Deep Dive into Northeast Seniors Housing Markets

Beth Mace

This is the fourth in a series of NIC Insider articles that “go deep” into a region of the country to examine seniors housing supply and demand market fundamentals. In the first article of the series on California, it became clear that the supply-constrained coastal metropolitan markets have experienced limited development which has supported high occupancy rates and significant rent growth. The less land- constrained Central Valley of California differed and has been experiencing more development, lower occupancy levels and weaker rent growth. In the second series of articles on the Southeast, development was more rampant, with the differences between stabilized and total occupancy rates relatively wide as the influence of new development weighed heavily on total occupancy rates. [expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Further pressure on occupancy rates is expected in many of the metropolitan markets in the Southeast since there is currently a lot of construction underway. And in the third article that examined local markets, Texas was highlighted and it became clear that development has been very active there as well, especially in Austin and Houston. In these metropolitan markets, construction as a share of inventory exceeded 20% for Austin as of the first quarter of 2017 (1,500 units) and 8% for Houston (also 1,500 units), more than the 5.6% share of the national average. Houston has also had to withstand the negative influence of the drop in oil prices on the broader economy and the indirect effect this may have on demand for seniors housing. And the timing is particularly challenging since new supply has continued to enter the market, despite a slowing economy. In these markets, the ability of those operators who recently opened properties, as well as incumbent operators, to reach revenue, rate and occupancy goals may be challenging.

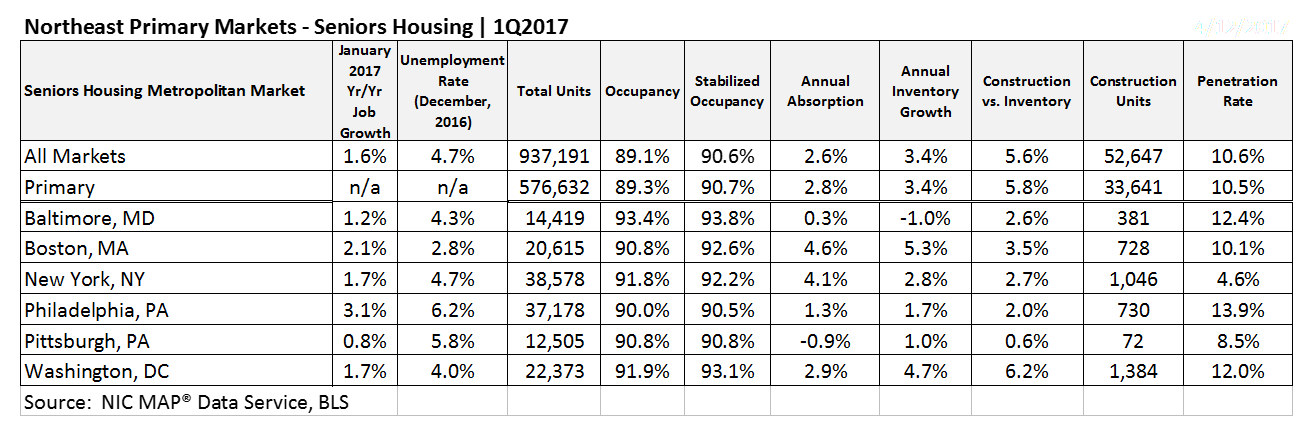

This article will examine seniors housing conditions for the largest metropolitan markets in the NIC MAP® Primary Markets in the Northeast. As the table above shows, this includes the six metropolitan area markets of Baltimore, Boston, New York, Philadelphia, Pittsburgh and Washington D.C. These six metropolitan areas make up 13% of the nation’s job base and except for Baltimore and Pittsburgh, all had job growth that exceeded that of the national annualized pace of 1.6% as of January 2017.

In addition to relatively fast job growth of 2.1% in Boston, labor market conditions are tight, with an unemployment rate of only 2.8%. Washington, D.C.’s labor markets are also quite tight, with a jobless rate there of only 3.8% (compared with 4.7% for the U.S. as a whole). The combination of tight labor markets and rising minimum wage rates in both D.C. and Boston will put pressure on expense growth for many operators of seniors housing and care properties, especially because labor expenses often account for up to 60% of the expense load.

