Rate of New COVID-19 Infections in Skilled Nursing Facilities Continues to Plummet*

NIC’s Skilled Nursing COVID-19 Tracker, featuring CMS data updated as of January 31, 2021, shows newly confirmed COVID-19 cases within skilled nursing facilities continue to plummet.

The per-resident rate of new COVID-19 infections continues to plummet in skilled nursing facilities, with a two percentage point drop and a likely continued downward trend.

“There is light at the end of the tunnel, and we don’t think it’s a train,” said a participant in a recent NIC Community Connector™ Meetup.

NIC’s Skilled Nursing COVID-19 Tracker, featuring the latest CMS data updated as of January 31, 2021, shows that newly confirmed COVID-19 cases within skilled nursing facilities continued to plummet. For the week ending January 31, the per-resident rate of new COVID-19 infections dropped to July levels as skilled nursing facilities reported a two percentage point drop in infections from 3% on December 20 when the Long Term Care (LTC) vaccination program was launched to 1% on January 31. The chart below depicts this decline.

New COVID-19 confirmed cases within skilled nursing facilities continued to fall at a faster pace compared to the U.S overall new cases. Notably, new confirmed cases within skilled nursing facilities are down 49% from 32,521 on December 20 to 16,701 on January 24, while U.S. new reported cases are down 24% over the same period.

Since January 31, U.S. COVID-19 cases have continued to fall steadily. On February 16, the rolling daily average of new infections hit its lowest level since October. In addition, the count of people receiving two doses of the COVID-19 vaccines as reported to the CDC in the Federal Pharmacy Partnership for Long-Term Care (LTC) Program nearly tripled in the first two weeks of February, from 641,561 on January 31 to 1,711,846 on February 16.

This continuing decline in U.S. cases along with the increase in vaccine supply and administration spark hope and suggest that new coronavirus cases in skilled nursing facilities are likely to continue trending lower in the next two reporting weeks ending Feb 7 and Feb 14.

The Skilled Nursing COVID-19 Tracker also shows that the share of properties reporting new COVID-19 infections fell from 34.5% on December 20 to 24.4% on January 24. Additionally, newly confirmed cases among staff are declining at the same pace as the new cases among residents.

“The drop in new cases is becoming evident in CMS data since vaccines have been administered and distributed in skilled nursing properties. While data suggest that we are entering the beginning of the end of this pandemic, it is still important to realize that we need vaccinations in combination with other interventions, including more frequent testing, greater emphasis on physical distancing, and adherence to masking guidelines. These interventions continue to be an effective and vital weapon against the rate of mutation of the virus and the spread of current virus strain until vaccines are widely accepted and distributed and herd immunity is achieved,” said NIC Chief Economist, Beth Mace.

* Blog and graph updated as of February 19, 2021

Takeaways and Highlights from Payments, Policy, & Capital Summit

Skilled Nursing News’ Payments, Policy, and Capital Summit brought together executives, policy professionals, and capital providers to share their thoughts on the skilled nursing industry.

Skilled Nursing News’ Payments, Policy, and Capital Summit brought together executives, policy professionals, and capital providers to share their thoughts on the recent past, present, and future of the skilled nursing industry. Highlights and key takeaways from the three-day virtual event are summarized here.

The summit included sessions on capital and one main topic of discussion was private equity and skilled nursing. In regard to investor interest in skilled nursing, private equity has been the bright spot in terms of buying skilled nursing properties even as the sector endured its most challenging year on record in 2020. One theme, however, has been the flight to quality as investors are interested in the best operators and properties in order to mitigate risk when allocating new capital. Private equity is still excited about the opportunity in the future as long-term care needs will remain given the fact that a very large population will be very sick with multiple illnesses and will not be able to afford private pay assisted living and unable to receive care in the home 24 hours a day.

However, in the short-term private equity does have concerns given the challenges, hence the flight to quality operators and properties. Indeed, the difficulty in operations continues. Skilled nursing occupancy was at 74.2% as of November 2020 based on data from the recent NIC MAP Skilled Nursing Data Report, representing a 11.2 percentage point drop from February 2020.

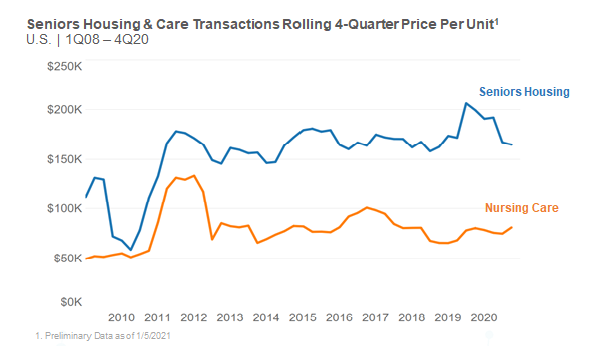

Despite the operational challenges, some owner/operators and families with plentiful capital have been the main buyers throughout the pandemic. In fact, according to preliminary fourth quarter 2020 data from NIC/RCA private buyers closed on $4.2 billion worth of seniors housing and care transactions for the year of 2020, which represented 57% of the volume. In addition, and perhaps an example of the flight to quality, skilled nursing (nursing care in the graph below) property price per bed has held firm according to NIC/RCA price per bed data (see graph below for details and sources). This pricing trend below is a national rolling four-quarter measure and it is not same-store; the mix of properties could impact the results. However, it does reflect what is trading in the market albeit with relatively lower transactions closed in 2020 due to the pandemic.

One of the comments made during the summit was that there were many transactions closed over $100,000 price per bed. So, what does this say as price per bed holds firm during this time of crisis? For one, the properties trading could be higher quality with good operators, as stated previously. In addition, there is still a very attractive expected spread in terms of the interest rates on debt and the expected long-term cash flow of a high-quality property, which may be supporting price levels.

Also, it was mentioned during the summit that government support has been a positive and private equity may be reassessing the “stroke-of-pen risk,” which is the risk that reimbursement rates are cut by the government. However, given the support of government funds during the pandemic investors may reassess the risk of government involvement as it has helped the sector stay afloat during this particular crisis. Lastly, there are some small private investors, owners and/or operators looking to expand regionally and have strong long-term views about the sector.

Much of the investor interest discussion, and the success of the sector, was certainly based on the quality operators but much of that quality is based on top talent and staff. It was mentioned that staff turnover was a top leading indicator of a successful operation before the pandemic and the belief is that is still the case. Staffing will continue to be a challenge now and after the pandemic and it should be a priority for both investors and operators alike to ensure the proper staffing is in place for all stakeholders.

