A Note From Brian Jurutka

NIC announced last month that it acquired Raleigh, NC-based VisionLTC to create the seniors housing industry’s leading market analytics platform serving many of the industry’s largest and most advanced stakeholders. Together, these organizations are forming a new company called NIC MAP Vision.

NIC announced last month that it acquired Raleigh, NC-based VisionLTC to create the seniors housing industry’s leading market analytics platform serving many of the industry’s largest and most advanced stakeholders. Together, these organizations are forming a new company called NIC MAP Vision.

The acquisition strengthens NIC’s ability to further fulfill its mission. NIC leaders have admired the agility, insights, and complementary data expertise of VisionLTC, which also aligned with NIC MAP® Data Service’s (NIC MAP) strategic plan to create the data and analytics champion that our industry needs.

The combined NIC MAP and VisionLTC staff members that make up NIC MAP Vision have the experience and expertise to provide a comprehensive data solution that industry investors, owners, and operators can rely on. NIC MAP Vision will integrate NIC MAP supply data with VisionLTC demand and healthcare data sets to provide for a powerful platform to identify risks and opportunities. VisionLTC’s chief executive officer Arick Morton leads NIC MAP Vision.

As Kurt Read, managing director at RSF Partners and chair of NIC’s Board of Directors, said, “Bringing NIC MAP and VisionLTC together will result in the best possible business intelligence for senior housing and care investors, owners, and operators.” The new company will help stakeholders understand, for example, the impact that living in a senior housing property or community has on Medicare spending; health and healthcare outcomes; when a market becomes saturated; and ways to successfully increase access and choice for people in the underserved “middle-income-market” for senior housing and care.

As the COVID-19 pandemic has made clear, investors, owners, and operators need a holistic approach to data to understand market dynamics, including health and well-being metrics. The impending influx of baby boomers into multifamily housing and senior living options in the years ahead makes bringing together senior housing data addressing supply, demand, and healthcare even more relevant and essential for the ultimate benefit of America’s seniors.

NIC remains committed to enhancing data, analytics, and connections that enable access and choice for older adults through a continued investment in must-attend events, networking opportunities, research, and thought leadership. NIC MAP Vision will provide NIC use of its data to continue and expand NIC’s analytics and thought leadership.

As the industry navigates through this disruptive time, we are fortunate to work with partners who appreciate that transparency is needed now more than ever. Helping decision makers solve the industry’s biggest challenges calls for a more robust spectrum of data, and we believe that through NIC MAP Vision, that call will be answered.

Sincerely,

Brian Jurutka

NIC President & CEO

Innovative Technology Curbs Loneliness, Delivers Peace of Mind: A Conversation with Connected Living’s Sarah Hoit

A year into the pandemic, and the world has changed. Just ask Sarah Hoit, CEO at Connected Living, a leading technology platform that enables communication and connection for today’s aging adult communities. Her company has grown quickly during a difficult time of physical isolation by connecting residents virtually with staff, family, and friends.

A year into the pandemic, and the world has changed. Just ask Sarah Hoit, CEO at Connected Living, a leading technology platform that enables communication and connection for today’s aging adult communities. Her company has grown quickly during a difficult time of physical isolation by connecting residents virtually with staff, family, and friends.

NIC Chief Economist Beth Mace recently talked with Hoit about her company and its acquisition by Omega Healthcare Investors—a move that promises to boost even faster growth. They discussed technology’s role to connect everyone for an enhanced senior living experience that’s definitely here to stay. Here is a recap of their conversation.

Mace: Can you tell us about the origins of Connected Living?

Hoit: I’m a social entrepreneur. I like to do things that haven’t been done before that can make an impact. I was facing a personal situation, as was my partner, who had aging grandparents in home care and senior living. There was no window into their situations. We had no way to communicate. We felt disconnected. Every family member’s desire is to be engaged with their elders and give them a voice. My business partner, Chris McWade, whom sadly we lost to cancer about five years ago, and I saw that no one had successfully connected an aging population. So, why not try? We founded the company in 2007 and were up and running 18 months later.

Mace: How big is Connected Living?

Hoit: We are nationwide in more than 300 communities. We expect to double the number of communities we serve this year. Our team is a fairly small group of about 30 full-time and some part-time people. Half are technologists, and the others are client service representatives. We have a seven-day-a-week Connected Living call center to provide customer services to residents, staff, and families.

Mace: Why did you pick Connected Living as your company name?

Hoit: We’re trying to combat ageism. When I first decided to leave my job to start a new company, I looked at the names of other products, and they didn’t sound fun. They seemed to stereotype older folks as sick and frail. Our name is purposeful. It’s about being connected and living. So, we are Connected Living.

Mace: What are the key elements of your platform?

Hoit: At the center of the Connected Living ecosystem is an enterprise content management system, a master brain. An administrative dashboard provides an easy link to all elements of our ecosystem. It includes our mobile app; in-room and Apple TV; smart home and voice technology; a resident network; programming; digital signage; Temi, the personal robot; and printed calendars and newsletters. Communities can pick the elements they want.

Hoit: At the center of the Connected Living ecosystem is an enterprise content management system, a master brain. An administrative dashboard provides an easy link to all elements of our ecosystem. It includes our mobile app; in-room and Apple TV; smart home and voice technology; a resident network; programming; digital signage; Temi, the personal robot; and printed calendars and newsletters. Communities can pick the elements they want.

Mace: The mission of Connected Living has been to provide innovative technology solutions and services that inspire an aging population to connect, contribute, and live each day to its fullest. How does your partnership with Omega Healthcare Investors better enable you to accomplish that mission?