In terms of seniors housing, a full 25% of the seniors housing unit inventory within NIC MAP Primary Markets is situated in the densely-populated metropolitan areas of Baltimore, Boston, New York, Philadelphia, Pittsburgh and Washington, D.C. Much like California’s coastal markets, these metropolitan areas are generally perceived to be markets with significant entitlement, regulatory or physical constraints for new development. Land that is available for seniors housing development must measure up against competing land uses such as residential single family or multi-family, mixed use or retail. The effects of limited development opportunities can be seen in the relatively low ratios of construction as a share of inventory in these six markets. For all Primary Markets, construction as a share of inventory equaled 5.6% in the first quarter. Only one market—Washington, D.C.—exceeded that ratio, while most of the other five Northeast markets had shares well below that rate. Moreover, in aggregate, these six markets are currently experiencing 13% of all construction in the Primary Markets compared with 25% of the inventory.

The flip side of the equation is demand, as measured by rates of absorption. Three of the six markets had absorption rates equal to or more than the Primary Market average of 2.6% in the first quarter. The strongest demand occurred in Boston, New York and Washington, D.C.

Because of these demand and supply conditions, occupancy rates tend to be relatively high in the Northeast markets, with all six markets exceeding the Primary Market average of 89.3% in the first quarter. Strongest occupancy was in Baltimore at 93.4%, followed by Washington, D.C., New York, Pittsburgh and Boston. Philadelphia trailed the pack at 90.0%. Limited construction in recent years has allowed the stabilized and total occupancy rates to be similar.

The exception was Boston, which saw a 5.3% increase in inventory in the past year. There, stabilized occupancy was 92.6%, while total occupancy was 180 points less at 90.8%. (A property is defined as “stabilized if it’s more than two years old or it has reached 95% occupancy. When the gap in total and stabilized is large, it is because there are a lot of properties in lease up which is pulling total occupancy lower). In fact, the NIC MAP Analyst® reports that there are currently 12 properties with a total of nearly 1,100 units that are not yet stabilized in Boston (there are 164 properties with 19,500 units that are stabilized). Moreover, there are currently 9 properties under construction with a total of 728 units coming on-line between now and the end of 2018. The combined effects of properties currently in lease-up and not stabilized, along with the properties that are presently under construction, suggests that incumbent operators in the market as well as operators that are opening properties will feel pressure as they strive to meet many of their business plans and pro forma assumptions. At 90.8% in the first quarter, occupancy was near a seven-year low in Boston (and near its 90.6% in the second quarter of 2016).

Baltimore and Washington, D.C. had the highest occupancy rates of the six Northeastern metropolitan areas at 93.4% and 91.9% as of the first quarter of 2017. They also had above average penetration rates at 12.4% and 12.0%, respectively. However, as discussed in past articles, high occupancy and high penetration rates do not necessarily go hand in hand, nor do high occupancy rates and low penetration rates. New York had a first quarter occupancy of 91.8%, above the primary market average of 89.3%, yet had a penetration rate of only 4.6%, and Pittsburgh had an occupancy rate of 90.8% and a penetration rate of 8.5%. Cultural factors as well as lifestyle choices, familiarity with seniors housing options as an alternative to living at home, operator mix and unit mix, and demographic characteristics are all factors that influence penetration rates.

New York is an interesting market to also look at further. The penetration rate in New York is a low 4.6%. This compares with the 10.6% average of the Primary Markets and ranks among the lowest in the nation. Construction activity in New York has been relatively limited since NIC began reporting data in 2006, averaging less than 2.6% of existing inventory. Limited development in turn helps to explain the low penetration rate and the relatively high occupancy rate of 91.8% in New York. Another less tangible factor in explaining the low penetration rate may be that many New Yorkers (especially those in Manhattan) live in rental or condo units (as opposed to detached single family residences) and already regularly bring a la carte services into their homes (care, services and food). Thus, the need to move into a property that offers many of these same services may be less compelling. That said, living alone in an apartment typically does not provide the positive benefits of socialization as well as hospitality and general wellness programs. Looking ahead, there are currently 10 projects under construction in New York totaling 1,000 units, but several others that are in the planning stages include the 15-story Hines/Welltower/Sunrise development that will be located at the corner of 56th Street and Lexington Avenue.