As for what to expect on the policy and regulatory front, panelists covered labor and workforce topics such as the potential increase in minimum wage and mandatory staffing ratios, as well as what the future holds for PDPM, value-based purchasing, and risk-sharing models.

The Path to a $15 Minimum Wage

There are several states where a significant portion of the CNAs make less than $15 per hour – often starting at $9 or $10 per hour depending on market. With the new administration, there is certainly more discussion around a $15 minimum wage, which is a concern for many operators. As you might expect, states with the lowest CNA wages are the states that have really low Medicaid rates. As a result, providers simply do not have the resources to pay more than they are paying. Mark Parkinson, President & CEO, AHCA/NCAL emphasized that “if you do the minimum wage, you have to create a Medicaid mechanism that helps these states to pay for these wage increases.”

The upcoming stimulus bill will be passed with the reconciliation procedure, which requires only 51 votes. As a result of passing through reconciliation, there are only certain things that can be included in the bill, and currently, the prevailing view is that a minimum wage increase cannot legally be included. There is still a slim chance it’s ruled that the minimum wage increase can be included in the bill, but even if that is the case, it’s not clear that all Senate Democrats would vote for it. Additionally, the Biden proposal on minimum wage does increase the minimum wage to $15 per hour, but it is done with a gradual, phased approach, meaning the $15 wage would not be realized until 2025.

Other Regulatory Implications to Staffing

There’s good data available that indicates buildings with significant amounts of RN coverage, relative to buildings that didn’t, fared better with regards to COVID-19 cases and deaths. This may mean that there could be minimum staffing requirements established for the skilled nursing sector. Less likely, but still possible, could be including infection control experts within each of these sites as well. The caveat to successful implementation of these staffing minimums, however, is that these need to be funded under Medicaid for operators to be able to actually execute on these.

Enforcement – What Will be Scrutinized?

Given that nominated HHS Secretary Xavier Becerra is an Attorney General, it’s almost inevitable that oversight of skilled nursing will increase. One of the first things Seema Verma, former CMS Administrator, did was to issue a proposal that slowed down much of the requirements of participation that she felt had gone too far. The proposed rule was never finalized, and it is unlikely the Biden administration will finalize the rule.

There was a noticeable drop in civil monetary penalties (CMPs) under the Trump administration, but there may be pressure to get them back to where they were under the Obama administration. Right now, without an identified CMS Administrator and several important positions at CMS still open, there are a lot of unknowns, but that is likely to be on the table. The Biden administration is also going to take a close look at arbitration to see what can be done to decelerate its use.

There’s going to be a real push by the states to get rid of multi-resident rooms, specifically those that house 3 or 4 residents in a single room. This was brought to light as particularly problematic during the pandemic and private rooms are not only important for infection control, but also for quality of life and resident satisfaction as well.

Patient Driven Payment Model

The Patient Driven Payment Model – PDPM – has been one of the bright spots for the skilled nursing sector over the last year and a half. Despite concerns that the new payment system was not budget neutral, there were no substantive changes made to PDPM in 2020. This was in large part due to the COVID-19 pandemic overshadowing the concerns that some may have had about PDPM, and that may wind up being the case for 2021 as well. At some point the dust is going to settle and CMS will look again at the budget neutrality of PDPM.

There are some reasonable arguments to be made that could protect the gains that were realized under PDPM. First and foremost is that, as a whole, Medicare spending was down in 2020. Taking a step back and looking at the overall system puts PDPM in a better light.

Value-Based Purchasing

With the COVID-19 pandemic taking the full focus of the skilled nursing sector in 2020 and continuing into 2021, discussions about value-based purchasing and unified payments systems were not as prominent as they had been in the past. Once the pandemic is finally behind us, however, these conversations will once again become a more pressing topic.

As Scott Pilgrim, CEO, Diakonos Group points out, skilled nursing operators can secure additional Medicaid dollars, but must promise increased quality in return. Pilgrim notes that there are four mechanisms to increasing reimbursement rates under Medicaid and that policymakers see value in tying value-based purchasing to each of these four levers: base-rate increases, add-on rates, provider tax implementation, and inter-governmental transfer programs.

Risk-Sharing Arrangements – Medicare Advantage & Special Needs Plans

Medicare Advantage continues to grow, and that will continue to be the case. Market share for Medicare Advantage is approximately 35% and increasing each year by another 1%. I-SNPs provide an incredible incentive for operators to keep residents healthy. The COVID-19 situation was an incredibly difficult situation to navigate for I-SNPs, especially to those in the northeast. They were responsible for the entire risk of these residents, and in some cases were responsible for massive hospitalization bills. In other parts of the country, even with COVID, I-SNPs had done reasonably, as other medical expenses were down so much. All that being said, it’s clear that when the pandemic is finally behind us, risk-sharing type of arrangements are going to be an absolute must for providers that want to thrive.

Listening to all the potential policy and regulatory changes on the horizon made it clear: calls to reform post-acute and long-term care following the COVID-19 public health emergency, along with a new Presidential administration, mean the climate is ripe for potential regulatory changes to be implemented.

Fact or Fiction: Lending Markets During a Pandemic, and Beyond

Hundreds of investors, owners, operators, analysts, and other industry stakeholders attended the latest in NIC’s new series of Leadership Huddle events Wednesday.

Hundreds of investors, owners, operators, analysts, and other industry stakeholders attended the latest in NIC’s new series of Leadership Huddle events Wednesday. In the webinar portion of the event, which was sponsored by National Health Investors (NHI), they were treated to a virtual smorgasbord of insights and expert discussion around financing markets in seniors housing and care. Attendees who had opted to participate in the Zoom discussion breakout session that followed, continued the discussion, adding their own thoughts and experiences in small groups.

Seniors housing financing markets have evolved over the course of the COVID-19 pandemic—as lenders and owners both adapted in real-time—to unprecedented asset-level revenue declines exacerbated by operating expense increases. In a “fact or fiction” Q&A-based format, an expert panel, including both lenders and borrowers, explored what really occurred during 2020 from a lending perspective, how transactions are being quoted currently, and what the near- and long-term future will hold for seniors housing debt. Co-facilitators Joel Mendes, Senior Director, JLL Capital Markets, Seniors Housing, and James Thompson, Senior Vice President, Director of Senior Housing Investments, BOK Financial, came prepared with a variety of “fact or fiction” questions, designed to elicit honest, insightful responses on how lenders, owners, and others in the industry are thinking and behaving during this extraordinary time. Panelists Robb Chapin, Chief Executive Officer, Bridge Seniors Housing Fund Manager, LLC, and Steven Schmidt, National Director, Seniors Housing Group, Freddie Mac, fielded the questions.