Hoit: It’s so exciting. We’ve been very selective about our partners. We wanted to find a group that had a similar outlook on the market opportunity. From the time Chris and I started the company, we never thought it was just going to be us. If you can find the right partners, you can make a bigger impact. It’s much easier than doing it alone. The pandemic brought attention to the crisis of loneliness among the aging. Omega understands, from a property perspective, that we can do tremendous good. A virtual connection is no longer just nice to have. It’s an essential, powerful service that provides programming and keeps residents and their families connected. The staff also needs modern tools to operate communities. Our technology was already in some of Omega’s beautiful Maplewood properties. I sat down with Taylor Pickett, CEO at Omega, and he said he thought we could make a big impact together. And that’s what it’s about for me. I’m an unusual CEO. I believe in the double bottom line that not only measures financial performance but also social impact. We have found the right partner, at the right time.

Mace: What’s the relationship with Omega?

Hoit: We are a wholly owned subsidiary of Omega, but we are based in Boston. I am CEO of Connected Living and also on the Omega management team. Omega’s operators will be introduced to our service, though it won’t be mandatory. Our marketplace is every building out there, not just Omega buildings. Our aspirations for the next few years are also to expand internationally, our technology is enabled to do so. We were already looking to expand internationally when the pandemic hit, and we are starting to revisit that. Our initial focus would likely be in the UK, where Omega already has a global portfolio with 100 UK properties and growing.

Mace: What impact has the COVID-19 pandemic had on Connected Living? Has it shifted how any of your products and services are typically used?

Hoit: The industry has been in turmoil. At first, people didn’t know what was happening. Everyone hit pause. Before last year, we knew isolation was a big issue for seniors. But the pandemic created a new reality that has accelerated the need to find new ways to connect. In the last couple of months, I feel as if the cloud has lifted. People have settled in, vaccinations are here. I think innovation has quickly propelled the senior living industry forward by five years overnight. Everyone is saying it’s a new day and we have to address the new reality.

Mace: Human connection and engagement have always been key elements of effective resident care. With the COVID-19 pandemic limiting group activities and the colder weather keeping more residents indoors, what strategies are being employed to maintain a sense of connectedness?

Hoit: One of the big advantages of our business is that we have an agile in-house development team. With Connected Living, we never think we’re finished. We conduct “tech sprints” where our team focuses on a specific product for two weeks. We release updates every month. The first few years of the company, I was outsourcing development and not getting exactly what I wanted. Now we have these amazing people in-house, and they deliver ahead of schedule.

We’ve deployed a variety of strategies to keep residents engaged. We developed an Apple TV app. We have a YouTube channel where the executive or activity director can provide live announcements, and residents can access other content. We’re like the Peloton of senior living, a hub for all the great content we can find from Namaste Yoga to Coro Music. We also have our own content through our Connected Living University with a robust curriculum and group discussions.

Mace: Connected Living’s technology powers the personal robot, Temi, which can assist staff with day-to-day operations and connect residents with family members and physicians, among other things. Personal robots may have historically been viewed as a feature of modern, luxury senior living. Has the COVID-19 public health emergency broadened the use of personal robots?

Hoit: We learned about Temi the robot just before the pandemic. I had been looking at robots for a while, and they’re neat. But they can cost as much as $75,000 and often don’t connect with anything else in the building. Temi is less than $4,000, weighs 25 pounds, and is 4 feet tall. Temi rolls right out of the box and connects to everything in the building. The most amazing thing is that Temi’s face is the person you’re talking to whether it’s your grandchild or doctor. Families use Temi for birthday parties and as a companion. It’s a way to enhance human connections. Temi assists the staff with day-to-day operations.

Hoit: We learned about Temi the robot just before the pandemic. I had been looking at robots for a while, and they’re neat. But they can cost as much as $75,000 and often don’t connect with anything else in the building. Temi is less than $4,000, weighs 25 pounds, and is 4 feet tall. Temi rolls right out of the box and connects to everything in the building. The most amazing thing is that Temi’s face is the person you’re talking to whether it’s your grandchild or doctor. Families use Temi for birthday parties and as a companion. It’s a way to enhance human connections. Temi assists the staff with day-to-day operations.

Mace: What makes Connected Living different from other organizations that offer senior living entertainment platforms to residents?

Hoit: Often in senior living, the information systems don’t talk to each other. Staff has to input information to several platforms. Connected Living has one point of entry that integrates different vendors. Already have a Sodexo menu? We can integrate that. Our content management system can link to virtually any data source.

Mace: Connected Living implemented a special Connection Accelerator package to allow seniors housing and care communities to get equipped to better provide connection and engagement ahead of the 2020 holidays. Was that program a success for Connected Living? Were there any surprises?

Hoit: We put that package together to help communities get connected at a critical time, and that’s one reason why we have so many new launches. Often when people think of technology, they think of something that’s complex and expensive. But we can start with our app and a digital sign. Every building has a monitor or screen to display our digital sign. Through our accelerated offering, we can provide a media stick for $300. Just download the app and we can be connected in a couple weeks. It’s simple. When you walk into a building, the signage tells people what’s happening—birthdays, activities, menus, everything. The sign is gorgeous and shows up on the TVs in the apartments too. Between the mobile app and the signage, everything can be accessed.

We can add content and other capabilities as we go along. But a community can start tomorrow and be connected with an elegant system that families and residents will want to use.

This program was a success for the operators who took up this offer and for their residents; and this was not a surprise to us because operators are really understanding the importance of enhanced resident interaction on both clinical outcomes and the ability to differentiate your facility from the competition. Given the success of this simple and easy entry point for operators into a connected platform, we plan to continue offering it through the duration of the pandemic.

Mace: Does Connected Living offer products and services that are specifically aimed towards the various care segments of seniors housing and care – independent living, assisted living, and skilled nursing? Are there specific products or services that are focused on the population that resides in memory care?

Hoit: A full suite of products is available for each level of living. People in independent living are pretty tech savvy and expect a community to offer the latest ways to connect. Some residents will primarily use the technology to connect with family and friends via video. Others will use it to set up their daily schedule, order their food for the day, listen to engagement content (music, yoga, meditation, etc.), share photos with grandchildren, or enhance their cognitive function through a carefully curated menu of games. In the higher acuity or memory care settings where residents may be less able to engage directly with the technology, family members can use the technology to keep up to date on the daily schedule of their loved ones and be involved in their lives, even if they live far away.

