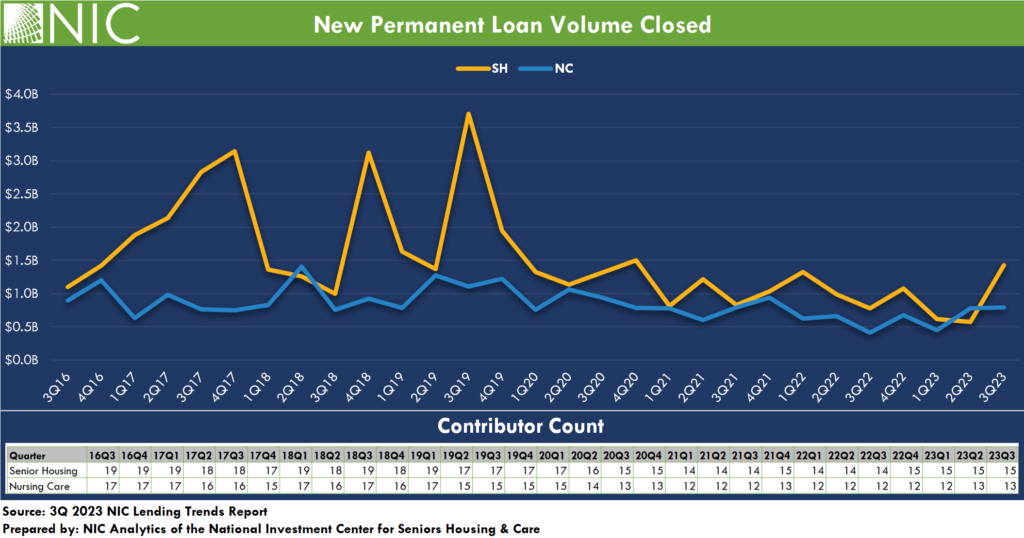

The issuance of new permanent debt for senior housing increased during the third quarter 2023. For the sample of lenders in the NIC Lending Trends Report,the volume of new permanent loans closed for senior housing surged to $1.43B, marking a 150% increase from the prior quarter. This increase suggests that some lenders and borrowers are likely adjusting to changing capital market and credit conditions and locking in long-term interest rates. However, the levels remained relatively low compared to the high volumes observed pre-2020.

The decline in mini-perm/bridge debt issuance for senior housing persisted and reached time-series low, reflecting a further 46% decrease from the prior quarter and 87% from late 2022 levels. Similarly, nursing care mini-perm/bridge loan closings, while slightly higher than those in senior housing for the past two consecutive quarters, remained relatively low and on par with pre-pandemic levels. Borrowers continue to adjust to the prevailing “higher for longer” mindset, anticipating sustained rates without a potential decline in the near future. While short-term debt options are limited, those available often come with increased costs and additional credit enhancements e.g., the need for more equity or a repayment guaranty.

New construction loan closings for senior housing subdued to weak levels and hit a new low within the time series in the third quarter of 2023. This is evident in construction starts which remained relatively feeble in the third quarter of 2023, and the number of senior housing units under construction in the 31 NIC MAP Primary Markets which remained near its lowest level since 2015, according to data released by NIC MAP Vision.

This notable decline suggests a trend of diminishing confidence in a quick construction market correction. Despite this, the consensus points towards mid- or late-2024 as the most likely period for senior housing construction starts to reach their lowest point.

As for nursing care, the issuance of construction debt was virtually non-existent for the lenders sampled in the Lending Trends Report. This aligns with the observed pattern of limited debt financing for new nursing care property construction since NIC began data collection in 2016.