In wrapping up, the key takeaways on current market performance in the Northeast include:

- Generally high occupancy rates

- Generally limited construction

- Variation in penetration rates, and

- Potential occupancy challenges in markets such as Boston and Washington D.C.

[/expand] [cresta-social-share]

Understanding Your Market Study: Part 3

Lana Peck

The first segment of this multi-part series established that market studies are a critical component of determining whether a proposed seniors housing property is an attractive investment opportunity. The second segment touched on maximizing accuracy in defining a market area. This installment of the series will discuss the next phase of the research: quantifying and qualifying the competitive environment.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Conducting an in-depth study of the competition

The primary objective of a market study is to determine whether a market can realistically support new, existing or planned seniors housing stock. A competitive analysis delivers intelligence that can be used to design or reposition a proposed property and inform strategies such as what to build, how many residences or units to build, and the timing of when to enter a market. Market studies also inform future marketing strategies, and help determine if an operator is capable of taking or splitting market share with competitors.

A simple, but thorough way to analyze a competitive marketplace is to use a systematic, funneling approach. This involves three steps: the creation of a broad overview of the penetration of different product types and trends that affect all operators in the market area; the separation of comparable and competitive properties; and the analysis of key competitors.

1. Segment the marketplace

The first step is to gather market-level information on the collective properties which comprise that market, such as property type, profit status, unit mix, occupancy rates, asking rent levels and concessions, if any, and proposals of future development. Find out what’s planned, what’s already in the development pipeline, and what projects potentially could be entitled to lessen the likelihood of unanticipated occupancy or lease-up challenges. This often requires inquiries into local planning departments on a regular basis.

Identify and categorize the businesses that serve seniors, and segment the market by property/service type. Differentiate among the traditional property types of CCRCs (Life Plan Communities), independent living, assisted living, memory care, and nursing care, and from other seniors housing and care services such as home health providers, post-acute and sub-acute care facilities, senior apartments and active adult communities. Aim to obtain a broad understanding of the array of seniors housing options and home and community-based services for seniors, which may positively or negatively influence demand for the proposed product.

This is easier said than done as the lines between seniors housing property types are blurring across the continuum of care, creating complex combinations of seniors housing products and care segments that can be located in a single building or across a campus system. More and more often, assisted living overlaps with independent living and skilled nursing, so it’s not uncommon for dual-purpose or dual-licensed buildings to accommodate assisted living services in an independent setting, or to combine assisted living and memory support residences under one roof.

2. Separate the competitive from the comparative

The comparative process simply lines up the subject property and others in the marketplace per product type; however, concluding the analysis at this point creates limitations. Listing all the different senior living options in a market area without deeper distinction tends to overstate the competitive intensity of the environment (i.e. the penetration rate).

For example, two or more assisted living communities located within a 5-mile ring could be considered comparable, as could a number of assisted living units that comprise part of a continuum of care in other properties. However, to be competitive, these properties would share location and market area, and have similar levels of service and pricing, number of residences/units, and target demographics.

In highly penetrated markets, it is worthwhile to identify with which communities the proposed project will regularly compete head-to-head for the same residents. The factors defining what makes a property competitive vary from strictly objective data to subjective factors that add nuance.

It is important to note that solely looking at the “competitive” may overstate demand; therefore, a best practice is to conduct a dual analysis and calculate demand in the context of all properties in the market and then repeat with only those that are “competitive.” In most cases, demand studies for higher levels of care will require including all comparable properties. However, different methods by which analysts calculate demand will be addressed in a later installment of the Insider.

3. Understand key competitors

Taking a consumer perspective and looking at the marketplace from the eyes of a prospective resident may reveal weaknesses among the existing products that can be leveraged to maximize market share, shed light on barriers to entry, or gain marketing insight. Contrasting the proposed property against comparable properties helps the analyst drill down to the elementary qualities that separate the comparable from the competitive, and strengthens and deepens the analysis. For example:

- Potential opportunity: The proposed property may be in the pre-development stages, but three of the most likely competitors are comprised of aging, lackluster stock.

- Potential challenge: The proposed property may be new and shiny, but the closest competitor may have been in operation for years and have an established, positive reputation, consistently drawing residents from the surrounding neighborhoods.

- Potential opportunity: The proposed property may be a renovation that divides units to create new, private suites, while a similar property across the street may have only a handful of private rooms and still adhere to a medical model of care.