Our systems can deliver multiple points of contact to share information, depending on the individual’s needs. It’s an important asset for the staff too. They can learn about the residents and who they are. With a little information, you can completely change the dynamics of the interactions between the staff and residents. And of course, adult children making the decision to place mom or dad in assisted living or memory care have similar expectations. They are not going to move mom and dad if there’s no window into the place.

Mace: Do you conduct research on memory care and what works?

Hoit: I serve on the board of an Alzheimer’s group. And our chief purpose officer was a dementia trainer. Memory care is a real passion of ours. My family has personal experience with the disease. It’s not a disease where one size fits all. Sometimes a patient can take part in all we offer, while others may find comfort in something simple like talking to Alexa.

Mace: Seniors housing and care operators have, perhaps by necessity, embraced new technologies that allow residents to connect and engage with others virtually. In your experience, how have residents themselves received these new technologies?

Hoit: If you ask older people if they want a computer, they might say, “No.” But if you ask them if they want to see their grandkids, they say, “Yes.” It’s all in the approach. Never count a senior out. Just ask the right questions. The thing they care about most is their family and friends. Give them options. Some might think Temi is fun. Some people like social media, while others don’t. Our app offers families private communications, which can be especially useful for those who are intimidated by social media.

Mace: Is there anything else you would like our readers to know?

Hoit: Our partnerships with communities are about impact. This is an important moment in time. We have been prepping for this for a decade, waiting for the chance to do maximum good. And the time is here. People need to take a breath. Our solution is simple. We can get everyone connected and build from there. With a small investment, owners worried about occupancies can engage residents and address what families worry about most: having a window into the community to provide peace of mind.

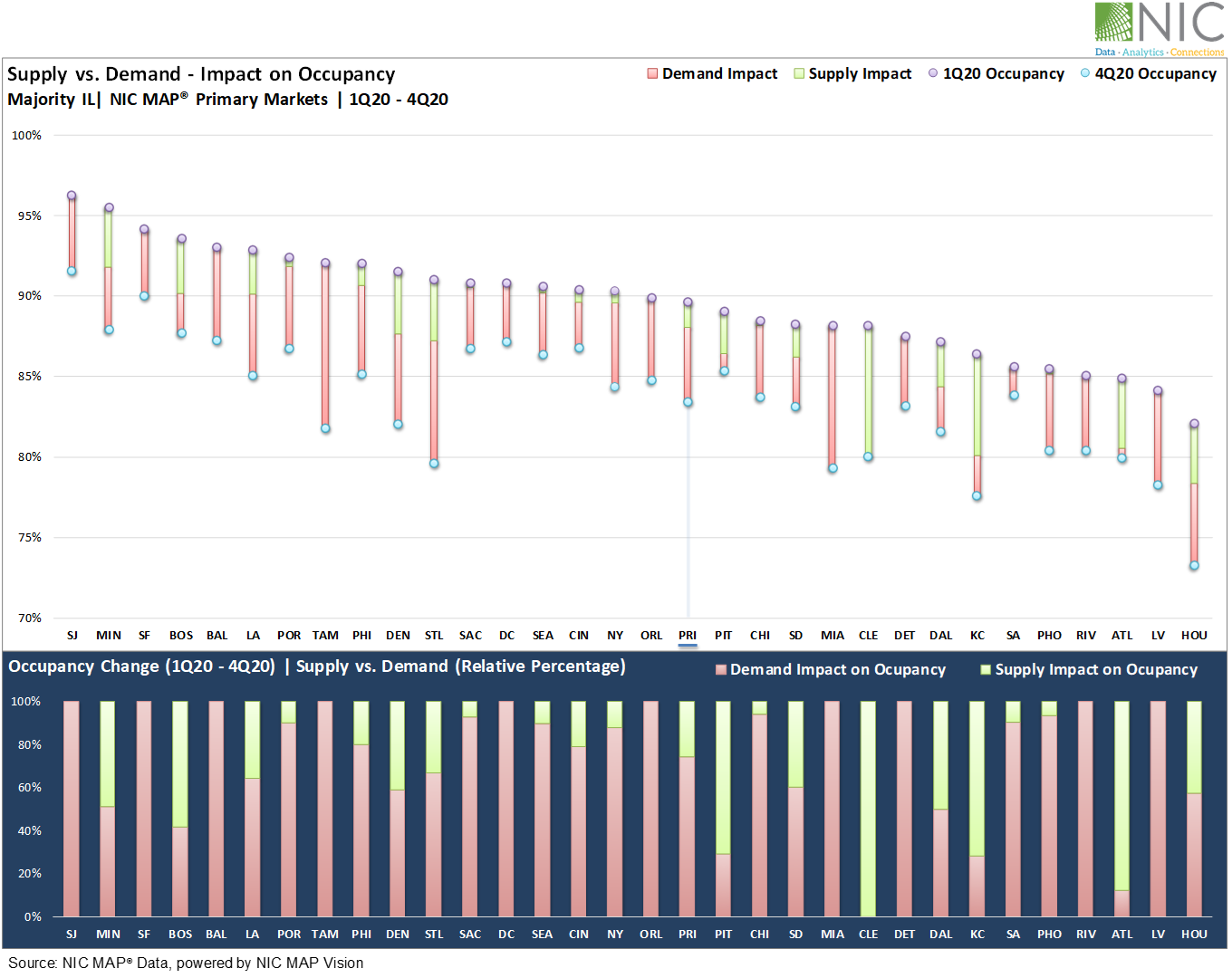

New Supply Accounted for One-Fourth of the Occupancy Drop in Independent Living Properties During the Pandemic

By Omar Zahraoui, Data Analyst, NIC

It has been a year since the pandemic first unfolded in the U.S. and began to influence the seniors housing and care industry, impacting disproportionately the nation’s most vulnerable elderly population and causing major disruptions with unprecedented downward pressure on occupancy levels, move-ins, and NOI.