On whether COVID-19 has reduced investor interest in seniors housing funds, Chapin responded, “that’s a hard fact, for sure.” He said that his group shelved those funds in the first six months of the year, focusing instead on the operational challenges brought on by the pandemic. For the rest of the year, he saw “10% to 15%” of normal flows of investment.

Mendes, responding to a question on non-recourse acquisition financing in 2020, suggested that the most-used term within the industry last year was “hit the pause button.” Permanent lenders such as Fannie Mae and Freddie Mac underwrote fewer loans as in-place cash flows, which they require to support their loans, declined throughout the year. Further, the non-recourse bridge debt market, according to Mendes, “did not fully materialize until later in 2020.”

Asked whether Freddie Mac’s senior housing portfolio has fared well, Schmidt responded, “relative to what we’ve heard from other lenders, that is predominantly true.” However, he said that the pandemic caused more stress in the seniors housing sector than did the global financial crisis. Freddie Mac instituted a three-month forbearance program, which he said was taken up by twice as many in seniors housing than in multifamily. The good news, according to Schmidt, is that most of those borrowers are now current. “We feel the program provided the necessary relief during the worst part of the pandemic, and we feel very good about that.”

Another line of questioning concerned the impact of regulators throughout the pandemic. Generally, panelists were positive, lauding the CARES Act, the Federal Reserve, who took action to temporarily ease balance sheet requirements, and PPP loans, all of which helped stabilize the sector throughout 2020.

Other questions focused on the present situation. The first of these concerned whether debt markets are a hindrance to the desire to buy and build new assets. Chapin labeled this one as a fiction, indicating that his organization was generally pleased with the response from lending relationships. He said, “we anticipate that we will continue to have very good outcomes with our lenders as it relates to refinancings and new acquisitions in 2021.” He continued, saying, “What we’re generally seeing is more conservative underwriting on debt service coverage ratios, lower LTVs, increased underwriting expenses for PPE, labor, insurance, and all the typical things that we’re all experiencing right now that have to be factored in.” He said that, although his company isn’t planning any new ground-up development projects for 2021, they expect to have shovel-ready projects in 2022.

Another “fiction,” according to Mendes, is that “new development financing terms are so conservative as to render them non-existent.” On the contrary, he said, “we closed new development debt financings all through 2020 and continue to do so today.” He said, “If I could pick one financing term that has changed the most since March 2020, I’d say it’s ‘recourse.’ Lenders are requiring more of it. Non-recourse debt financing, particularly that starts with a six on the loan-to-cost, is pretty hard to come by.” He continued, “If you’ve got a solid project it can get financed today, no doubt about it.”

On current lending, both Chapin and Thompson indicated optimism, particularly as vaccinations continue to reach millions of residents within seniors housing. Thompson said, “Lenders are learning what to ask when it comes to underwriting and due diligence. I see more lenders willing to dig in and do the due diligence than earlier in the pandemic. It’s early in the year so, from a practical standpoint, lending groups have loan-growth goals that they have to deal with.”

Some questions probed into the near future. Mendes, explaining his optimism, said, “a theme in the senior housing capital markets in 2020 and through to today is that in-place performance at the asset level is usually declining month-over-month. You engage a deal in September and, come December, the numbers look worse, which has caused ongoing stress in the transaction process. I believe what we’ll see later this year is just the opposite. The numbers are going to start looking better as the transaction process progresses. This trend, in my opinion, will be accelerated by the decline in construction starts, and also combined with the growth in the 80-plus demographic.” He pointed out that growth in that demographic from 2021 to 2023, “is projected to be twice what it was from 2017 to 2019.”

Mendes continued, saying, “from an equity perspective, dry powder in the United States for real estate in December 2020 was over $200 billion, that’s uninvested private equity, which is close to a record high.” He explained that, with so much liquidity in the market, “lenders can expect high quality sponsors, like Bridge for instance, with the ability to invest meaningful equity into transactions.”

Looking ahead, the panelists generally foresee a gradual return to pre-pandemic business practices and performance. They discussed the impact of numerous factors throughout 2021, including the regulatory impact on banks, the potential for improved occupancy, and the attractiveness of the sector to investors. On that point, Schmidt pointed out that big pre-COVID challenges, such as labor shortages and oversupply of new properties have eased. He said, “Operators will have to recognize, and I think we are, the new normal and not revert back to the old normal and continue to evolve. That creates the real opportunity. The owners and operators that do that really well will attract a lot of investment capital going forward.” The webinar portion of this NIC Leadership Huddle event is available, in its entirety, on NIC.org. Registration is now open for the upcoming February 24 Leadership Huddle, titled, “Is There an Investment Case for Skilled Nursing in the Intra-and Post-Pandemic World?” Spaces for the follow-up discussion group are limited, and are offered on a first-come, first-served basis

Executive Survey Insights | Wave 21: January 25 to February 7, 2021

NIC’s Executive Survey of operators in seniors housing and skilled nursing is designed to deliver transparency into market fundamentals in the seniors housing and care space as market conditions continue to change.

“Significant headway is being made to vaccinate residents and staff in seniors housing and care communities. According to 84 small, medium, and large seniors housing and skilled nursing operators from across the country—ranging in size from single-building operators to operators with hundreds of buildings across their portfolios of properties—considering all care segments, approximately 80% of residents and 50% of staff have received their first dose of the COVID-19 vaccine on average, and about 60% of residents and 45% of staff have received their second dose. While educating and motivating staff to be vaccinated continues to be cited as a challenge, the majority of organizations have not made the vaccine mandatory. Although one-quarter of respondents noted an increase in prospect interest specifically related to the availability of the vaccine, the survey data has yet to show an upward trend in occupancy. It will be interesting to see when the trend begins to reverse with greater penetration of the COVID-19 vaccine in the coming weeks and months.”