- Potential challenge: The proposed property, a renovation and repositioning project, may have been full with a wait list for years, but a call to the local planning and zoning authorities reveals a new development with a state-of-the-art fitness center will break ground within the next six months.

Clearly, a competitor analysis conducted from the desktop can be very detailed. However, it is important to visit the competitors in person and tour the market area to validate assumptions.

Considering the objective and subjective data together paints a compelling picture of the key competitors in the marketplace. Keep in mind that the more thorough the competitor analysis, the more reliable subsequent market feasibility and demand studies will be.

To hear tips on the public sources of key information to maximize the thoroughness of a competitive analysis, check out the April 19 blog post, and plan to watch the recorded webinar that will be available May 24. [/expand] [cresta-social-share]

Genesis HealthCare’s B.J. Hauswald Discusses the Growing Role of Value-Based Care

Strategic shifts to meet changing market conditions are necessary to achieve sustainable success.

This approach has been applied by B.J. Hauswald to her work as senior vice president of strategic development at Genesis HealthCare—an owner and operator of 475 skilled nursing and assisted/senior living facilities. She joined Genesis in 1998 as treasurer, and since then has helped to guide the company through a number of transitions. While her early years at Genesis were focused more on developing the company’s portfolio of assets, her role has now evolved to help the company transition to value-based care and population health management.

NIC recently spoke to Hauswald about the future of the changing skilled nursing sector from her perspective at Genesis, and as a new member of NIC’s Board of Directors. What follows are highlights of the conversation.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

NIC: What first interested you in the long-term care field?

Hauswald: I’ve always been involved in growing and changing industries. Before joining Genesis, I was a health care banker, and before that, I financed the cellular and cable industries through their early growth. What has kept me in the long-term care field is the combination of the ability to be mission- and business-focused at the same time. Our mission is to manage the challenges of caring for a frail, older population. We need to develop sustainable solutions to support these populations while providing sufficient returns to enable the company and industry to continue to invest in the sector. Genesis has always had a willingness to invest in innovation and explore potential alternatives for care delivery models. That’s what keeps me going.

NIC: How have your career and work at Genesis prepared you for your new role on the NIC Board?

Hauswald: I see myself as a representative of the new value-based arena. We need to prepare ourselves as a company and industry for population and value-based health management. NIC is moving in that direction and will play a big part in that future.

NIC: How does NIC’s mission—ensuring access and choice in seniors housing and care—resonate with you?

Hauswald: Seniors housing is real estate and private pay oriented, but we’re facing a trend where we will see an enormous population that needs services and do not have the savings to be able to afford the alternatives that currently exist. The development of new supportive delivery models, for those consumers with more limited resources, is a good mission for NIC.

NIC: What challenges have you faced as a woman in a male-dominated industry, at least at the executive level? What do you bring to the table as a woman?

Hauswald: Many years ago, I was a founding member of the Women Business Leaders of the U.S. Health Care Industry Foundation, whose focus has been greater participation by women serving on the boards of health care companies, and the promotion of women as senior managers. Women are the majority of our employees, caregivers and residents. So I think it’s something to work on, and it’s changing. I’m working more and more with ACOs and health systems, and many of the quality improvement and strategic positions are held by women. And hopefully that will translate into more C-suite executives over time.

NIC: What are the biggest challenges facing the skilled nursing industry today?

Hauswald: The lack of sustainable financing for the industry prevents it from making the investments needed to serve the needs of future patients and residents. There is no long-term care Medicare entitlement in this country, and people are surprised, at the difficult time when transitioning a loved one, to discover this. Skilled nursing loses money on Medicaid residents and makes a small profit on Medicare patients. And in the short run, value-based care is driving down Medicare utilization for skilled nursing, making it very difficult to sustain profitability.

NIC: How will these changes evolve over time?

Hauswald: Demographic trends and the relatively lower cost of serving patients in skilled nursing facilities will eventually drive more business our way. Payors and ACOs are value oriented and are sending more people directly home to save money, meaning that those who remain in skilled facilities are more complex, sicker and older than the patient populations of the past. The long-term ramifications of insufficient financing means we have not been able to invest as much as we would like in the clinical capabilities we need to better manage sicker, older populations. And there haven’t been many real technological advances to support clinical staff or care in our sector.