It has been a year since the pandemic first unfolded in the U.S. and began to influence the seniors housing and care industry, impacting disproportionately the nation’s most vulnerable elderly population and causing major disruptions with unprecedented downward pressure on occupancy levels, move-ins, and NOI.

The pandemic largely is to blame for this past year’s drastic occupancy drops. However, some metropolitan markets saw a significant decline due to negative absorption (as a result of especially weak demand) compounded by new supply or high growth in inventory. In other words, the supply part of the equation has amplified the impact of the pandemic on occupancy levels due to weak demand and slowing rates of move-ins.

In this article, we examine, measure, and quantify the impact of the supply- and demand-sides of the occupancy equation for occupancy declines since the first quarter of 2020. The exhibit below provides a zoomed-in view of the said impact for majority independent living properties across NIC MAP® Primary Markets since the pandemic began in the first quarter of 2020. A similar analysis has been done for assisted living, nursing care, and seniors housing (the combination of assisted living and independent living).

For context, the occupancy rate for majority independent living properties across the Primary Markets fell 6.2 percentage points (pps) to a new low of 83.5% in the fourth quarter of 2020 from the pre-pandemic level of 89.6% in the first quarter of 2020. About one-fourth of the occupancy drop can be explained by new supply (1.6 pps) and 74% is due to declining demand (equivalent to 4.6 pps). Notably, it only took three quarters (nine months) for the Primary Markets to lose or give back all of the units occupied during the eleven quarters prior to the pandemic. Said another way, it only took three quarters (nine months) of time to reverse eleven quarters (2.75 years) of positive demand within the Primary Markets. This clearly shows the consequential impact the pandemic has had on demand and the independent living market’s performance.

Drilling deeper into metropolitan markets, Cleveland’s occupancy fell 8.1 percentage points (pps) from 88.2% in first quarter 2020 to 80.1% in fourth quarter 2020. Interestingly, the 8.1 pps drop in occupancy is explained by strong growth in inventory, suggesting that supply including new property openings, property expansions, and properties in lease-up put the majority of downward pressure on occupancy rates. Net absorption was negative in the second and third quarters, but that was offset by strong demand in the fourth quarter of 2020.

Kansas City also experienced a drop in occupancy that also was largely due to new supply entering the market; it had negative demand as well, but supply was a larger issue.

On the other hand, Detroit is a market that experienced a drop in occupancy largely due to demand; inventory did not expand between the first quarter of 2020 and the fourth quarter of 2020. Other markets that lost occupancy largely due to demand effects in majority independent living properties include San Jose, San Francisco, Baltimore, Washington D.C., Orlando, Miami, San Antonio, Riverside and Las Vegas—none of these markets experienced significant inventory growth.

Notably, although San Jose continued to rank first in independent living occupancy among the Primary Markets at 91.6% in the fourth quarter, its occupancy rate still fell 4.7 percentage points over the course of the pandemic. Its drop in occupancy was due to negative demand. Moreover, San Jose experienced a relatively higher decrease in demand compared to some of the markets at the bottom of the pack in the occupancy rankings, e.g., Atlanta and Kansas City where the drop in occupancy is due in significant part to new supply.

Similarly, the drop in occupancy rates for total seniors housing and majority assisted living properties has been the result of both supply and demand pressures.

While this analysis captures NIC MAP quarterly data as of the fourth quarter of 2020, the NIC Intra-Quarterly Snapshot report featuring NIC MAP Data, powered by NIC MAP Vision, showed that occupancy continued to be pressured lower through the February 2021 reporting period, but the rate of decline slowed as confirmed COVID-19 cases fell and vaccinations rose. There are promising signs for the outlook for seniors housing properties, in particular, to turn positive and remain bullish despite the ongoing challenges of the pandemic.

There is no doubt that demand will likely pick up for seniors housing properties when restrictions on move-ins ease and efforts to enlighten potential residents and families about the value proposition of seniors housing and to build back confidence gain traction.

Ongoing research by NIC Analytics suggests that some seniors housing markets will likely return to pre-pandemic demand sooner than others. However, the rebound may take a lot longer for some markets than others and will be influenced by both supply and demand factors. Will those markets with fewer developments bounce back faster than the ones where supply is high? And what will the recovery/rebound from the pandemic look like for the seniors housing industry? Further analysis on this topic is forthcoming.

To keep abreast of future analyses, be sure to regularly check NIC’s blog, NIC Notes. To learn more about NIC MAP Vision and how it can help your organization, please email sales@nicmapvision.com.

Capital Markets in 2021: What Lies Ahead?

By Bill Kauffman, Senior Principal, NIC

As the seniors housing and care sector progresses through 2021, some cautious optimism is palpable as the vaccine rollout ramps up throughout the country. That said, there are still many pressure points apparent such as low occupancy rates, rising insurance costs, and labor shortages. Uncertainty about the pandemic’s path and its impact on seniors housing and nursing care has also affected investment attitudes, transaction activity, capital markets broadly, and the lending environment. This article reviews these latter impacts by examining recent trends and conditions.

As the seniors housing and care sector progresses through 2021, some cautious optimism is palpable as the vaccine rollout ramps up throughout the country. That said, there are still many pressure points apparent such as low occupancy rates, rising insurance costs, and labor shortages. Uncertainty about the pandemic’s path and its impact on seniors housing and nursing care has also affected investment attitudes, transaction activity, capital markets broadly, and the lending environment. This article reviews these latter impacts by examining recent trends and conditions.

Underwriting Standards. Generally, many underwriting changes caused by the pandemic are still in place, but lending requirements should continue to “normalize” as vaccinations improve the seniors housing operating environment in the coming months. One change that may remain in underwriting standards, however, is gaining better understanding of the upstream and downstream aspects of operator partners. Lenders and other capital providers may now spend more time underwriting other parts of the healthcare system when thinking through a deal. This would include, for example, understanding the hospital referral patterns in a market, as well as an assessment of the strength of a particular health system around a property or portfolio of properties.