–Lana Peck, Senior Principal, NIC

NIC’sExecutive Surveyof operators in seniors housing and skilled nursing is designed to deliver transparency into market fundamentals in the seniors housing and care space as market conditions continue to change. This Wave 21 survey includes responses collected from January 25 to February 7, 2021, from owners and executives of84 small, medium, and largeseniors housing and skilled nursing operators from across the nation, representing hundreds of buildings and thousands of units across respondents’ portfolios of properties.

Detailed reports for each “wave” of the survey and a PDF of the report charts can be found on theNIC COVID-19 Resource Centerwebpage underExecutive Survey Insights.

Additionally, the full range of time series data for each wave of the survey by care segment for move-ins, move-outs, and occupancy rate changes can be found HERE.

Wave 21 Summary of Insights and Findings

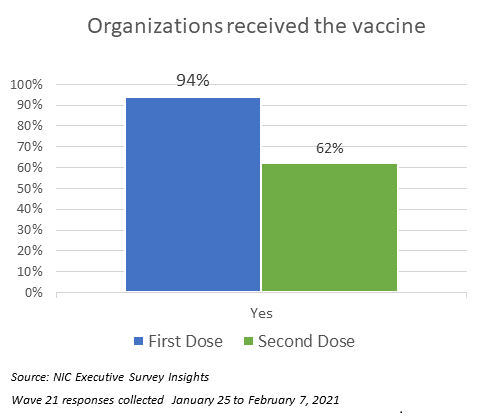

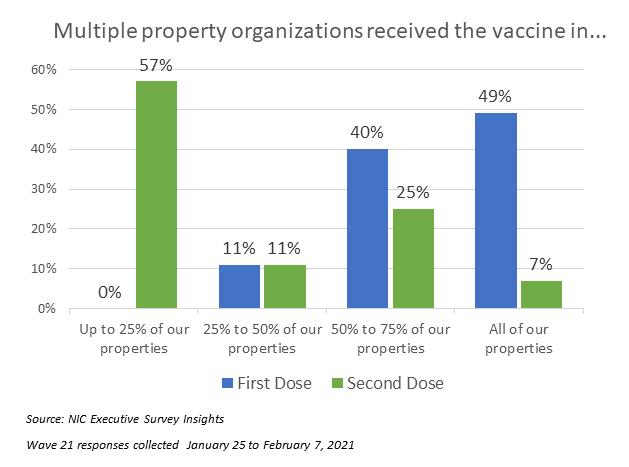

Most organizations that responded to the Wave 21 survey, which ended on February 7, had already finished their first COVID-19 vaccine clinics, and many, but not all, have started their second clinics. Nine out of ten have had their first clinic (94%), while two out of three (62%) have had their second clinic. Among those organizations that have received the second dose and have more than three properties in their portfolios, over half (57%) have received it in up to 25% of their properties, and one-third (32%) have received the second dose in 50% to 75% of their properties.

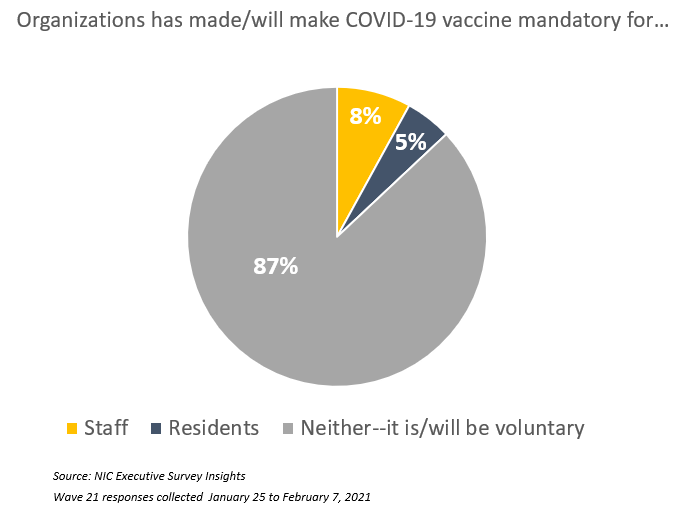

Four out of five organizations inWaves 20and 21 indicated that educating and motivating staff to take the vaccine was a challenge (the Wave 20 survey report detailed strategies by operators to encourage and improve vaccine acceptance; Wave 21 measures those strategies for change). The majority of organizations have not made the COVID-19 vaccine mandatory for residents and/or staff (87%). Whether or not the vaccine remains voluntary for most organizations will continue to be monitored in Wave 22 of the survey as anecdotal comments by some operators suggest that unless staff vaccination rates improve, mandatory vaccination may be considered.

According to Wave 21 survey respondents, approximately 80% of residents and 50% of staff of seniors housing and care properties—considering all care segments across their portfolios of properties—have received their first dose of the COVID-19 vaccine on average, and about 60% of residents and 45% of staff have received their second dose. This CDC reportoffers comparison dataregarding vaccine coverage among more than 11,000 skilled nursing facilities in their first clinic conducted during the first month of the CDC Pharmacy Partnership for Long-Term Care Program.

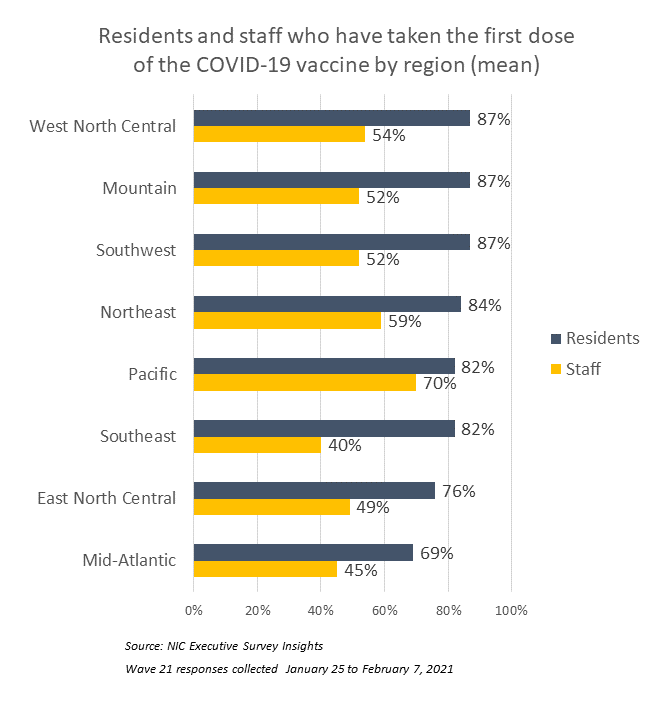

The chart below shows the average of survey respondents’ residents and staff that have taken the first dose of the COVID-19 vaccine, by region. The East North Central and Mid-Atlantic regions were the lowest for residents—averaging 76% and 69%, respectively. The Southeast and Mid-Atlantic regions were the lowest for staff—averaging 45% and 40%, respectively. It is important to note that vaccine distribution rates depend on a variety of factors including but not limited to supply and demand, acceptance, and vaccination administration logistics.