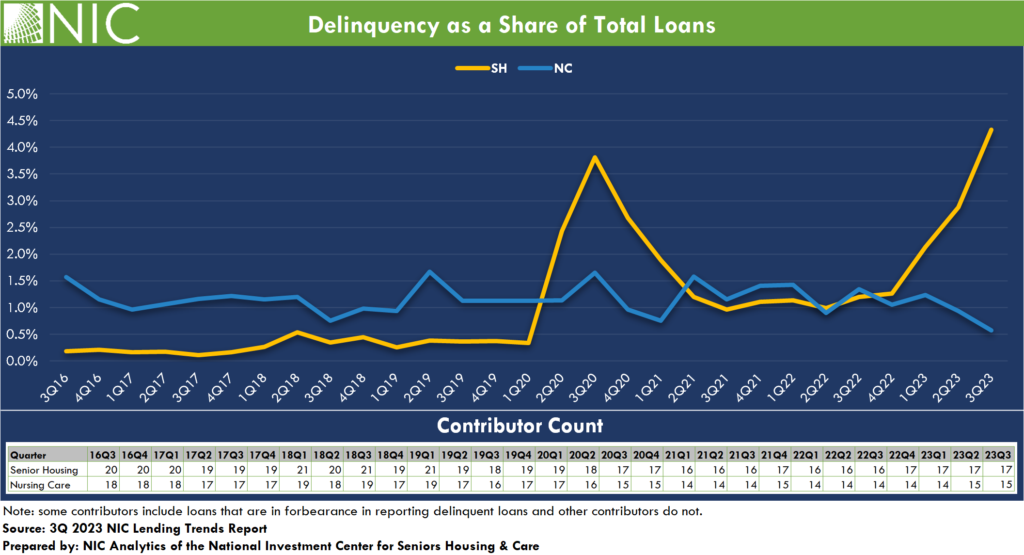

The total balance of delinquent loans for senior housing saw a notable increase to time-series high. Delinquencies in senior housing rose by 50% in the third quarter 2023 while those in nursing care declined by 38% from the prior quarter. Delinquencies as a share of total loans rose to 4.3% for senior housing, up from 2.9% in the second quarter of 2023 and 1.3% in late 2022. For nursing care, the delinquency rate edged down to 0.6% from 1.1% in late 2022. Note that loans in forbearance are reported in the delinquent loan data for some debt providers. Also of note, foreclosures were reported for the sample in third quarter 2023 for both senior housing and nursing care, $20.2M and $14M, respectively.

From the Field: 3Q 2023 Survey Comments

For the past three quarters, NIC Analytics has reached out to our network of lender data contributors to this report, asking them questions about the lending environment for senior housing and nursing care. We are asking about their strategies in response to changing capital market conditions, lending patterns with respect to existing versus new clients, and any notable trends they are observing in the market.

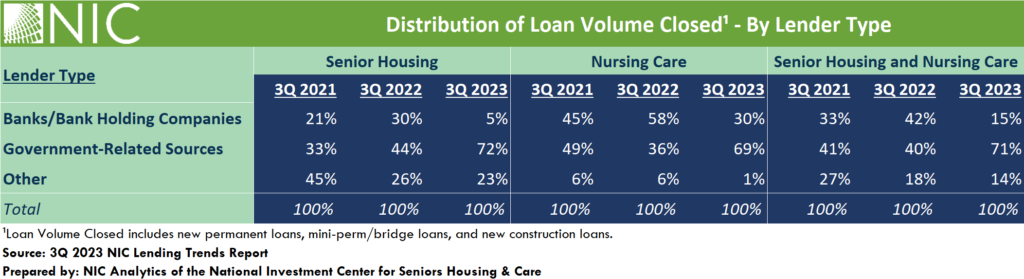

In the face of changing capital market conditions, the responses in the third quarter 2023 were diverse. Approximately two-thirds reported tightening lending standards, but credit requirements aligned with the first half of 2023, while a third maintained base credit standards but focused on strong sponsorship and credits opportunities due to reduced credit availability from banks. As the exhibit below shows, over the past three years, there has been a decline in the share of loan volume closed by banks and other lenders, juxtaposed with a rise in the share of loan volume closed by government-related sources (based on this sample of lenders captured by NIC).

The third quarter of 2023 also prompted greater focus on long-term relationships with many lenders extending loans predominantly to existing clients, acknowledging persisting challenges posed by rising short-term and long-term interest rates, staffing issues, slow census recovery in some cases, and inflationary increases in operating costs. Although some lenders onboarded new clients despite tightened lending standards.

Additionally, lenders noted that many properties displayed improved three-month NOI over 12-month NOI, but the surge in interest rates and cap rate trends sometime offsets potential loan proceeds. Further, the impact of higher interest rates caused some loans to become debt service constrained and resulted in adjustments to requested loan amounts to meet minimum DSCR requirements.

In conclusion, the third quarter “from the field” survey reflects the adaptability of senior housing and nursing care lenders and borrowers to new economic realities in the face of shifting market conditions. The industry grapples with a balancing act – tightening standards to navigate challenges while seeking opportunities to position themselves for the road ahead.

Download the complimentary 3Q 2023 NIC Lending Trends Report for full details on these and other trends in senior housing and skilled nursing lending.

Note: These data are not to be interpreted as a census of all senior housing and skilled nursing lending activity in the U.S., but rather reflect lending activity from participants included in the survey sample only.

The 4Q 2023 NIC Lending Trends Report is scheduled for release in mid-May 2024.

Interested in participating? The NIC Lending Trends Report helps NIC Analytics to deliver on NIC’s mission to enable access and choice by further enhancing transparency of capital market trends in the senior housing and care sectors. We very much appreciate our data contributors. This report would not be possible without them.

If you would like to participate and contribute your data, please contact us at analytics@nic.org. As a courtesy for providing data, data contributors receive this report ahead of its publication on the website. The information provided as part of the survey will be kept strictly confidential. Individual answers will be combined with the answers of all other respondents. Data acquired from this survey will only be reported in the aggregate, and therefore, the resulting aggregated data will not be attributed to you or your company upon distribution.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. NIC's privacy policy can be viewed here. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.