It’s likely that seniors housing lenders will be increasingly active and confident, but the COVID-19 pandemic will continue to impact the issuance of debt. For example, lenders are likely to continue to focus more on debt service coverage ratios than loan-to-value ratios. This is because values have typically not fallen as much as the net operating income at properties thereby decreasing the debt service coverage ratios more significantly. Regarding construction financing, a critical pandemic-related impact has been recourse. Lenders are requiring more recourse, and non-recourse debt is significantly harder to obtain, even for strong sponsors/borrowers. Overall, construction financing is still relatively restrictive with most originations coming from regional banks.

Lending Activity. Conventional bank lending has opened up considerably as of late, but it is not comparable across all banks. Banks with experienced staff and a long-term presence in the seniors housing market are making the first moves, and they are using the power of data to do so. Compared to earlier in the pandemic, lenders have gotten more comfortable with what the downside is to occupancy and have learned what to ask when it comes to underwriting and due diligence. Some finance companies may loosen standards to take advantage of market share, but more conservative banks are still cautious, certainly less cautious than at the onset of the pandemic, but still cautious, nonetheless.

There is also the reality that the volume of distressed properties may increase. Somewhat surprisingly to many is that this has not yet occurred largely due to the forbearance agreements and loan modifications and debt extensions on the part of banks. Bank reserves set aside to account for troubled loans have largely not materialized, and delinquencies and losses have been not yet mounted. That said, this will not last forever, and there will likely be some distressed activity in the coming months. Or possibly, cash flow will improve as the market recovers for those that currently are not able to service debt.

Will Transactions Activity Increase in 2021? Not surprisingly, transactions volumes and deal activity declined in 2020 because of the pandemic. Many buyers stood on the sidelines, while others elected not to sell and waited out the pandemic for a higher price, especially if they had intended on selling before the pandemic started. In addition, financing was challenging even if the seller and buyer were motivated.

Total seniors housing and care closed transaction volume for 2020 was only $8.5 billion, which was down 50% from the 2019 total of $17.1 billion. Both seniors housing and nursing care (skilled nursing) were, with no surprise, down significantly in volume. Seniors housing volume declined 52%, closing $5.7 billion of the total volume, and nursing care declined 44%, closing the remaining $2.8 billion of the total for 2020. However, after minimal closings in the second quarter of 2020 as the sector was in the beginning of the pandemic, activity began to increase slowly. As an example, seniors housing and nursing care (skilled nursing) closed $628 million and $421 million worth of transactions, respectively, in the second quarter but both closed over $1 billion to finish out the year in the fourth quarter.

Many expect that transaction activity will increase as 2021 progresses and capital providers, including debt and equity capital, become increasingly competitive for deal flow, and as investors need to place allocated capital into the sector, the so called “dry powder.” One of the main topics of discussion has been distressed properties and if that will become a larger portion of transaction activity as banks grow impatient in the event that occupancy does not bounce back in the coming months. That remains to be seen but does warrant watching as the sector starts to heal from the pandemic.

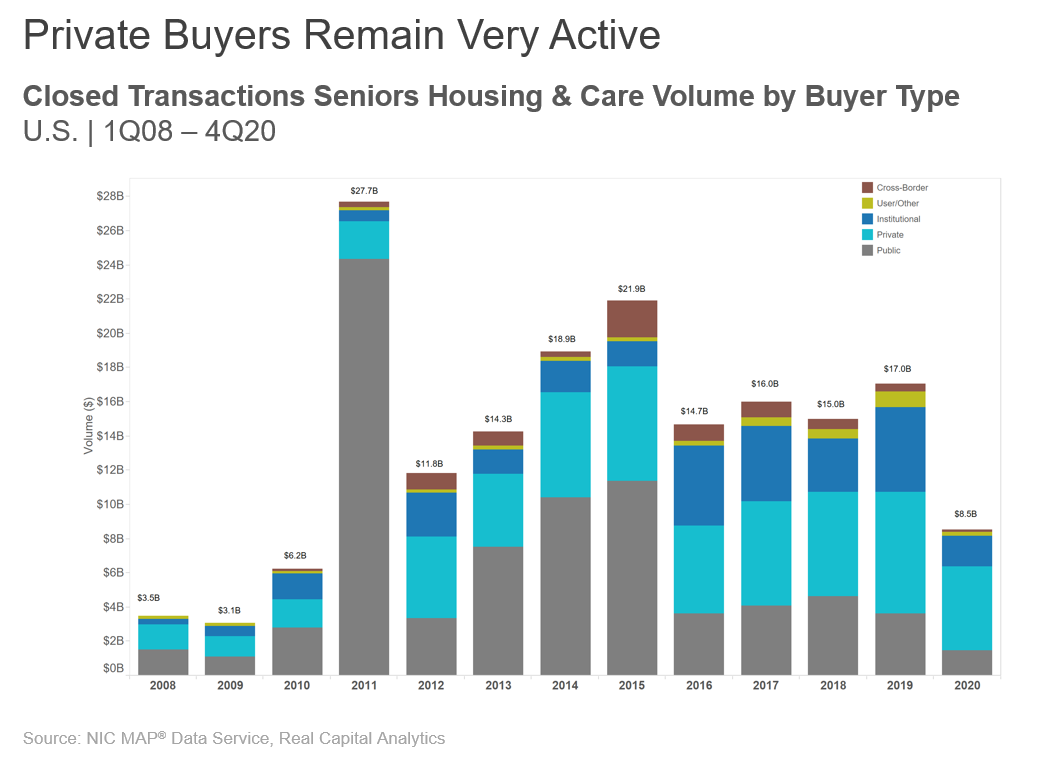

The Buyers. As noted previously, transaction activity has been muted, therefore, buyer activity in the sector remains low and decreased significantly between 2019 and 2020 due to the pandemic.

