NIC MAP Vision released its latest Skilled Nursing Monthly Report on March 30, 2023. The report includes key monthly data points from January 2012 through January 2023.

Here are some key takeaways from the report:

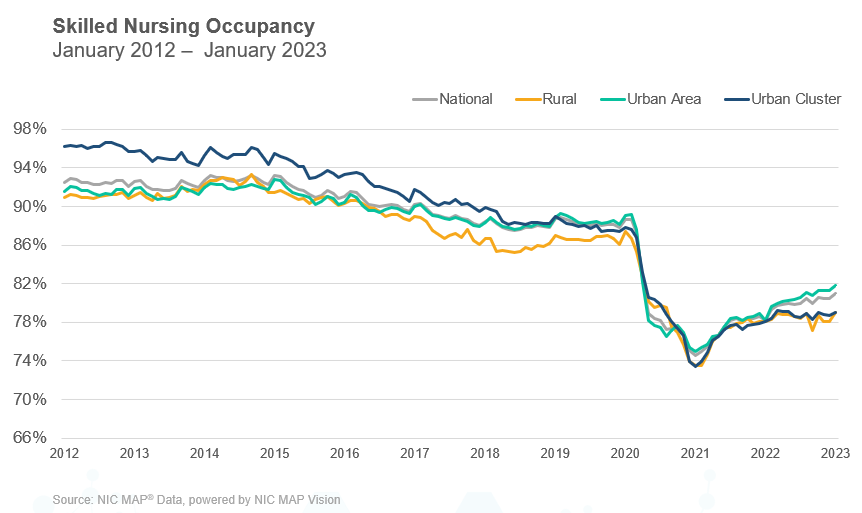

Occupancy

Skilled nursing occupancy started the year with a positive trend in January 2023. It increased 49 basis points from December to end the month at 81.0%. There was positive momentum in occupancy throughout 2022 and it is up 643 basis points since the low point (74.5%) reached in January 2021. Although occupancy was relatively flat from May 2022 through September 2022, it did increase 274 basis points from January 2022 to January 2023. The staffing crisis in the sector is still a significant burden on skilled nursing operators, especially as the acuity level of patients has increased along with the demand for nurses. As staffing, wage growth, and general inflation pressures persist, operations for many operators will be under pressure but the long-term demand for skilled nursing services is expected to grow over time.

Medicaid

Medicaid revenue mix was unchanged ending January at 49.8%. However, it is up 91 basis points from one year ago when it was 48.8% in January 2022. One element of the Medicaid revenue share of a property’s revenue is revenue per patient day (RPPD) and that increased 0.49% from December. It is up 2.79% since January 2022 and is now at $269, which is an all-time high.

Medicaid reimbursement has increased more than usual as many states embraced measures to increase reimbursement related to the number of COVID-19 cases throughout the pandemic, but many states have continued to increase reimbursement. Medicaid has increased 6.3% since February 2020. On the other hand, covering the cost of care for Medicaid patients is still a major concern as reimbursement does not cover the cost of care in many states. In addition, nursing home wage growth is elevated along with overall inflation, and staffing shortages are a significant challenge in many areas of the country.

Medicare

Medicare revenue per patient day (RPPD) decreased slightly from December 2022 to end January 2023 at $592. This was a decrease from $594 in December, which was its highest level since June 2020 when the federal government began implementing many initiatives to aid operators of properties for cases of COVID-19, including increases in Medicare fee-for-service reimbursements to help care for COVID-19 positive patients requiring additional care. Medicare RPPD is down slightly from one year ago in January 2022, which was when COVID-19 cases were elevated and RPPD was elevated as well. In addition, RPPD is up 3.0% since September 2022 which is likely due to the fiscal increase for 2022-2023. Meanwhile, Medicare revenue mix trended down in the month of January, decreasing 18 basis points from 23.3% to end the month at 23.1%. It is down 211 basis points compared to one year ago in January 2022. There was an elevated number of COVID-19 cases in January 2022 and the data suggests there was a significant uptick in the utilization of the 3-Day Rule waiver as COVID-19 cases increased last year. The 3-Day Rule waiver was implemented by Centers for Medicare and Medicaid Services (CMS) to eliminate the need to transfer positive COVID-19 patients back to the hospital to qualify for a Medicare paid skilled nursing stay, hence increasing the Medicare census at properties. As the cases decline, the Medicare revenue share declines, all else equal.

Managed Care

Managed Medicare revenue mix increased 85 basis points from December to end January at 11.2%. This is up 254 basis points from the pandemic low set in May 2020 of 8.7%, which was a time when elective surgeries were suspended and created fewer referrals from hospitals to skilled nursing properties. Meanwhile, Managed Medicare revenue per patient day (RPPD) increased from $467 to $468 in January. Compared to its year-earlier value of $474, it is down 1.3% and it is down $117 (20.0%) from January 2012. It continues to create pressure on operators’ revenue as managed Medicare enrollment continues to expand its reach and coverage around the country. However, some operators see an opportunity to capture patient volume with the growth of managed care. The persistent decline in managed Medicare revenue per patient day continues to result in an expanded reimbursement differential between Medicare fee-for-service and managed Medicare. Medicare fee-for-service RPPD ended January 2023 at $592, representing a $124 difference. For context, the differential one year ago was $119 and two years ago it was $101.

To get more trends from the latest data you can download the Skilled Nursing Monthly Report. There is no charge for this report.

The report provides aggregate data at the national level from a sampling of skilled nursing operators with multiple properties in the United States. NIC continues to grow its database of participating operators to provide data at localized levels in the future. Operators who are interested in participating can complete a participation form on our website. NIC and NIC MAP Vision maintain strict confidentiality of all data received.