I hope we don’t need a national crisis to ultimately identify this as a problem and develop a solution. While I’m not optimistic that the current debate regarding health care and entitlement reform will move us forward, I am encouraged by some of the results we’ve had changing the culture and care delivery through alternative value-based payment opportunities. As an industry, we will need to change our real estate mentality to begin to address the needs of the population 20 years out.

NIC: Genesis is unique in terms of scale. What are the benefits and drawbacks of a large operation?

Hauswald: We have corporate resources that many of the smaller and regional operators which make up the majority of industry don’t have. And while a large organization gives you flexibility to try new approaches with sufficient scale such as value-based care, size sometimes makes it difficult to move as quickly as smaller operators. The industry today finds itself in an increasingly competitive situation, and a bit of a price war, if you think of length-of-stay as pricing. Everyone is trying to gain market share by producing better results with shorter lengths-of-stay without undermining profitability. Smaller operators are quite nimble responding to their own market’s needs, while we often need to consider whether a solution can work on a larger scale, in multiple markets, and with different patient populations. Rolling out solutions across an entire organization is challenging.

NIC: The idea of the Medicare-only or transitional-care skilled facility has generated buzz in the industry. Genesis has the PowerBack model. Why were you motivated to try this model, and what makes it successful?

Hauswald: The model was an extension of our short-stay units in skilled facilities to address the specific needs of the short-stay patient. We designed the facilities for a different model of care, focused on the delivery of more intensive clinical capabilities. We developed orthopedic, cardiac and pulmonary specialty units, which are supported by Genesis physicians and nurse practitioners.

What’s challenging is that the model is much busier than the traditional nursing home. These facilities for all short-stay are large with 120 beds. They have 150-200 admissions a month compared with 25-40 for other skilled nursing facilities. While the short-stay model requires substantial admissions to be sustainable, it draws from a pretty wide geography due to greater desirability compared to long-term care. It requires an exponentially greater capability to admit and discharge patients, since hospitals require us to take patients at all hours, and the more value-oriented ACOs want their patients to have rehab services seven days a week. You always have to be cognizant of what each market looks like when developing new facilities, but even more so with this model. Health care is very local. Some markets won’t have enough referral and admission volume, especially if fewer people are going to skilled nursing facilities in the short-run.

NIC: What data do you look at to evaluate quality?

Hauswald: In the past, the focus was on long-term care quality measures, such as the prevalence of pressure ulcers and falls. That has expanded to include short-stay measures, like 30-day readmission rates. We’re focused on a growing list of quality metrics for long-term and short-stay patients as we try to improve five-star quality ratings for all the centers. These are not only used by patients and caregivers, but also by third party payors, ACOs and health systems to choose preferred partners. In our value-based demonstration programs, such as the Bundled Payments for Care Improvement Initiative (BPCI), we are focused on readmission rates and skilled nursing utilization. Also, Genesis has 500 physicians and nurse practitioners participating in the Medicare Shared Savings Program, which includes population health-based metrics like hospitalization utilization, immunizations and other preventative measures. It’s making a big difference in the way we think about and change our business to provide more value to hospitals and payors.

NIC: Are there any metrics for which you wish you had better data?

Hauswald: Claims data is the real change maker. Having the ability to see what happens to patients post-discharge, along with overall Medicare costs and use patterns for patients is illuminating. The ability to take real-time claims data and couple it with internal data from our own electronic health records is extremely powerful. But we are only at the beginning of building those capabilities.

NIC: What insights can you share with investors on what to look for in a skilled nursing facility? What are the common characteristics of a successful community or red flags?

Hauswald: What makes this industry both valuable and challenging is that it is a people business. The number one thing that makes a facility successful is the strength of the executive team — the executive director, nursing director, rehab program director, and medical director. How attuned are they to the organization’s goals, and have they changed their practices to meet those goals? Leadership is more important than anything else. That is the key to success of an individual facility.

Click here to download the latest “NIC Skilled Nursing Data Report”

[/expand] [cresta-social-share]

Meet Richard Wang, a Former Intern and Now FLC Member Finding Success

By Anika Hartounian, Cornerstone Affiliates (dba HumanGood effective June 1, 2017)

When we think about the senior living industry and how we attract young talent, the story doesn’t usually start with the comment: “I knew I wanted to do this all of my life”. Unfortunately, the industry is not perceived as the most glamorous field by new college grads. Most young professionals in the space today either had personal life experiences which led them to a purpose-driven career, or their professional careers gradually led them to this changing industry, one full of opportunity, growth, and innovation.