The bar chart below depicts transaction volume by buyer type, annually through 2020. The public buyer type is just that, any publicly traded company. The private buyer type is any company that is not publicly traded. For example, a private REIT or single owner or partnership, family offices, etc. The institutional buyer type is usually the equity funds that manage pension money or other types of institutional money. Cross-border represents any buyers from outside the United States.

Although activity in 2020 was low compared to 2019, one buyer that has been relatively steady is the private buyer. Private buyers were responsible for $4.9 billion in closed transaction activity in 2020, which made it the only buyer type to average $1 billion in activity each quarter in 2020. Private buyers ended the year on a strong note by closing $1.6 billion in the fourth quarter, which helped propel private buyers to represent over half of the closed dollar volume for 2020 at 58%. There is still much interest from investors, but most of that is coming from the smaller private buyer types, hence smaller deals. This interest is expected to continue as the sector navigates 2021.

In terms of the institutional buyers and the public buyers, which historically represent larger transactions, both registered under $2 billion in 2020. Institutional buyers and public buyers closed dollar volume for 2020 was $1.8 billion and $1.4 billion, respectively, which represented a decline of over 60% for both. It is possible that these buyers will increase acquisition activity in 2021, especially the institutional buyers if more distressed opportunities become available. The distressed activity could increase if banks become impatient with delays in debt service and/or occupancy takes longer than expected to bounce back.

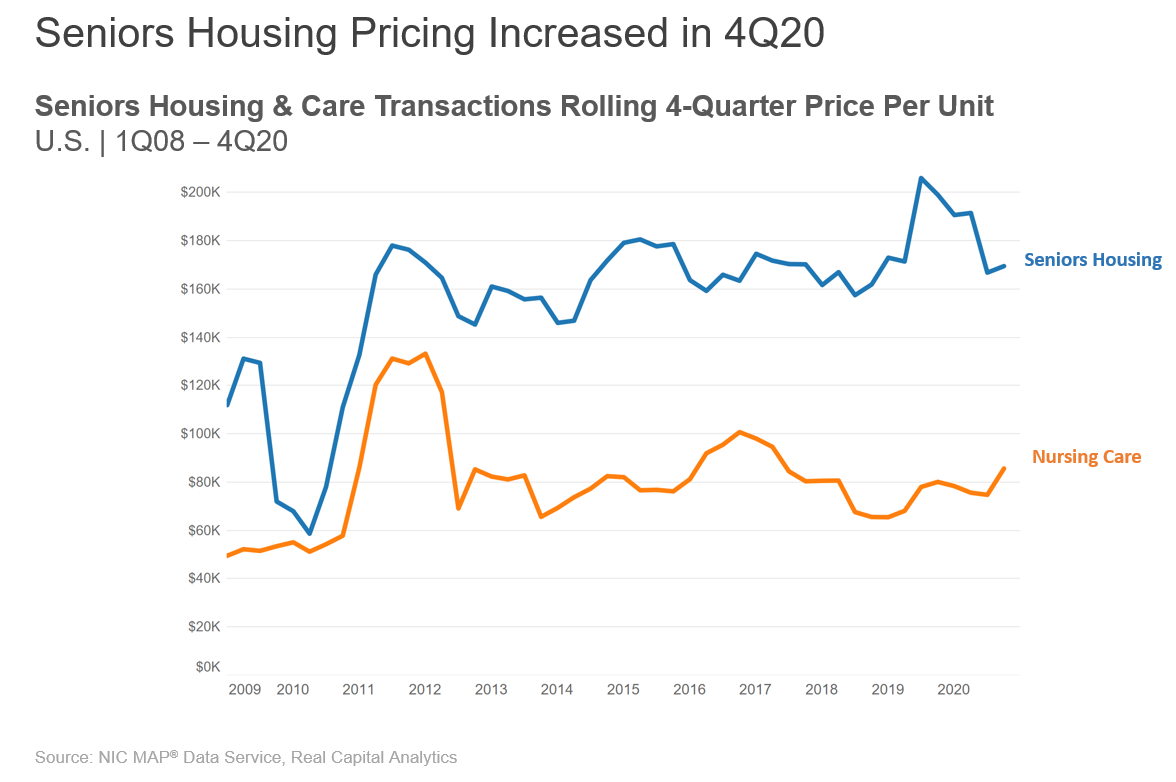

Skilled Nursing Price Per Bed a Surprise in 2020

There was a difference in closed transactions pricing trends between seniors housing and nursing care in 2020. One may have thought that, going into the pandemic, the pricing for both seniors housing and nursing care (i.e., skilled nursing) property transactions would decline. However, comparing the fourth quarter of 2019 to the fourth quarter of 2020 shows that seniors housing unit pricing decreased 14.8% to end 2020 at $169,700 per unit, but nursing care price per bed increased in that same time period by 6.9% to end the year at $85,800 per bed.

The graph below depicts this difference by showing the rolling-four-quarter seniors housing price per unit (PPU) and nursing care price per bed. This pricing graph is a national measure, and it is not same-store; therefore, the mix of properties could impact the results. It does reflect, however, what traded in the market, albeit with relatively lower transactions closed in 2020 due to the pandemic. The recovery in seniors housing pricing will likely depend on the direction of net operating income (NOI), barring any significant interest rate movements, and that means occupancy is a big factor as the sector progresses through 2021.

In regard to skilled nursing, what does this say as price per bed holds firm during this time of crisis? For one, some properties trading could be higher quality with good operators, and the buyer believes this environment is temporary so why give a discount for that? In addition, there is still a very attractive expected spread in terms of the interest rates on debt and the expected long-term cash flow yield of a high-quality property, which may be supporting price levels. Many skilled nursing properties are financed through long-term HUD loans that often have relatively low interest rates. Lastly, there are some small private investors, owners and/or operators looking to expand regionally and have strong long-term views about the sector. Many of these buyers see opportunity in the future as long-term care needs will grow given the sheer demographics and also the fact that a very large portion of the aging population will have multiple comorbidities, will not be able to afford private pay assisted living, and will be unable to receive care in the home 24 hours a day.