Vaccination administration logistics was a challenge for roughly 40% of organizations in Waves 20 and 21. Many operators indicated that their organizations have experienced varying levels of disorganization, confusion, and delays in terms of the pharmacy program in vaccinating residents. Some organizations mentioned that they are working to provide resources and information for their independent living residents on where they can get the vaccine on their own in some states, including Florida and California.

Many operators have been eagerly anticipating a boost in occupancy due to the COVID-19 vaccine availability. Although about one-quarter of organizations responding to the Wave 21 survey note an increase in prospect interest specifically related to the vaccine, most (67%) do not, suggesting other influential factors. For example, the share of organizations citing increased resident demand (86%) as a reason for acceleration in the pace of move-ins in the past 30-days is at the highest level since the Wave 12 survey. Additionally, respondents citing resident or family member concerns as a reason for acceleration in move-outs continues to trend at its lowest level (20%) due in part to operator innovations in infection mitigation and creative visitation protocols which have gained acceptance from many residents and families, quelling move-outs due to the virus. (Some organizations have branded programs to the marketplace highlighting their commitment to safety and health protocols).

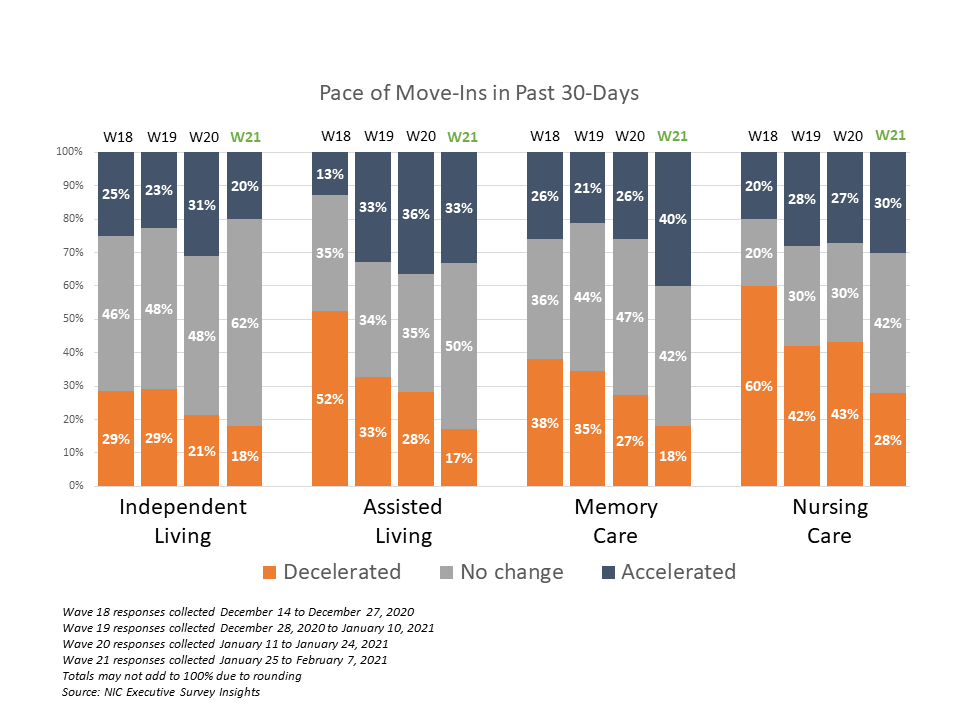

In Wave 21, the shares of organizations reporting acceleration in the pace of move-ins is higher than the portion of organizations reporting deceleration for each of the care segments. Furthermore, organizations reporting deceleration in the pace of move-ins has shrunk across each of the care segments over the past three waves of the survey.

While the independent living care segment saw the least change in the pace of move-ins, with 62% of organizations noting no change, more organizations with memory care units reported acceleration in the past 30 days (40%) than in eight prior waves of the survey (reflecting operators’ experiences in mid to late August).

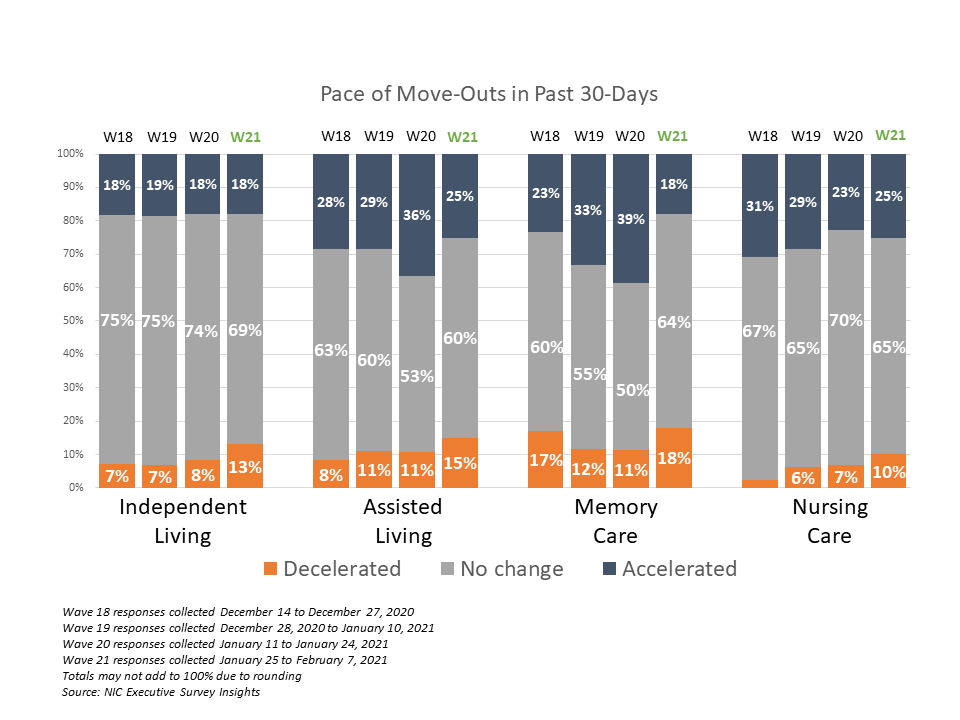

Substantially fewer respondents in Wave 21 noted that their organizations had a backlog of residents waiting to move in (15%)—lower than at any time since the question was first asked in late July, and down from approximately one-third of respondents in the prior survey. Possible reasons may include typical seasonality experienced during the winter months and fewer organizations offering rent concessions to support sales. In the Wave 21 survey, the fewest respondents reported offering rent concessions to attract new residents (45%) since mid to late August. Another possible reason may include less turnover of inventory. The pace of move-outs slowed in the Wave 21 survey. Between 75% and 82% of organizations noted no change or deceleration in the pace of move-outs in the past 30-days for each of the care segments.