NIC is at the forefront of attracting young talent into the senior living industry through established scholarship programs, internship opportunities, and working committees such as NIC’s Future Leaders Council (FLC). These efforts are focused on leadership development in the senior living space.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Everyone has a story to tell about their start in senior living.

We interviewed the FLC’s very own Richard Wang, who previously participated in the NIC internship program and last year was selected for the FLC class of 2019. His experience has been far from the stereotype of senior living as an industry that doesn’t offer young people many career opportunities. Wang was a highly motivated student, steered by his personal life experiences, who took advantage of the resources available through NIC. And now he is a participant in a growth industry, who is giving back through his involvement in the FLC.

Currently Vice President of Investments & Strategy at Belmont Village Senior Living, Wang recently shared his thoughts with NIC about his early career experiences.

NIC: Tell us about yourself, and how you became involved with NIC.

Wang: After graduating from USC, I moved to Beijing with the intention of building my career in real estate development at my father’s firm. Due to his health issues, he soon handed me the keys, and I ran the company for the next five years. Real estate development in China can be very challenging to navigate and I had to learn everything on the job. But I grew quickly and experienced situations I would have never faced if I had I stayed in the U.S. Several years later, just in time for the 2008 Beijing Olympics, I introduced two U.S. food and beverage concepts to the Chinese market when I opened an American sports bar/restaurant and a Vegas-styled VIP nightclub. Both venues, which received multiple awards, immersed me in the realm of operations.

In 2011, my father’s health deteriorated again, and a dearth of quality caregivers in China piqued my interest in seniors housing and care. That sent me on a quest to further pursue the industry. All paths pointed me back to the U.S. And I was accepted at the Wharton School at the University of Pennsylvania, where I found NIC.

NIC: How would describe your experience in the NIC internship program?

Wang: Going into the internship program, I was eager to learn. I wanted to absorb as much as I could during my three months at Belmont Village. As with many organizations, the majority of the training programs are geared toward the operations platform. There wasn’t a precedent for someone like me who had a real estate development and entrepreneurial skill set. Working with Paul Chapman, Belmont’s chief development officer, we created a hybrid internship program that offered me a chance to see senior living through various lenses. Throughout my internship, I looked for places where I could add value and came away knowing much more about the industry. The internship also allowed me to hit the ground running when I joined Belmont full time nine months later. Internships really can become what you make of them.

NIC: What interests you the most about the senior living industry?

Wang: From a fundamental level, I see myself as a major investor in senior living. The industry is poised for growth and it just makes sense. On a more altruistic level, I also have a personal goal to promote accurate, responsible investment into research-based senior care initiatives throughout the world—to offer seniors the care and dignity they deserve in new markets such as China.

NIC: What does the FLC mean to you?

Wang: I feel privileged to be a part of this class of hand-picked individuals. The FLC has helped me to focus on working with the young leaders who are shaping the future of the industry. I look forward to building strong ties with my classmates through our committees, retreats and collaboration on NIC initiatives.

Note: The deadline for nominating candidates for the Future Leaders Council’s Class of 2020 is Friday, May 26, and the nomination process and accompanying forms are available here. [/expand] [cresta-social-share]

2017 Spring Investment Forum Recap Series 1

The Medicaid Question: What’s Happening in Leading-Edge States

Changes to the Medicaid program and its funding mechanisms are likely to have a major impact on the skilled nursing sector which relies on Medicaid reimbursements for about 65 percent of its revenues.

The crucial industry issue was discussed by a panel of experts at the 2017 NIC Spring Investment Forum, during a session titled: “The Medicaid Question: What’s Happening in Leading-Edge States.”

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

The discussion took place just as legislation to repeal and replace the Affordable Care Act (ACA) was being considered. Though the effort to advance legislation failed, the proposed changes highlighted how Medicaid funding might be cut and seriously impact skilled nursing providers.

“There may be an effort to reform Medicaid,” said session panelist Larry Atkins, executive director, National MLTSS Health Plan Association, a group of managed care organizations that manage long-term services and supports (LTSS) for state Medicaid programs. “And there are no guarantees.”