In wrapping up, the seniors housing and care sector includes many types of investors. Most are steadfast in the long-term viability and strength of the sector and see significant opportunity despite near-term pandemic-related challenges. Indeed, the sector will need to navigate uncertainty in 2021. One priority will be to build back the balance sheet liquidity lost during the pandemic.

Broadening the Stage for Seniors Housing & Care

Facilitating new connections is a part of NIC’s mission. For many, that means networking at NIC events, such as the upcoming 2021 NIC Fall Conference, or building new business relationships on the NIC Community Connector networking platform. For NIC Co-founder & Strategic Advisor Bob Kramer, it’s bigger than that. “When I stepped down as NIC CEO a few years ago, part of my new role, in addition to advising NIC, was to become a scout and an ambassador, identifying and reaching out to potential new partners for seniors housing and care,” Kramer explained. “I was tasked with educating and inspiring prospective new partners and collaborators to understand the potential of working with seniors housing and care – and to help our traditional audiences prepare and plan for the near future.”

Since that time, Kramer has been speaking to leaders beyond the senior living sector, educating them on the industry, and sharing his insights on what opportunities and challenges the future may hold. In addition to numerous boards and business groups, he has addressed some of the most important and influential organizations in healthcare, academia, technology, and regulatory policy. In recent months, Kramer has spoken at meetings hosted by the Milken Institute’s Center for the Future of Aging, the Urban Institute, the Brookings Institution, the Milbank Memorial Fund, the AARP Public Policy Institute, the National Academies of Sciences, Engineering, Medicine, and many more.

The COVID-19 pandemic has significantly accelerated the pace of many of the changes which Kramer has been speaking of for some time. Some may seem to have come to fruition seemingly overnight. Telehealth, for example, is not a new idea for more safely and efficiently delivering care for seniors housing residents, but over the past year its adoption has skyrocketed. But that’s not the only change that the pandemic has necessitated and crystallized. Kramer now envisions a swift and disruptive broadening of the industry, which will, of necessity, involve new partnerships and collaborations with an array of industries and stakeholder groups which up until now have not needed to connect with seniors housing and care leaders. For the first time, innovation in seniors housing will define not only its own fate but may be central to the success of numerous stakeholders far beyond their traditional silos, who are seeking to scale their senior-focused products and services.

According to Kramer–and now to many of the new audiences he’s been engaging with–senior living, in its many forms, must adapt to a series of new market realities in order to survive and prosper. That’s where the need to make new connections arises. Kramer said, “Senior living will need to interact with healthcare partners and payers, policymakers, technology providers, academics, and others, in order to adapt and provide the products and services that both consumers and payers have already begun to demand.” But to do so will require a greater level of understanding of seniors housing and care, particularly among those not already familiar with the industry.

All of these players will need to understand, looking at their own market from outside perspectives, that there are enormous opportunities, through partnerships, to deliver new models of housing, care, and services that customers will need and demand. “Failure to do,” warned Kramer, “will result in many senior living providers standing by, as new competitors, likely from other industries, will steal their market from them.”

On top of that, the impact of the COVID-19 pandemic has also raised the bar for consumer (i.e., residents’ and their families’) expectations for transparent communication, safety, infection control and prevention, use of technology to enable peace of mind, care delivery, and resident engagement.

Senior living will need to offer newer, savvier models of care and community, as well as a great deal of modern inventory, but will require new partners to do so. In a time of value-based care, COVID-19 policy changes, evolving consumer demands, and new models of healthcare delivery, the days of the personal care model that only provides assistance with activities of daily living, in which residents in need of medical care are simply transported and left to the healthcare system, are likely very limited.

Kramer points out that disruptors may be coming after the seniors housing market. He said, “Today, many companies in the sector are fatigued from the long, hard fight against COVID-19, and have suffered a long period of higher expenses and lowered revenues. While they need to be investing in new technologies, safety systems, and attracting a demanding new generation of customers with an aspirational value proposition, many are just struggling to survive.” Other business sectors, such as big tech companies and Silicon Valley startups, along with major pharmacies and giant retailers, for example, are already making moves to serve seniors, potentially at the expense of traditional seniors housing and care. As Kramer pointed out, “They are looking at the potential of a market which, traditionally, seniors housing and care has only managed to penetrate at a rate of 10 to 11 percent of the age 75-plus population.”

In his talks around the country, Kramer finds himself educating groups on the realities and business dynamics of an often-misunderstood industry. He gives them a more balanced view of what it takes to run a community that is home to frail elders. It likely is not surprising to seniors housing leaders that too many people are confused on terminology, types of residents, different business models, and many other critical factors that define the industry. Such confusion is on display daily in the many news stories that focus on the sector.

Kramer has found that NIC’s focus on data, analysis, and research, which in 2019 produced the landmark study which introduced the topic and coined the language of the “Forgotten Middle” seniors housing market, serves to enhance the credibility of NIC to engage with audiences on a broader scale. In addition, Kramer notes, “With all the understandable focus on quality of care in light of the pandemic, this moment offers the senior living industry an important opportunity to stress that senior living is about much more. Though quality of care is table stakes in a post-pandemic era, what is most significant to residents is their quality of life—in the sense of human connection, belonging, and purpose—that the senior housing community is in a position to provide for millions.”

You may already know Bob Kramer for his long history of thought-leadership in seniors housing and care. But did you know he was in attendance at some of the last concerts of a number of legendary musicians? Find out more details as Beth Mace speaks with Bob in the new NIC Chats podcast, launching later this month.

The State of the Senior Care Insurance Market: A Conversation with AmWINS Healthcare’s Mike Walton

By Jason Zuccari, Vice President of Business Development, Hamilton Insurance Agency

It should come as no surprise that 2020 was hard on the senior care insurance market. But before COVID-19 hit, the General and Professional Liability (GL/PL) sector was already facing a gradually hardening market after soft cycling over the last decade. Declining markets and an inability of carriers to maintain profitability spurred the downward trend, fueled by increased litigation. Additionally, adverse claim development has sent rates and deductibles through the roof.