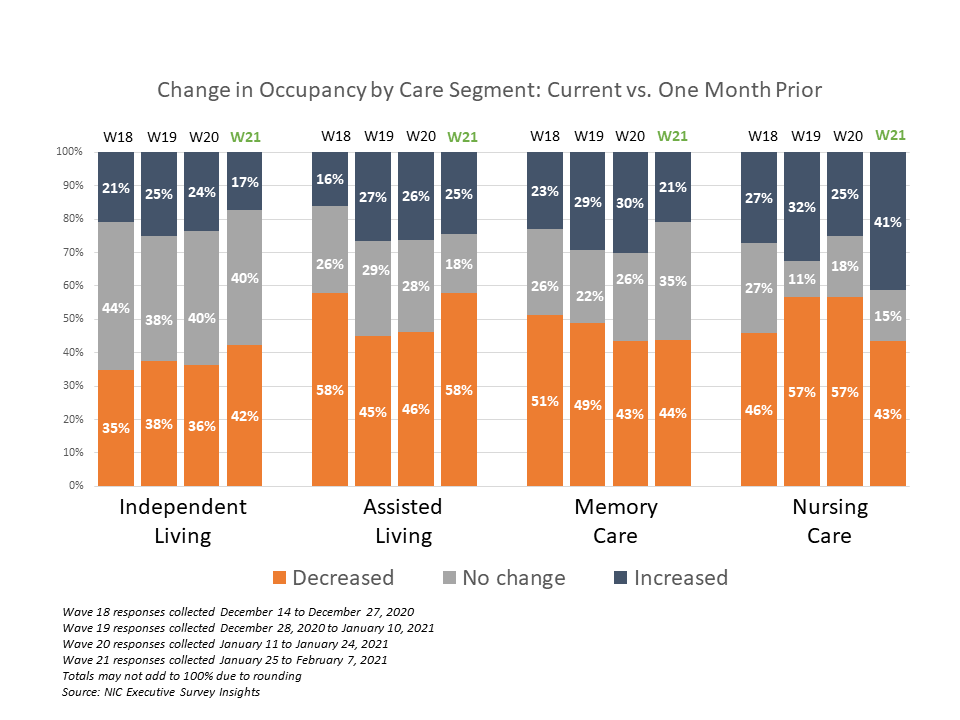

Reflecting operators experiences at the end of 2020, the Wave 21 survey data has yet to show an upward trend in occupancy. For each of the care segments, the shares of organizations reporting occupancy declines in the past 30-days (across their portfolios of properties) continued to outpace those reporting higher occupancy. It will be interesting to see if the data that has been trending this way since the Fall surge of the coronavirus begins to reverse with greater penetration of the COVID-19 vaccine in the coming weeks andmonths.

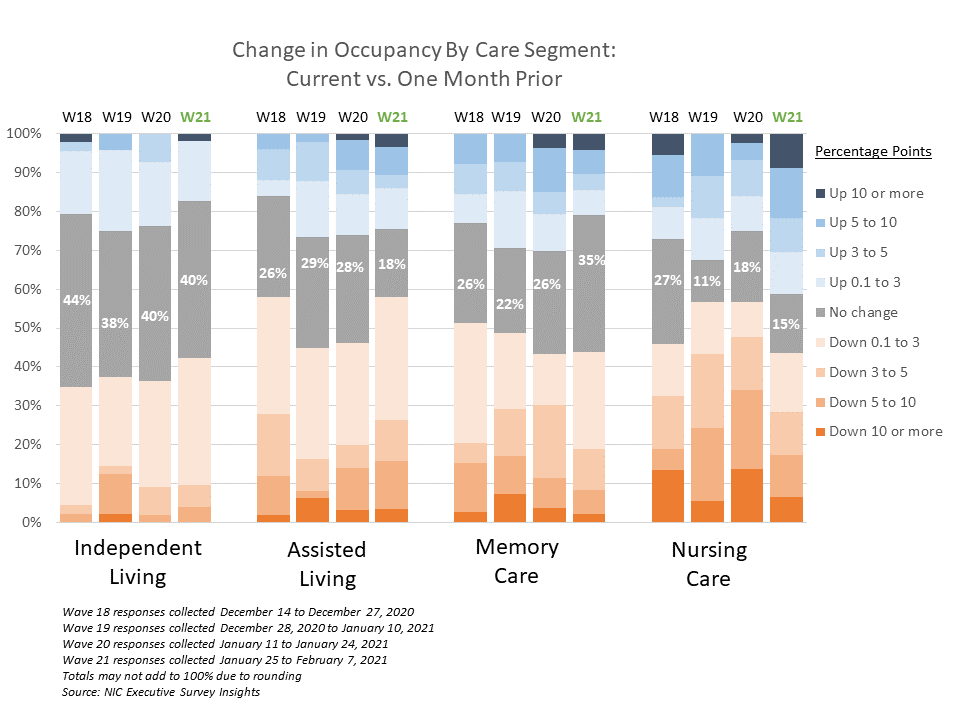

The chart above shows that in Wave 21, 41% of organizations with nursing care beds reported increasing occupancy rates. The chart below describes the degree of those occupancy rate changes and illustrates that more organizations with nursing care beds in Wave 21 reported stronger increases than in the prior three waves of the survey. (The blue and orange-hued stacked bars correspond to the solid bars in the chart above indicating the degree of change by the saturation of color.) In the Wave 21 survey, about one-third of respondents with nursing care beds (31%) reported occupancy increases of three percentage points or more. However, in the Wave 20 survey, fewer than one-fifth had reported the same (16%).