The session was moderated by James H. Gomez, CEO and president of the California Association of Health Facilities, which represents 1,150 skilled facilities in California. Also speaking was former New York Health Care Association President and CEO Dick Herrick.

Gomez reviewed the proposed changes to Medicaid in the ACA replacement legislation to provide insights into where the program might eventually be headed. He noted that states have been incentivized to spend money on their Medicaid populations because the federal government has matched state funding. But policy discussions in Washington have focused on limiting or capping the federal government’s contribution. This could be accomplished through block grants, which give the states a fixed amount of money instead of matching state allocations. “Most states don’t like this idea because it puts the burden on the states,” said Gomez. He estimates a block grant system could translate into a $9 billion hit to the budget in California where 14.1 million people are enrolled in the Medicaid program.

Skilled nursing providers worry that the states will not properly apportion block grants, said Herrick. “This is a big issue.” He foresees tough battles with other provider groups, each lobbying for a shrinking pool of funds.

“This is a profound shift from a culture of maximizing Medicaid to one where the states get a lump sum of money,” said Herrick. “As a business person, you can understand why the federal government has had enough.”

The management of block grants or budget caps would be a challenge, said Atkins of MLTSS. The group was formed last September and includes 11 organizations that cover more than 800,000 Medicaid enrollees. About 160,000 enrollees are participating in a demonstration program for so-called dual eligibles, those who receive both Medicare and Medicaid benefits.

“There’s a value to managing this population,” said Atkins. “It’s a major part of the budget.” He added that home and community-based services comprise a growing part of Medicaid payments. These programs vary widely, but 22 states have already moved to cap long-term services and supports in one way or another, Atkins said.

New and creative ways are needed to finance long-term care services and supports, said Atkins. He noted that one of the fundamental problems with long-term care is that no financing mechanism exists for seniors who are not Medicaid eligible. He would like to see a system that allows Medicare dollars to fund support services for seniors. “We are trying to make the case that a good support program will have a positive impact on medical spending,” he said.

If budgets are squeezed under new funding models, Atkins said the states may look to managed care organizations like those offered by members of his group to help coordinate care and the associated payments of the frail elder population. A successful transition to managed care will rely on finding ways to build trust with skilled nursing operators, said Atkins. Panelist Gomez agreed, adding: “The plans are not our enemy. The plans have a job to do.”

Another challenge for providers is wage growth. A number of cities have enacted minimum wage increases that will result in higher labor costs. If coupled with lower Medicaid reimbursement rates, operators could face a very challenging environment, the panelists said.

The panelists concluded that operators and managed care organizations must partner together to make sure the system works, and has proper funding in the future. “In the long run, it’s an opportunity to show what we can do,” said Atkins.

Update: The U.S. House of Representatives on May 4 narrowly approved legislation to repeal and replace major parts of the Affordable Care Act, which would cut $880 billion over 10 years from the Medicaid program.

Hot New Investments in Senior Care

An under-recognized investment trend has the potential to enhance senior living operations and boost returns.

Private equity and venture capital firms are pouring hundreds of millions of dollars into innovative business models related to home care, care coordination, enhanced primary care at home and new technologies targeted specifically at frail seniors.

These burgeoning enterprises serve the same population as seniors housing operators, but they’re not tied to a bricks-and-mortar model. Instead, they offer new ways to deliver care and services to elders, which present an opportunity for savvy seniors housing operators and investors.

“You can’t care for seniors and be a successful operator in the future without having a greater awareness of the innovation taking place in aging care service delivery,” said Anne Tumlinson, CEO at Anne Tumlinson Innovations, a consulting firm based in Washington, D.C. “Real estate companies need to expand their capabilities and leverage these new platforms. “

The 2017 NIC Spring Investment Forum featured a session on the topic moderated by Tumlinson titled: “Hot New Investments in Senior Care.” (The entire video recording of the session is available here.) Other panelists included: consultant Melanie Bella, former director, Medicare-Medicaid Coordination Office, CMS; Benjamin Berk, CEO, Attuned Care; and Burt Yarkin, managing director, The McLean Group.

Yarkin commented: “People are looking at the future and they know senior care will be valuable.”

[/expand] [cresta-social-share]