It should come as no surprise that 2020 was hard on the senior care insurance market. But before COVID-19 hit, the General and Professional Liability (GL/PL) sector was already facing a gradually hardening market after soft cycling over the last decade. Declining markets and an inability of carriers to maintain profitability spurred the downward trend, fueled by increased litigation. Additionally, adverse claim development has sent rates and deductibles through the roof.

Add the coronavirus to the mix, and you have a recipe for grim uncertainty. Despite knowing that GL/PL carriers have COVID-related claims in hand, their true liability is yet to be determined. As a member of NIC Future Leaders Council and Vice President of Hamilton Insurance Agency, one of the nation’s largest independent brokerage firms specializing in senior housing and long-term care facilities, I have had a front row seat to the changing tide. To discuss the forces driving these trends upward, I sat down with Mike Walton, President of AmWINS Healthcare. AmWINS Group is the largest specialty insurance wholesale insurance brokerage firm in the U.S.

Zuccari: To what do you attribute rising rates in the long-term care insurance market?

Walton: Litigation against nursing properties continues to increase year after year. Over the past 10 years, the frequency of claims has increased nationally by approximately 40 percent per 100 occupied skilled nursing beds. Recent studies projected a 0.4 percent increase in frequency on an annual basis. However, these projections were based on data that does not consider the effect of the COVID-19 pandemic. As such, actual claims experience in 2020 and 2021 may be much greater. In addition to frequency of claims, increased severity is also a significant concern. The average professional liability claim nationally is just under $228,000 and trending at an increase of approximately 2.7 percent per year. In many venues, the frequency and severity of claims are much greater than the national averages. In addition to adverse litigation trends, another contributing factor to the hardening market is that there are far fewer commercial insurance markets underwriting long term care liability risk than we had several years ago. In just the past few years, we have seen at least 15 insurance companies exit the senior care liability marketplace. The remaining markets are far more selective as to which facilities they are willing to insure and require higher premiums and/or deductibles to meet their obligations to pay claims and meet financial objectives. Depending on the litigation trends in certain regions of the country, the number of markets willing to underwrite senior care properties may drop by more than two-thirds.

Zuccari: In this new climate, how much scrutiny on facilities can operators expect from underwriters?

Walton: With a wave of acquisitions in the senior care industry, underwriters are scrutinizing buyers with great care. They are also looking at the buildings and operations being purchased as new buyers can’t make quality and risk improvements overnight. Litigation trends of the venue, claims associated with the building, existing quality and clinical issues, staffing considerations, and other existing risk factors are significant considerations during the underwriting process. Buyers should be proactive with their due diligence in understanding the liability risk associated with the seller’s operations and how it may impact their cost of funding liability risk. Often, distressed operations are the most attractive for acquisition. While the location of a building and past ownership are not modifiable, buyers should identify operational concerns with respect to liability exposures and develop business plans with quality and risk management objectives that will be initiated immediately to improve liability risk and avoid claims. These objectives and plans should be presented to prospective insurance providers in a fashion that will impact the underwriting process to the advantage of the buyer. It is especially beneficial for buyers to work with insurance representatives that can help evaluate the risk pre acquisition, provide the tools and services needed to improve risk post acquisition, and effectively advocate and influence insurance providers in the underwriting process.

Zuccari: What are other benefits of enlisting an experienced broker, to be a middle-man between operators and underwriters?

Walton: The role of a broker, beyond placing business, includes claims advocacy and claims management. It comes down to understanding and communication. We often receive loss runs that provide no detail as to the cause and circumstances of the claim. For example, a claim description often states something as simple as “medical incident” or “negligent care”–one reserve for the same description may be for $3,000, and then another $100,000. Why the disparity? What does the claims adjuster know that is not on the loss run? A broker should be on top of that, corresponding directly with a claims adjuster to determine the difference between the two disparate reserves. It is critical that the client knows what is happening with each claim and be given the opportunity to participate in providing information that may be critical in mitigating the outcome of defending or settling a claim. Risk assessment, risk management, and claims advocacy are among the services a valued insurance representative/broker should bring to their client.

Zuccari: What can existing operators do to stay ahead of the curve?

Walton: If they’re able to understand the details of what goes into a star ratings and what information provided to CMS affects those ratings, they can anticipate and proactively address any concerns underwriters may have regarding such ratings. We, along with some of the better underwriters in the industry, do not rely on the CMS star system to evaluate a facility. It is, in the opinion of many, a very flawed assessment tool. There are analytic tools that can accurately assess a facility’s quality and associated liability risk. We can provide our retail partners with these analytic tools, and provide operators with the information they must have to understand how underwriters view their facility and enable them to address any negative views. Further, these same tools can be used to improve quality and risk, avoid fines and penalties, and maximize reimbursement.

Zuccari: How can operators structure insurance arrangements to optimize coverage while keeping costs low?

Walton: If an operator’s claims are predictable from year to year, then they should consider self-insuring the predictable losses via a deductible or self-insured retention. Otherwise, they will just be trading dollars with the insurance company. This is particularly relevant for larger facilities where operators have a pretty good expectation of what their claims are going to be every year. In one recent example, we just worked on an account in New York with 260 beds, and historically they average almost seven or eight claims a year averaging $100,000 to $150,000 per claim and $600 – $700K total incurred losses per year. In this case, it makes sense for that facility to self-insure the first $100,000 to $200,000 per claim. To fund $700,000 in claims with an insurance company, it would cost the account over $900,000. For every dollar paid in claims by an insurance company, they must collect an additional 30 to 40 cents to cover overhead. There are many creative structures that can be provided to properties with predictable claims, as well as those that have an occasional claim. A good insurance representative/broker should explore such structures on behalf of their client.