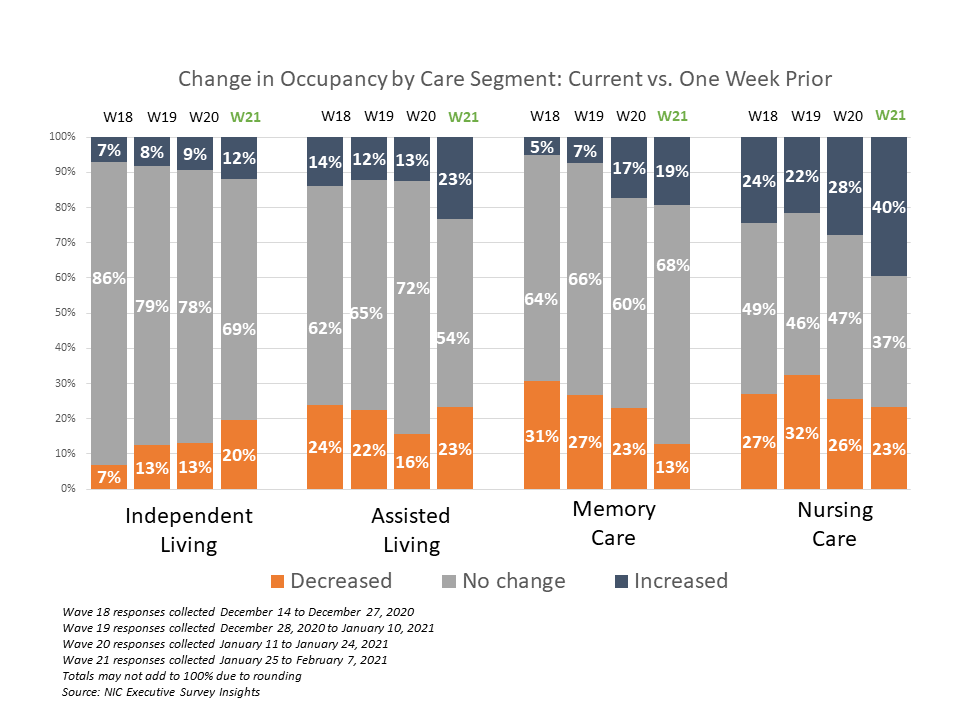

Similar to past surveys, differences in week-over-week occupancy rates typically result in little change. However, the assisted living and nursing care segments show higher shares of respondents reporting occupancy rate increases from one week prior in Wave 21 compared to Wave 20 (23% vs 13% and 40% vs. 28%, respectively).

Wave 21 Survey Demographics

Responses were collected between January 25 and February 7, 2021 from owners and executives of 84 seniors housing and skilled nursing operators from across the nation. Owner/operators with 1 to 10 properties comprise just over half of the sample (58%). Operators with 11 to 25 properties make up about one-quarter of the sample (26%), while operators with 26 properties or more make up 15% of the sample.

About one-half of respondents are exclusively for-profit providers (47%), two out of five (41%) are nonprofit providers, and 12% operate both for-profit and nonprofit seniors housing and care organizations.

Many respondents in the sample report operating combinations of property types. Across their entire portfolios of properties, 68% of the organizations operate seniors housing properties (IL, AL, MC), 36% operate nursing care properties, and 45% operate CCRCs (aka Life Plan Communities).

Owners and C-suite executives of seniors housing and care properties, we’re asking for your input!By demonstrating transparency, you can help build trust. The survey results and analysis are frequently referenced in media reports on the sector including inMcKnight’spublications,Mortgage Professional America Magazine,Senior Housing News,Multi-Housing News, and other industry-watching media outlets. The surveys’ findings have also been mentioned in stories byKaiser Health News, CNN, theWall Street Journal, and other major news outlets across the U.S.

The Wave 22 survey is available and takes 5-10 minutes to complete.If you are an owner or C-suite executive of seniors housing and care and have not received an email invitation to take the survey, please clickthis linkor send a message toinsight@nic.orgto be added to the email distribution list.

NIC wishes to thank survey respondents for their valuable input and continuing support for this effort to bring clarity and transparency into market fundamentals in the seniors housing and care space at a time where trends are continuing to change.

Skilled Nursing Occupancy Reached New Low In November 2020

NIC MAP® Data Service released its latest Skilled Nursing Monthly Report on February 4, 2021, which includes key monthly data points from January 2012 through November 2020.

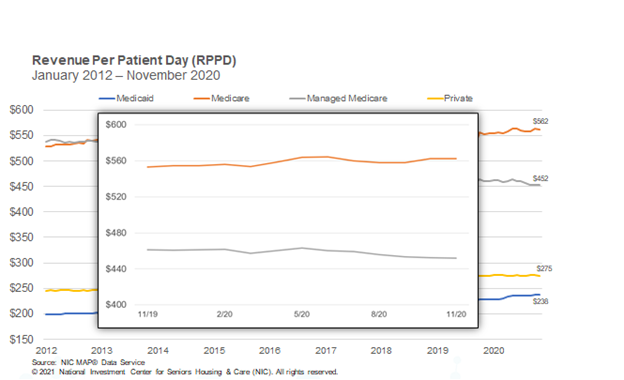

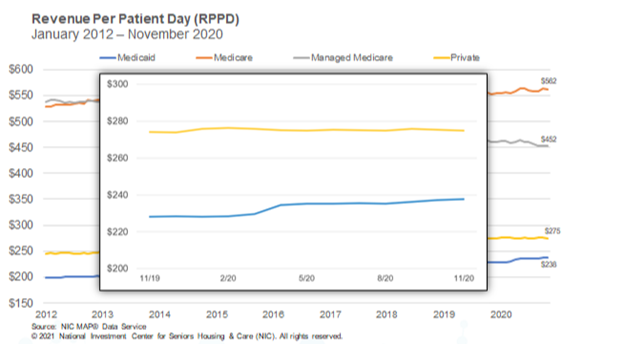

Medicaid Revenue Per Patient Day Up But Cost of Care Still a Concern.

NIC MAP® Data Service released its latest Skilled Nursing Monthly Report on February 4, 2021, which includes key monthly data points from January 2012 through November 2020.

Here are some key takeaways from the report:

Occupancy

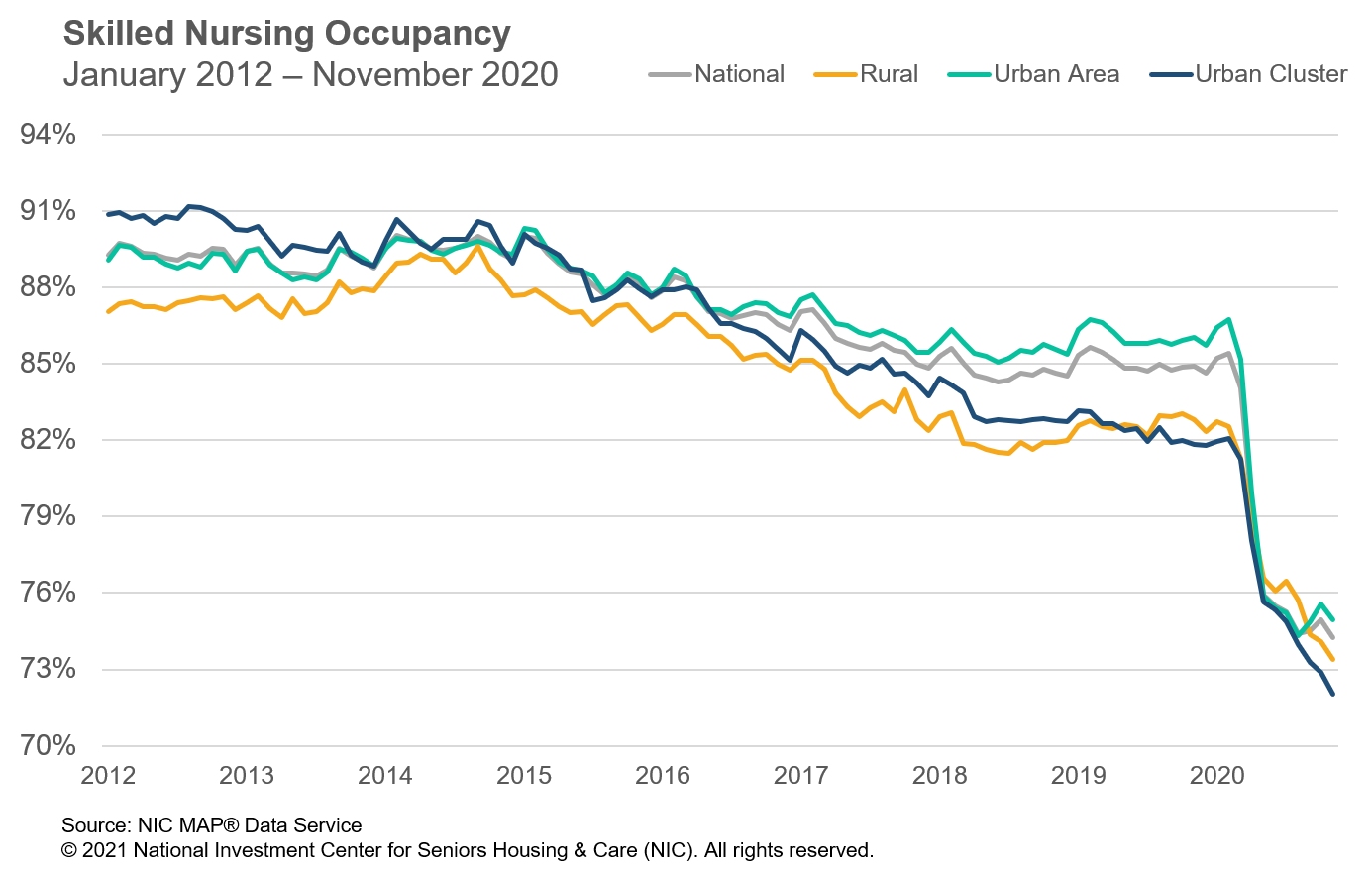

Occupancy continues to be challenged for skilled nursing properties, with the November 2020 occupancy rate falling to a new low of 74.2%. It was down 69 basis points from October (74.9%) and 11.2 percentage points from pre-pandemic levels in February 2020 (85.4%) and 10.7 percentage points from year-earlier levels. Since February 2020, COVID-19 has significantly impacted skilled nursing operations across the country due to high acuity levels of residents, pandemic-related deaths as well as fewer elective surgeries at hospitals which have resulted in less need for rehab services often provided by nursing care properties. As the country and the skilled nursing sector navigate through the Winter months and vaccine distributions, it is likely that occupancy will continue to face pressure.

Medicare

Medicare revenue per patient day (RPPD) was unchanged at $562 from October to November 2020. However, it is up by 1.6% since March. This increase is likely because of additional reimbursement by Medicare for COVID-19 positive patients requiring isolation, in addition to the temporary suspension of the 2.0% sequestration cuts by the Centers for Medicare and Medicaid Services (CMS). In addition, Medicare RPPD increased 1.7% compared to a year ago. Meanwhile, Medicare revenue mix increased 80 basis points from October to end November at 22.2%. It has increased 141 basis points since April.

Managed Medicare

Managed Medicare RPPD hit a time-series low (since 2012) as it decreased once again from the prior month. It ended November 2020 at $452. Early in the pandemic managed Medicare RPPD increased but has resumed the years-long trend of monthly declines. It is down 2.0% since November 2019 and has declined 16% ($86) since January 2012, Meanwhile, managed Medicare revenue mix decreased 36 basis points from October to November to 8.8%. However, it has declined 208 basis points since February, when it was 10.9% before the pandemic started.

Medicaid

The relatively large increases in Medicaid RPPD seen at the onset of the pandemic have slowed, especially after the 2.1% increase experienced in April. Early in the pandemic, initial increases in reimbursement from some states helped skilled nursing properties related to the number of COVD-19 cases at properties. In November, RPPD increased 0.2% from October, ending at $238. On a slightly longer time frame, Medicaid RPPD is up 4.2% from the prior year. However, even with this increase, the concern continues to be that current Medicaid RPPD does not cover the actual cost of care in most states.

To get more trends from the latest data you can download the Skilled Nursing Monthly Report here. There is no charge for this report.

The report provides aggregate data at the national level from a sampling of skilled nursing operators with multiple properties in the United States. NIC continues to grow its database of participating operators in order to provide data at localized levels in the future. Operators who are interested in participating can complete a participation form here. NIC maintains strict confidentiality of all data it receives.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. NIC's privacy policy can be viewed here. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.